Capital budgeting is the process of evaluating long-term investment projects. It involves analyzing expenditures that will generate benefits over multiple years. The key steps in capital budgeting are project proposal, review and analysis, decision making, implementation, and follow-up. Techniques for evaluating projects include payback period, net present value (NPV), and internal rate of return (IRR). NPV and IRR are more sophisticated as they discount cash flows to determine if a project will earn a return higher than the firm's cost of capital.

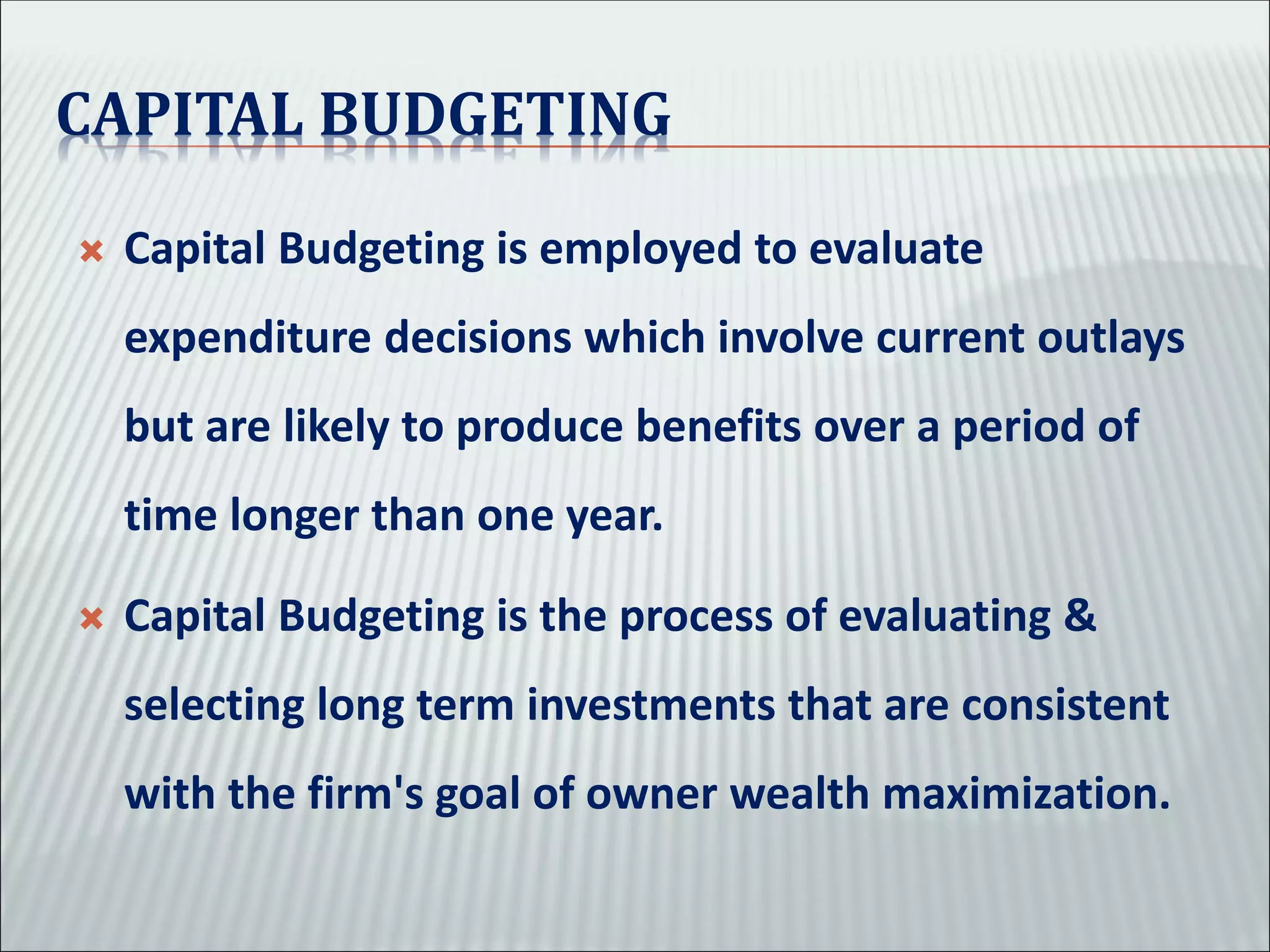

![(Original Investment- CCF YFR)

➢ Payback = [ YFR – 1] -----------------------------------------------

CF YFR

Where ,

YFR = Year of full recovery

CCF YFR = Cumulative CF at the start of year of full recovery

CF YFR = Cash flow during YFR

➢ Payback Period is generally viewed as an unsophisticated

capital budgeting technique, because it does not explicitly

consider the time value of money by discounting cash flows to

find the present value. Payback period also ignores cash flows

beyond payback period.](https://image.slidesharecdn.com/capitalbudgeting-230923170358-3228ef9b/75/Capital-Budgeting-pdf-8-2048.jpg)

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)