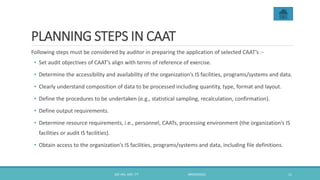

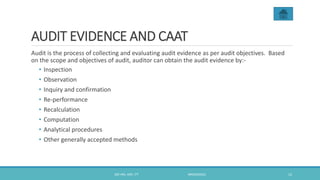

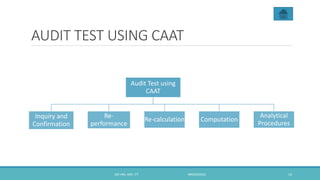

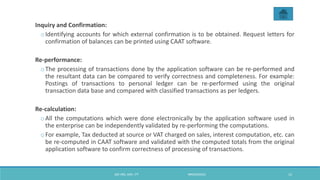

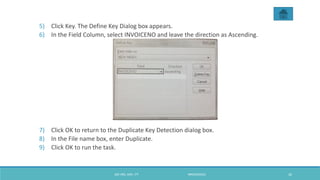

The document discusses Computer Assisted Audit Techniques (CAAT). It defines CAAT as using computers to automate accounting and audit processes. CAAT allows auditors to do more work in less time and provide more robust assurance. The document outlines planning steps for CAAT, types of audit evidence that can be obtained through CAAT, and audit techniques like snapshots, integrated test facilities, and embedded audit facilities. It also discusses audit sampling methods and provides an example of using IDEA software to detect duplicate invoices.