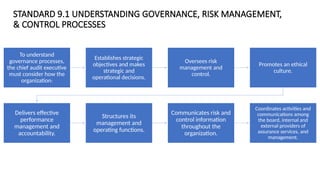

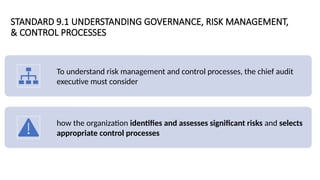

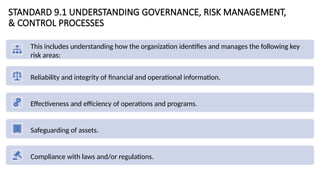

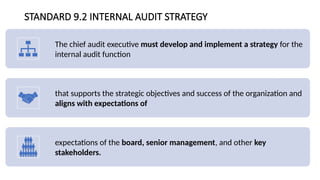

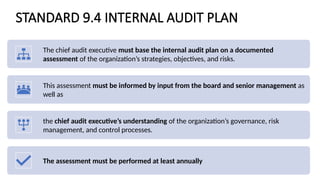

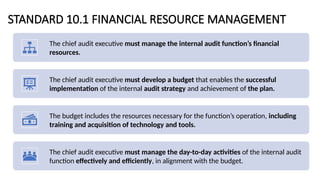

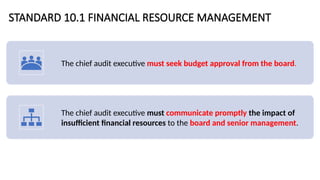

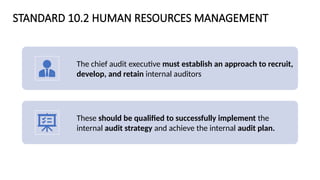

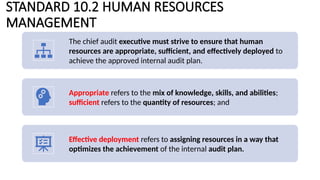

The document outlines the responsibilities and principles governing the chief audit executive (CAE) in managing the internal audit function according to global internal audit standards, with particular focus on strategic planning, resource management, and effective communication. It emphasizes the need for thorough understanding of governance, risk management, and control processes to develop an effective internal audit strategy, while ensuring continuous performance improvement and conformance with standards. Additionally, it highlights the importance of building relationships with stakeholders and establishing clear communication protocols for reporting audit results.

![[NALL OCR] HALL, Basil (1824). Extracts from a journal written on the coasts ...](https://cdn.slidesharecdn.com/ss_thumbnails/nallocrhallbasil1824-260202221936-b93ec330-thumbnail.jpg?width=640&height=640&fit=bounds)