Download to read offline

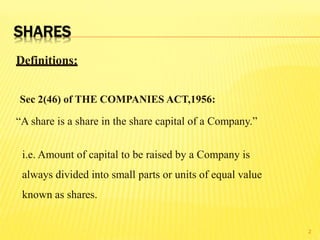

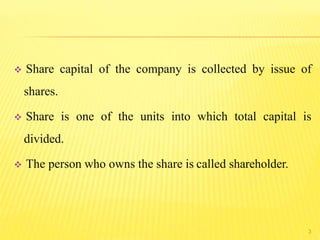

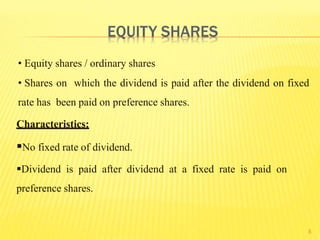

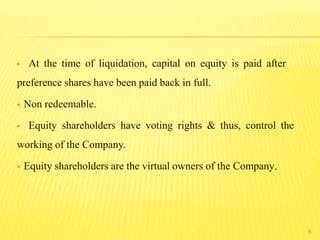

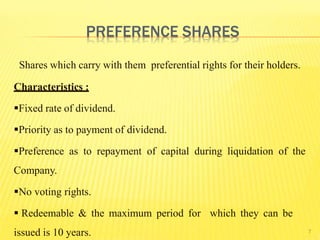

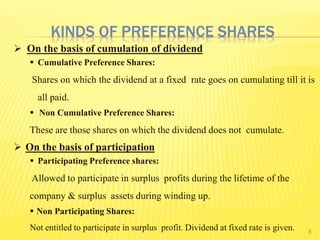

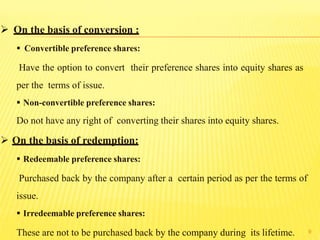

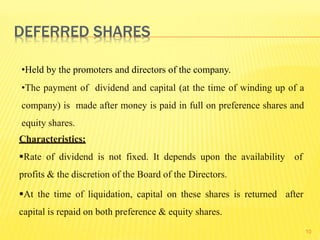

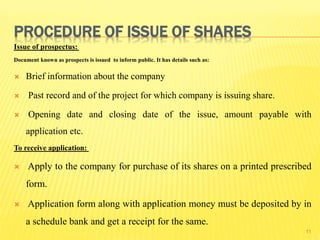

The document defines shares and discusses the different types of shares that can be issued by companies. It explains that a company's total capital is divided into equal units called shares. There are three main types of shares: equity shares, preference shares, and deferred shares. Equity shares represent ownership in the company and have voting rights, but no fixed dividend. Preference shares have a fixed dividend rate and priority in repayment but no voting rights. Deferred shares rank below equity and preference shares. The document also discusses the process of issuing shares through a prospectus, receiving applications, allotment of shares, and making calls on shares.