Downloaded 20 times

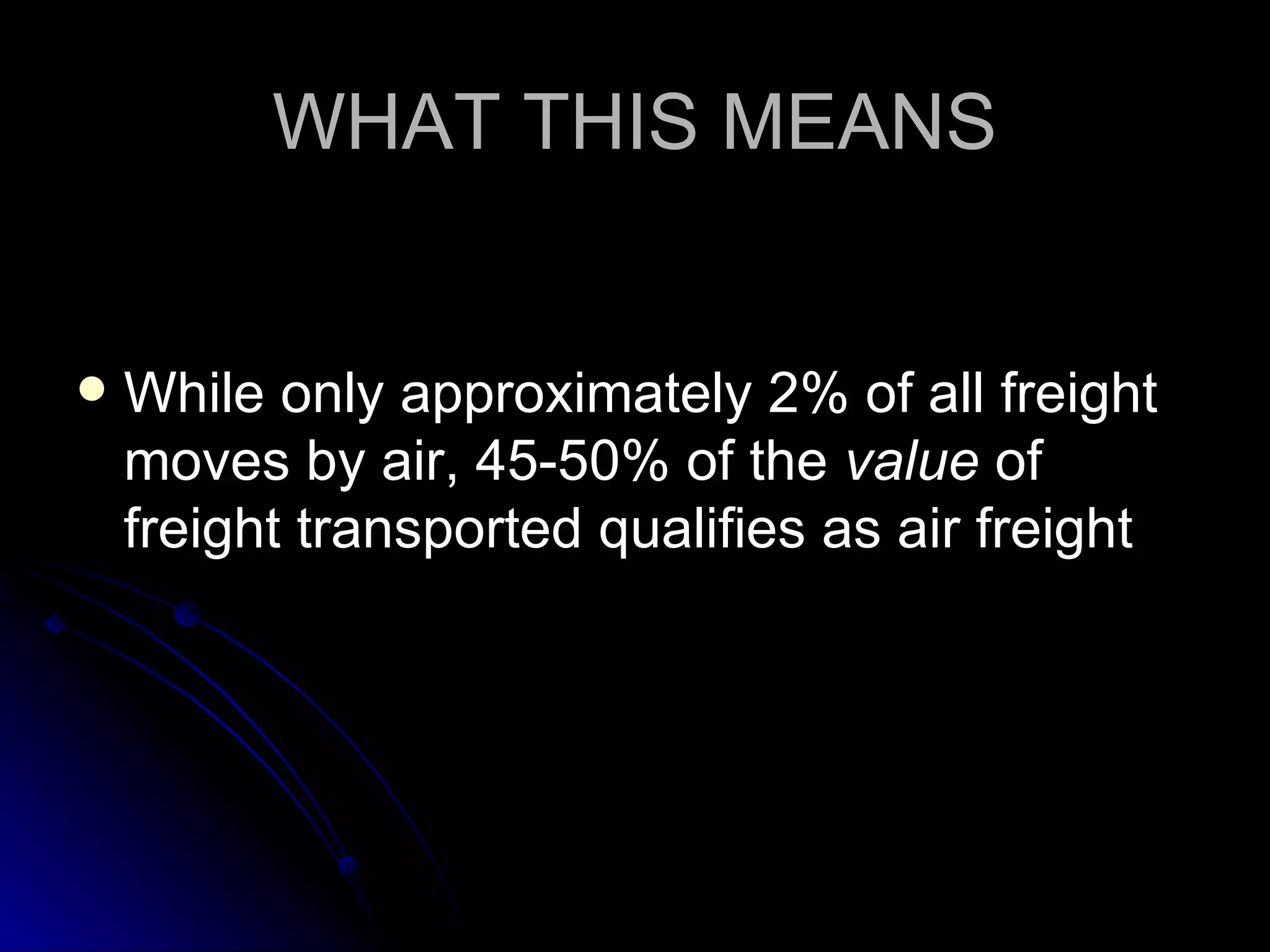

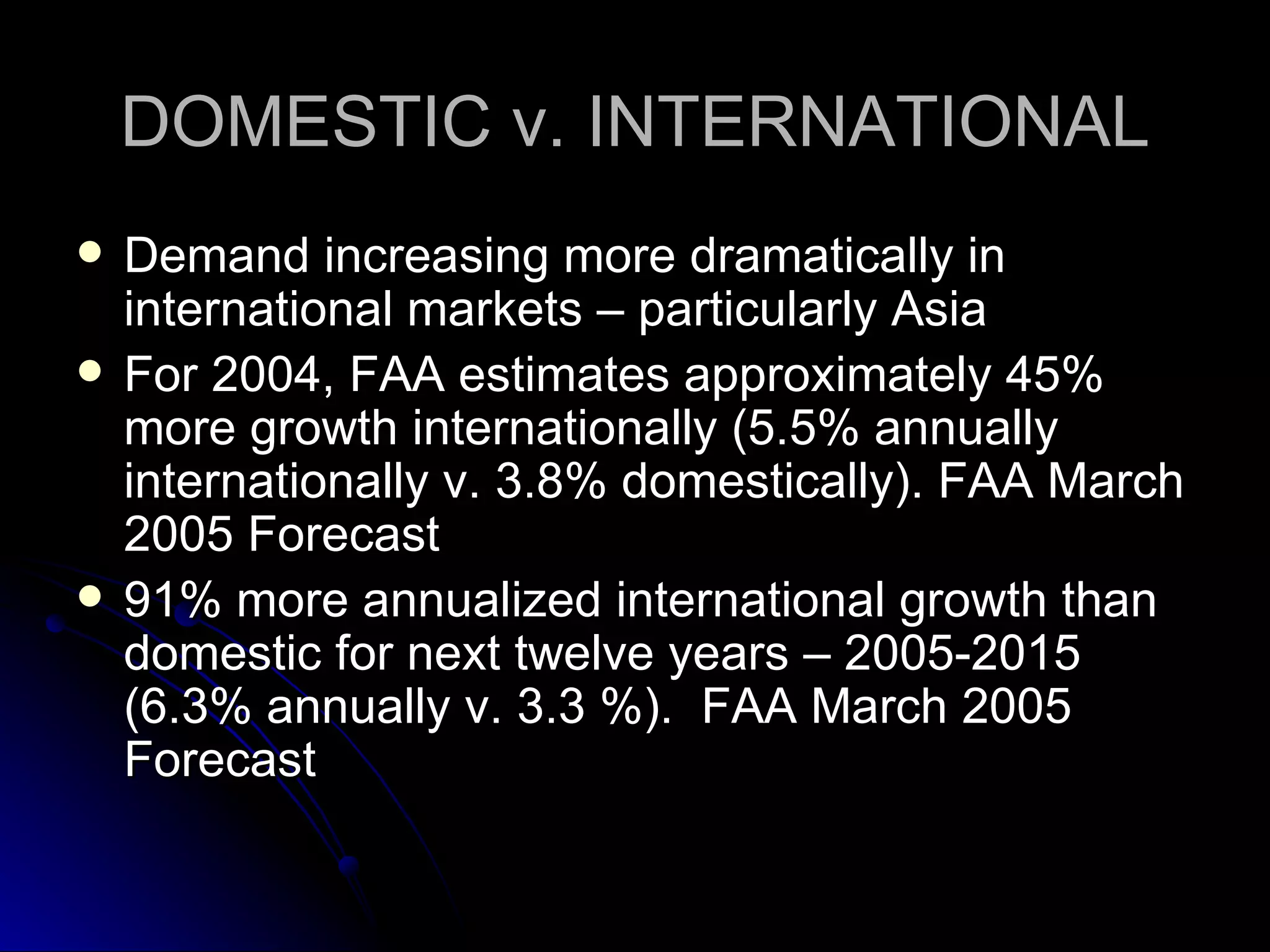

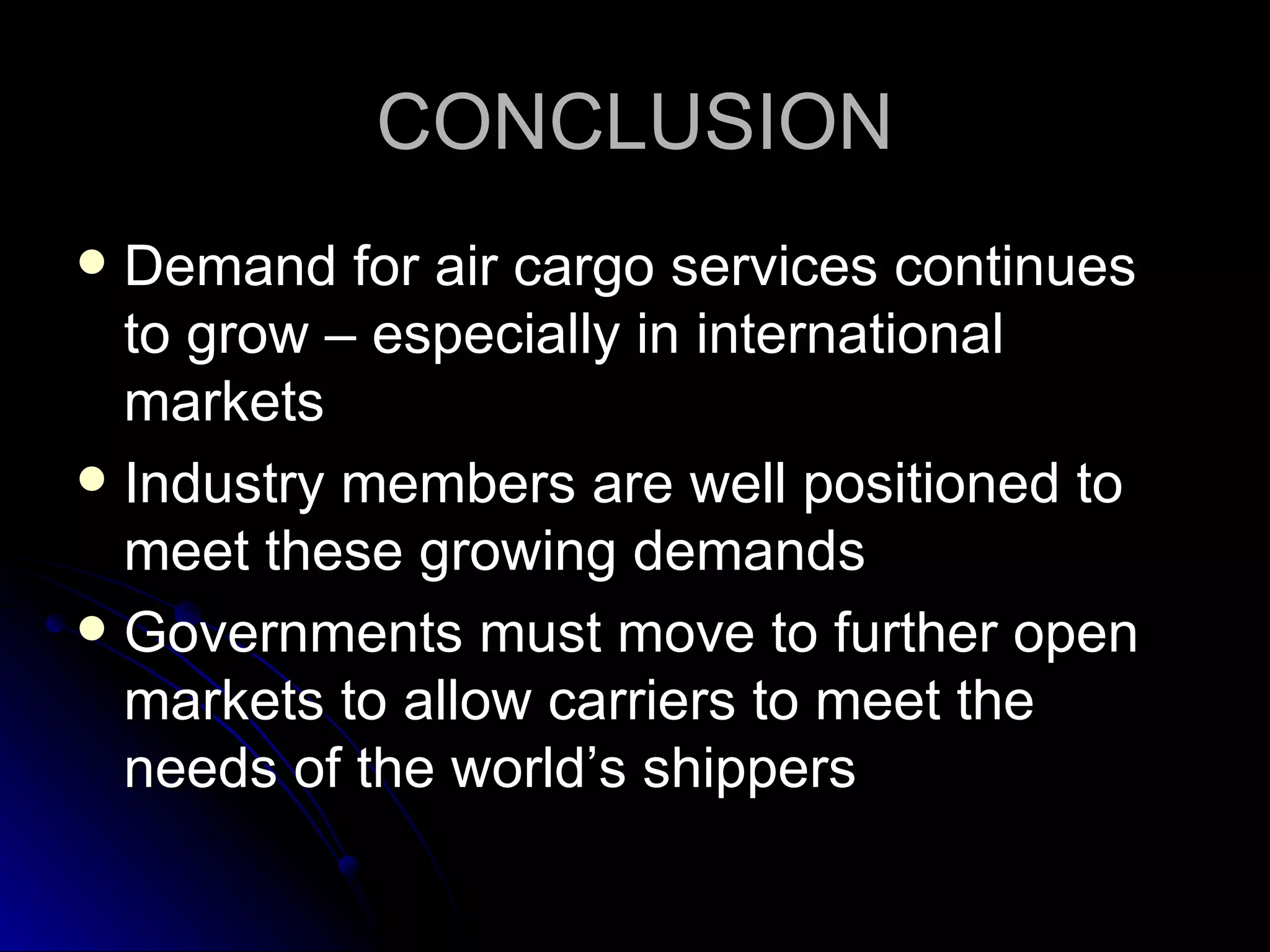

The document summarizes a presentation given at the Federal Aviation Administration's Annual Forecast Conference about air cargo demand. It discusses the different segments of the air cargo industry, including passenger aircraft bellies and all-cargo aircraft. It notes that while air cargo only makes up about 2% of total freight by volume, it accounts for 45-50% of the total value of freight transported. The presentation also examines trends in domestic versus international air cargo, finding that international demand is growing more dramatically, especially in Asian markets. It concludes that demand for air cargo services continues to grow internationally and that industry members and governments need to further open markets to meet shipper needs globally.

![Algemeneintroducie dh llogistics[1]](https://cdn.slidesharecdn.com/ss_thumbnails/algemeneintroduciedhllogistics1-100904035133-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)