1

Audit

• Presented By-Atharva Rajesh Gandhi

• First year M Pharmacy

• Subject: Documentation and Regulatory Writing

• Department Of Drug Regulatory Affairs

• Guided By- Dr. Lokesh Premchand Kothari

(M.Pharm, Ph.D.)

SHRI NEMINATH JAIN BRAHMACHARYASHRAM

SHRIMAN SURESHDADA JAIN COLLEGE OF PHARMACY

NEMINAGAR CHANDWAD DIST. NASHIK

Audit

Definition-

•Auditing is definedas the on-site verification activity, such as

inspection or examination, of a process or quality system, to

ensure compliance to requirements

•According to ISO defines as the “A systemic, independent, and

documented process for gathering audit evidence and objectively

assessing them to ascertain the extent to which the verification

criteria are met.”

•According to Internal Audit Standard Board(ICAB), “Auditing is

an impartial review of financial information of any organization,

whether profit-oriented or not, and irrespective of its size or legal

form, when such an investigation is conducted with a view to

offering an opinion thereon.”

3

4.

4

Goals Of anAudit

Goals

Ensuring

Accuracy

compliance

Risk

identification

Transparency

and

accountability

Fraud

detection

Performance

evaluation

5.

5

Audit Objectives

PRIMARY

OBJECTIVE

1. ToExamine

the Accuracy of

Books of

Accounts

2. To Express

Opinion on

Financial

Statements

SECONDARY

OBJECTIVE

1. Detection and

Prevention of

Errors

2. Detection and

Prevention of

Frauds

6.

6

Types of Audit

InternalAudit

External Audit

Second party Audit

Third party Audit

Process Audits

System Audits

Product Audits

7.

Internal Audit

i) Ensurethat on organization is meeting its own quality standards or

contractually required standards. (called a first party audit).

ii) Done by auditors who work for the Company.

iii) Auditors must be independent of the function they are auditing.

Purpose of Internal Audit :

• To ensure that adequate quality Systems are maintained

• To assess Compliance with the cGMP’s a firms standard operating

procedure.

• achieve consistency between manufacturing & testing facilities.

• To identify problems internally and correct problems prior to a

FDA inspection.

7

8.

8

External Audit

1) ExternalAuditors are separate from the Company

2) They may be hired by a Suppliers and customers

3) They may be audited by the government to verify.

Purpose of External Audit:-

• Reducing the risk of failure

• Confidence in the partnership arrangement.

• Carried out by Company on its vendors.

• No legal requirement to conduct the audit.

• Ensuring that requirements are understood

9.

9

• Second PartyAudits:

External audits done by a Company that has a Contract with the audited

firm is known as second party Audit.

• Third party Audits:

External quality audits done by an organization that has no contract with

the Company it is auditing is called a third party Audit.

• Process Audits :-

A process audits verifies that a documented process meets quality

standards. This process could be a manufacturing process or service process.

10.

10

• Products Audits:-

A product quality audit verifies that a physical products meets design

Specification's and other quality measurements.

• System Audits:

It is a review of how quality standards are measured and met by the

Company. It verifies the procedures used to measure the quality of the

product, how detects are recorded, and how the compony ensures that

failed product is not passed.

11.

11

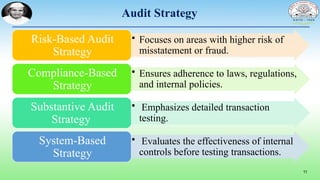

Audit Strategy

• Focuseson areas with higher risk of

misstatement or fraud.

Risk-Based Audit

Strategy

• Ensures adherence to laws, regulations,

and internal policies.

Compliance-Based

Strategy

• Emphasizes detailed transaction

testing.

Substantive Audit

Strategy

• Evaluates the effectiveness of internal

controls before testing transactions.

System-Based

Strategy

12.

12

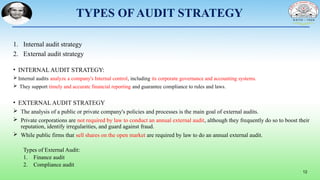

TYPES OF AUDITSTRATEGY

1. Internal audit strategy

2. External audit strategy

• INTERNAL AUDIT STRATEGY:

Internal audits analyze a company's Internal control, including its corporate governance and accounting systems.

They support timely and accurate financial reporting and guarantee compliance to rules and laws.

• EXTERNAL AUDIT STRATEGY

The analysis of a public or private company's policies and processes is the main goal of external audits.

Private corporations are not required by law to conduct an annual external audit, although they frequently do so to boost their

reputation, identify irregularities, and guard against fraud.

While public firms that sell shares on the open market are required by law to do an annual external audit.

Types of External Audit:

1. Finance audit

2. Compliance audit

13.

13

• Why isan Audit Strategy Important?

Helps focus on key areas (like financial records, internal controls, or

compliance).Saves time and resources by planning ahead. Reduces risks and

errors in auditing. Ensures rules and regulations are followed. Helps in better

decision-making based on findings.