Download to read offline

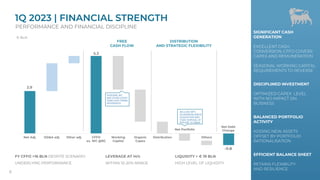

ENI reported its 1Q 2023 results, delivering on performance and strategy: - Production was up over 2% quarter-over-quarter to 1.66 million barrels of oil equivalent per day. - EBIT was €4.6 billion and net profit was €2.9 billion, resisting price impacts through profit improvement. - Cash flow from operations was €5.3 billion with excellent underlying cash conversion. - Leverage remained low at 14% providing financial strength and flexibility.