Download to read offline

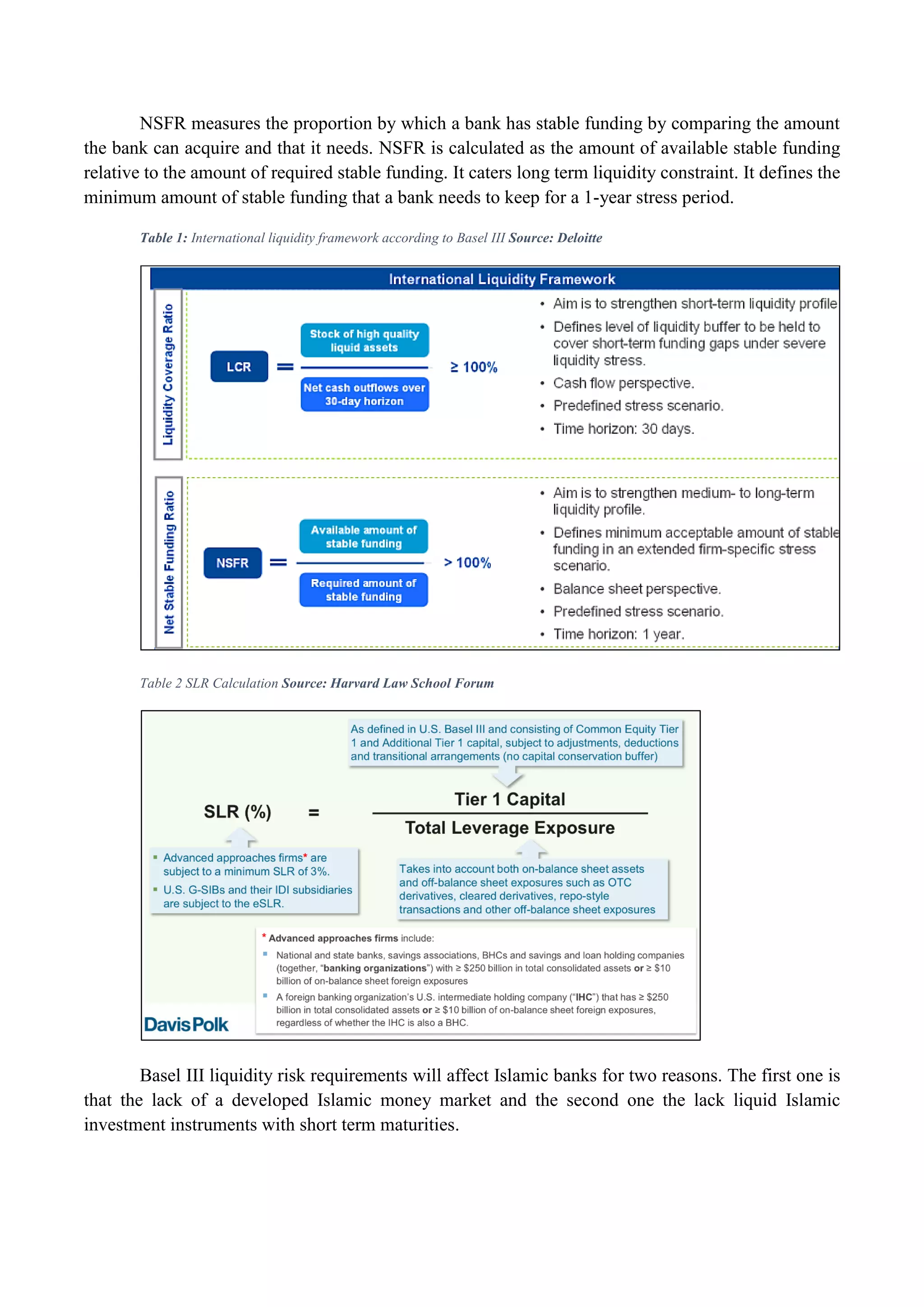

The document discusses Basel III, a global regulatory framework for banking designed to mitigate risks and enhance the resilience of financial institutions post the 2007-08 financial crisis. It focuses on liquidity risk management, outlining key components like the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR), which aim to ensure banks can meet their financial obligations. The challenges posed by these regulations, particularly for Islamic banks due to the lack of developed markets and liquid investment instruments, are also highlighted.