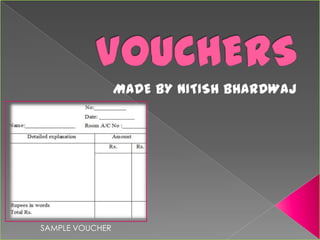

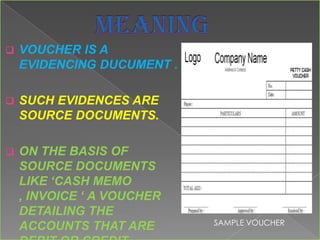

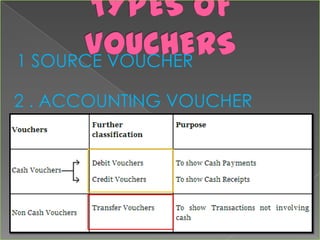

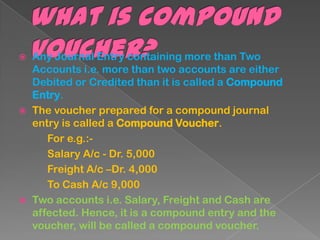

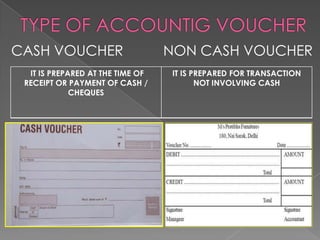

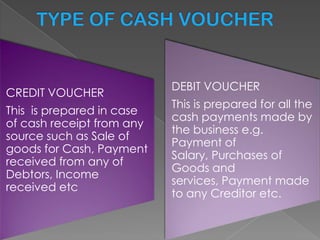

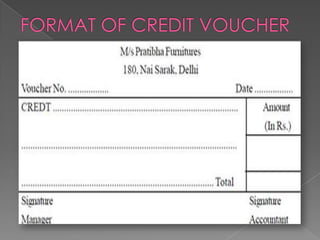

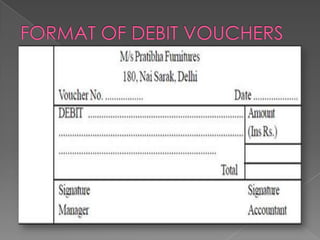

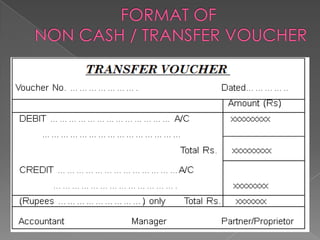

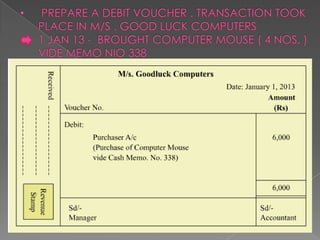

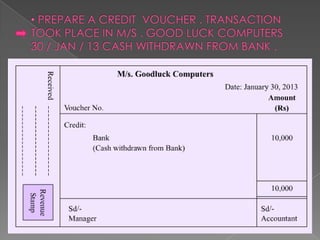

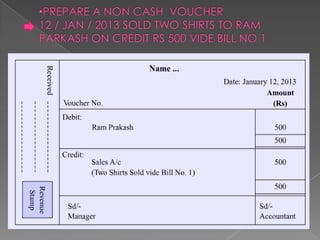

The document explains the nature and purpose of vouchers in accounting, describing them as written evidence of business transactions supported by source documents. It outlines different types of vouchers such as cash, non-cash, credit, and debit vouchers, along with the concept of compound vouchers for transactions involving multiple accounts. Vouchers serve as formal records signed by accountants, reflecting transaction details for accurate financial documentation.