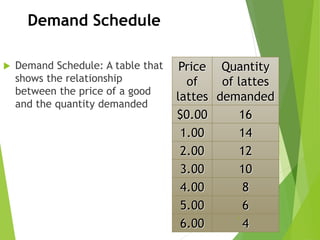

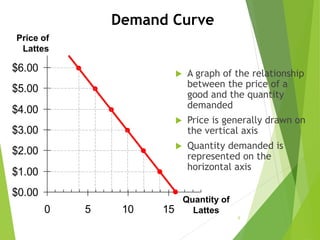

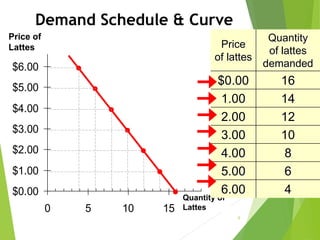

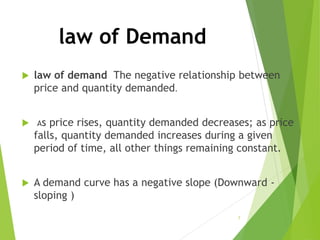

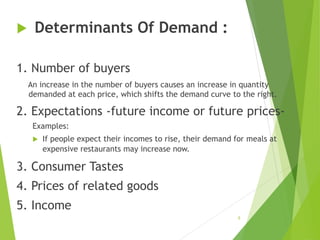

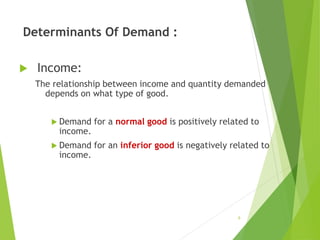

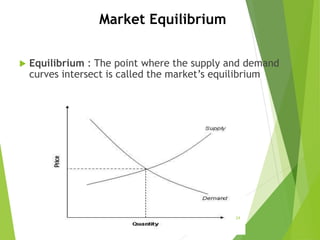

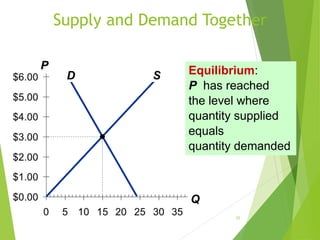

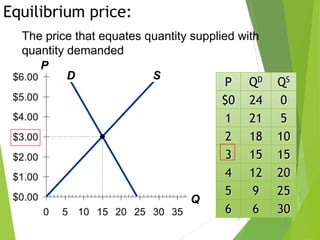

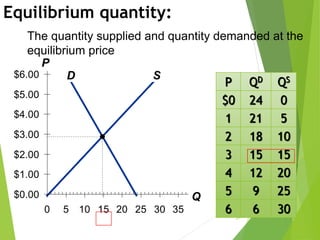

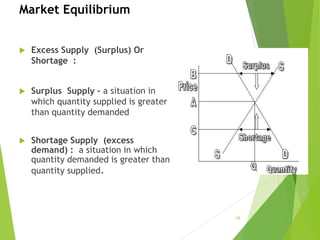

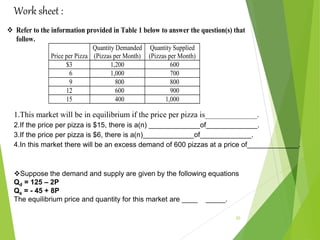

This document discusses demand, supply, and market equilibrium. It defines key concepts such as demand curves, supply curves, and how equilibrium price and quantity are determined by the intersection of supply and demand. Determinants of demand and supply are outlined. The document also discusses how shifts in supply or demand curves impact equilibrium. Consumer and producer surplus are introduced as measures of efficiency in competitive markets.