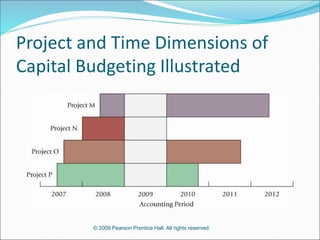

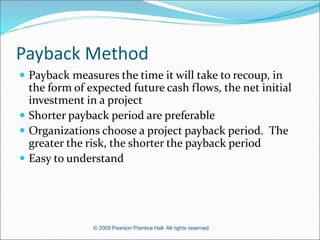

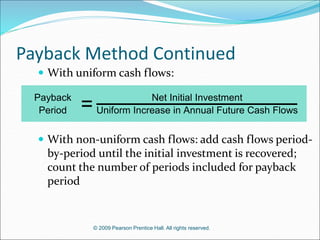

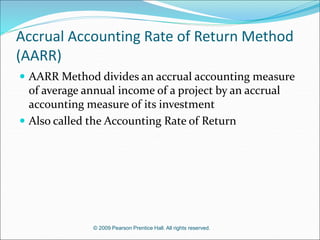

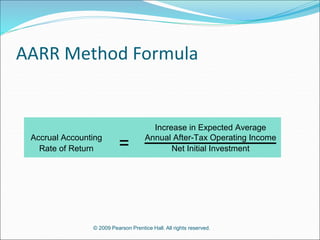

This document discusses capital budgeting and cost analysis. It covers two dimensions of cost analysis: the project-by-project dimension and the period-by-period dimension. It also describes the six stages of capital budgeting and four common capital budgeting methods: net present value, internal rate of return, payback period, and accrual accounting rate of return. Additionally, it discusses discounted cash flows, relevant cash flows, and strategic considerations in capital budgeting decisions.

![MINGGU 10,11 _ OBLIGASI DAN VALUASINYA VAL[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/minggu1011obligasidanvaluasinyaval1-240325143349-968cd9a4-thumbnail.jpg?width=640&height=640&fit=bounds)