Adjustment in final accounts

•Download as PPTX, PDF•

3 likes•2,615 views

The document discusses various adjustments that need to be made in final accounts, including expenses owing, prepaid expenses, accrued income, income received in advance, depreciation, and bad debts. Expenses owing are expenses incurred during the year but not yet paid, and are shown as a current liability. Prepaid expenses are expenses paid during the year that relate to the next year, and are shown as a current asset. Accrued income is income earned during the year but not yet received, and is added to income as a current asset. Income received in advance is income received for the next year, and is deducted from income as a current liability. Depreciation and bad debts are expenses deducted from assets.

Report

Share

Report

Share

Recommended

accounting for management

The document discusses various types of adjustments that may be needed when preparing final accounts at the end of an accounting period. These include closing stock, outstanding expenses, prepaid expenses, depreciation, bad debts, and others. For each adjustment, the document explains how to record the adjustment entry in the final accounts, including impacts to the trading account, profit and loss account, and balance sheet.

Adjustments to final accounts

An introductory slide on how to adjust for bad debts,provision for doubtful debts and provision for cash discounts

Final account adjustment

The Trial Balance is a statement of ledger account balances as on a particular date (instance).

Final Accounting is done towards the end of the accounting period.

The trial balance that we consider in the preparation of final accounts is the one that is prepared towards the end of the accounting period i.e. on the last day of the accounting period.

There might be a number of accounting transactions which might not have been taken into consideration by the time the Trial Balance has been prepared.

The transactions which have not yet been journalized, appended to the trial balance are what we call adjustments.

Any irrecoverable portion of sundry debtors is termed as bad debts. Bad debt is a loss to the business. If it is given in the Trial balance, it should be shown on the debit side of Profit & Loss Account. Bad debts given in the adjustment is to be deducted from sundry debtors in the Balance Sheet and the same is debited to the Profit & Loss Account.

Final accounts - Adjustments

This document outlines various accounting adjustments that may be needed when preparing final accounts, including the first and second effects of each adjustment. Some key adjustments include closing stock, which credits trading and assets the balance sheet; outstanding expenses, which debits trading/profit & loss and liabilities the balance sheet; and depreciation, which debits profit & loss and assets the balance sheet by deducting from the asset value.

Final Accounts adjustments

This document discusses various accounting adjustments needed to accurately determine a company's financial performance and position. It explains how to record adjustments for inventory valuation, prepaid and accrued expenses, uncollectible accounts, insurance claims, goods distributed as samples, goods withdrawn by the proprietor, and purchases and sales on credit. Adjustments are made through journal entries, with one entry to an income statement account and a corresponding entry to an asset or liability on the balance sheet. This ensures expenses and revenues are properly matched and assets and liabilities are accurately reported on the financial statements.

Final account ppt

This PPT is for Students of 11th, 12th and BBA. This ppt includes basic information for Final Account.

Account final account

This document discusses the preparation of final accounts, which involves the trading account, profit and loss account, and balance sheet. The trading account is used to calculate gross profit and loss. The profit and loss account calculates net profit or loss. The balance sheet shows sources of funds and their utilization. The document also discusses the treatment of various adjustments like outstanding expenses, prepaid expenses, depreciation, and their impact on the final accounts. Preparing final accounts is essential for organizations to understand their actual performance.

Accounts

This document provides information to prepare final accounts with adjustments for Ravinder, including:

1. The Trial Balance is given for Ravinder with various account balances.

2. Additional adjustments are provided, including manager's commission calculated as 10% of net profits before commission.

3. Interest on a 12% loan taken on July 1, 1987 is to be calculated and any outstanding amount adjusted.

4. Goods worth Rs. 1,500 taken by the proprietor for personal use requires an adjustment.

The student is to prepare the Trading and Profit & Loss Account, Balance Sheet, and make the necessary adjustments based on the Trial Balance and additional information given.

Recommended

accounting for management

The document discusses various types of adjustments that may be needed when preparing final accounts at the end of an accounting period. These include closing stock, outstanding expenses, prepaid expenses, depreciation, bad debts, and others. For each adjustment, the document explains how to record the adjustment entry in the final accounts, including impacts to the trading account, profit and loss account, and balance sheet.

Adjustments to final accounts

An introductory slide on how to adjust for bad debts,provision for doubtful debts and provision for cash discounts

Final account adjustment

The Trial Balance is a statement of ledger account balances as on a particular date (instance).

Final Accounting is done towards the end of the accounting period.

The trial balance that we consider in the preparation of final accounts is the one that is prepared towards the end of the accounting period i.e. on the last day of the accounting period.

There might be a number of accounting transactions which might not have been taken into consideration by the time the Trial Balance has been prepared.

The transactions which have not yet been journalized, appended to the trial balance are what we call adjustments.

Any irrecoverable portion of sundry debtors is termed as bad debts. Bad debt is a loss to the business. If it is given in the Trial balance, it should be shown on the debit side of Profit & Loss Account. Bad debts given in the adjustment is to be deducted from sundry debtors in the Balance Sheet and the same is debited to the Profit & Loss Account.

Final accounts - Adjustments

This document outlines various accounting adjustments that may be needed when preparing final accounts, including the first and second effects of each adjustment. Some key adjustments include closing stock, which credits trading and assets the balance sheet; outstanding expenses, which debits trading/profit & loss and liabilities the balance sheet; and depreciation, which debits profit & loss and assets the balance sheet by deducting from the asset value.

Final Accounts adjustments

This document discusses various accounting adjustments needed to accurately determine a company's financial performance and position. It explains how to record adjustments for inventory valuation, prepaid and accrued expenses, uncollectible accounts, insurance claims, goods distributed as samples, goods withdrawn by the proprietor, and purchases and sales on credit. Adjustments are made through journal entries, with one entry to an income statement account and a corresponding entry to an asset or liability on the balance sheet. This ensures expenses and revenues are properly matched and assets and liabilities are accurately reported on the financial statements.

Final account ppt

This PPT is for Students of 11th, 12th and BBA. This ppt includes basic information for Final Account.

Account final account

This document discusses the preparation of final accounts, which involves the trading account, profit and loss account, and balance sheet. The trading account is used to calculate gross profit and loss. The profit and loss account calculates net profit or loss. The balance sheet shows sources of funds and their utilization. The document also discusses the treatment of various adjustments like outstanding expenses, prepaid expenses, depreciation, and their impact on the final accounts. Preparing final accounts is essential for organizations to understand their actual performance.

Accounts

This document provides information to prepare final accounts with adjustments for Ravinder, including:

1. The Trial Balance is given for Ravinder with various account balances.

2. Additional adjustments are provided, including manager's commission calculated as 10% of net profits before commission.

3. Interest on a 12% loan taken on July 1, 1987 is to be calculated and any outstanding amount adjusted.

4. Goods worth Rs. 1,500 taken by the proprietor for personal use requires an adjustment.

The student is to prepare the Trading and Profit & Loss Account, Balance Sheet, and make the necessary adjustments based on the Trial Balance and additional information given.

Final Account Adjustments

Balance Sheet Inc is a leading tax service provider in the West Palm Beach area. Having an experience of more than 26 years on our side, we have been providing exceptional services to our client in preparing and filling forms to strategic tax planning. We also offer audit related services and can also represent you before IRS cases of audit and collection.

Some of our tax services are

1. Payroll returns

2. Individual Income

3. Business

4. Non Profit Returns

5. Offers in compromise

6. Direct IRS Communication

So, whether you hate preparing your tax returns or find taxes to be time consuming, we can help you out. We can also help you if you need 100% accuracy in your taxes or are facing issues related with IRS debt/audit.

Adjustments of Final Accounts

The different types of adjustments that should be made in the preparation of final accounts are given and how the how the adjustment should be treated.

Final Account

This document summarizes the final steps in the accounting process. It includes preparing a trial balance to check account balances, a trading profit and loss account to determine profit or loss, and a balance sheet to present the company's financial position by listing assets, liabilities, and capital. The document provides an example trial balance, shows the calculations to prepare a profit and loss statement, and presents an illustrated balance sheet. The final accounts are the last step of the accounting cycle and ensure the accuracy of the financial records.

Final accounts adjustments- students

The document discusses various adjustments that need to be made at the end of the accounting period before preparing the final accounts. These include adjustments for prepaid expenses, outstanding expenses, unearned revenue, accrued income, provisions for doubtful debts and discounts, depreciation, goods distributed as free samples, and loss from fire. The adjustments involve debiting/crediting relevant accounts in the trading, profit and loss accounts and reclassifying related balances in the balance sheet.

Introduction to final accounts

This document introduces the key financial statements prepared at the end of an accounting period: the trading account, profit and loss account, and balance sheet. It explains that the trial balance is prepared first using debit and credit columns to show asset/expense and liability/income balances. The trading account calculates gross profit by subtracting the cost of goods sold from net sales. The profit and loss account then calculates net profit by subtracting total expenses from total profits including gross profit and other income. Finally, the balance sheet presents the financial position by showing assets, liabilities, and capital/net assets.

Final Accounts of a Sole Trade Business

This document provides instructions for preparing final accounting statements, including a profit and loss account and balance sheet. It defines key terms like gross profit, cost of goods sold, direct expenses, and indirect expenses. It explains how to prepare a trading and profit and loss account, showing gross profit, expenses, net profit or loss. It also defines current and fixed assets and notes that a balance sheet shows the financial position of a business by reporting asset and liability balances. The overall purpose is to explain the accounting cycle and the process of preparing final accounting statements.

Final account

Final accounts refers to a company's financial position at the end of its accounting period, usually a year. At the end of the period, a company prepares final accounts including a trading account, profit and loss account, and balance sheet to understand if it made a profit or loss. The trading and profit and loss accounts calculate gross and net profits/losses based on accounting principles for a specified period. The balance sheet recognizes assets and liabilities on a specified date and defines items such as non-current assets, intangible assets, current assets, current and long-term liabilities, working capital, and capital employed and owned, showing their interrelationships.

Topic 9 final accounts

Learner will be able to prepare final statement of a business - Profit and loss account and Balance Sheet

Final acc

The trial balance provides financial information for Jain Bros as of March 31, 2006. Key figures include:

- Gross sales of Rs. 4,30,950 and purchases of Rs. 2,47,400

- Opening stock of Rs. 18,000 and creditors of Rs. 24,000

- Fixed assets including freehold property of Rs. 2,10,000, plant and machinery of Rs. 3,80,000, and computers of Rs. 1,22,000

- Capital account of Rs. 6,50,000 and bank overdraft of Rs. 16,500

Final account

The document provides information about the final steps in the accounting process which include preparing final accounts such as trading account, profit and loss account, and balance sheet. It explains that these final accounts are needed to determine the profit or loss for the year and the year-end financial position of the business. The document then goes into detail about how to prepare each of these final accounts, the key components that make up each account, and various adjustments and accounting entries needed to accurately capture the financial activities and position of the business.

Final accounts of banks & companies

The document discusses the key aspects of final accounts of banks and companies. It explains that final accounts comprise the income statement (trading and profit & loss account) and balance sheet. It provides details on various expenses like direct, indirect, administrative etc. It also discusses elements of assets and liabilities like fixed assets, current assets, owners' funds, reserves, secured and unsecured loans. Key adjustments in final accounts like closing stock, outstanding expenses, depreciation etc. are also summarized.

Presentation on Final Accounts- SOMS, TU

This document provides an overview of key concepts related to final accounts, including manufacturing account, trading account, profit and loss account, and balance sheet. It discusses the purpose and treatment of various adjustments that must be considered when preparing final accounts, such as prepaid expenses, accrued income, depreciation, and provisions. The document also explains common transactions like insurance claims, appropriation of profit to reserves, and manager's commission. Overall, it serves as a guide to understanding the accounting process for finalizing financial statements at the end of an accounting period.

Adjustments to the final accounts of business organisations 12

This document discusses adjustments made to business accounts, including capital vs revenue expenditures and incomes, accruals and prepayments, bad debts, depreciation, and provisions for doubtful debts. Capital expenditures are expenses related to long-term assets that are capitalized on the balance sheet rather than expensed immediately. Revenue expenditures are day-to-day operating costs that are expensed in the period incurred. Accruals and prepayments ensure expenses and revenues are recorded in the appropriate period based on when they are incurred rather than when payment is made. Bad debts are customer balances written off as uncollectible, while provisions for doubtful debts account for expected future bad debts.

Final account trading account pl acc balance sheet

The document provides details about the final accounts process in accounting. It explains that final accounts include the preparation of trading, profit & loss, and balance sheet statements. These statements are prepared from the trial balance to determine the profit/loss for the year and the year-end financial position. The document outlines the key components of the trading account, profit & loss account, and balance sheet, and provides examples of their format and various adjustments made in their preparation.

Adjusting entries

Adjusting entries are used to match expenses and revenues to the correct accounting period. There are two types of adjustments - accruals and deferrals. Accruals recognize revenues or expenses that were earned or incurred in the current period but not yet recorded, like accrued interest. Deferrals move revenues or expenses that were already recorded to the proper period, like prepaid insurance being moved to the period of coverage. Adjusting entries are journal entries posted to the general ledger at the end of each period to ensure accurate financial reporting.

Final accounts

The document provides study notes on final accounts, including trading account, profit and loss account, and balance sheet.

It defines final accounts as the set of financial statements that include a trading account, profit and loss account, and balance sheet. The trading account shows gross profit or loss, the profit and loss account shows net profit or loss, and the balance sheet shows the financial position of the business.

Specimen templates are provided for a trading account, profit and loss account, and balance sheet. Key features and purposes of each statement are also summarized, such as the trading account determining gross profit/loss, the profit and loss account determining net profit/loss, and the balance sheet showing assets, liabilities, and

Final accounts

The document summarizes the key steps in preparing final accounts from a trial balance:

1. The final accounts include a trading account, profit and loss account, and balance sheet. These are prepared using figures from the trial balance.

2. Items in the trial balance are written against the final account(s) in which they appear. Each item is only used once.

3. Closing stock does not appear in the trial balance but is noted separately. It is used twice - in the trading account and balance sheet.

4. Preparing the final accounts involves transferring figures from the double-entry accounts to the appropriate statement, using the trial balance as a summary.

Final accounts

- The document discusses key steps in the accounting process including preparing trial balance, final accounts (trading account, profit & loss account, balance sheet), and various adjustments needed for the financial statements.

- It provides examples and explanations of key final account components like trading account, profit & loss account, balance sheet, and adjustments for closing stock, outstanding expenses, prepaid expenses, accrued income, and more.

- The purpose is to explain how to close accounts and prepare final financial statements that show the profit/loss for the period and current financial position.

Adjusting Entries

Adjusting entries are journal entries made at the end of an accounting period to allocate revenues and expenses to the appropriate period. This is necessary because under the accrual basis of accounting, revenues are reported in the period they are earned and expenses in the period they are incurred. Some accounts, like prepaid expenses and unearned revenue, require adjustment to adhere to the revenue recognition and matching principles. The document provides examples of accounts that need adjustment, the cash versus accrual accounting methods, and the purpose of adjusting entries in ensuring financial statements reflect the proper period's financial activity.

5. FINAL ACCOUNTS WITH ADJUSTMENTS.pptx

The document discusses various accounting adjustments that may be required before finalizing financial statements at the end of an accounting period. Some key adjustments mentioned include closing stock, outstanding expenses, prepaid expenses, accrued income, unearned income, depreciation, bad debts, and provisions. The effects of each adjustment on the trading account, profit and loss account, and balance sheet are explained. Common adjustments like interest on capital, drawings, and loans are also covered. The purpose of adjustments is to determine the true profit/loss for the period and accurate financial position of the business.

Final account

The document discusses the three main financial statements prepared during the final accounting process:

1) The trading account determines gross profit or loss and includes only direct expenses and revenues.

2) The profit and loss account determines net profit or loss and includes indirect expenses and revenues. It begins with the trading account balance.

3) The balance sheet discloses total assets, liabilities, and capital on a given date. It includes adjustments for prepaid/accrued items and closing balances from other statements.

Accounting cycle

The accounting cycle is a series of steps to record, classify, and summarize a business's financial transactions over an accounting period. It begins with analyzing transactions and recording them in a journal. The journal entries are then posted to ledger accounts, where balances are calculated. An unadjusted trial balance lists the ledger account balances before adjusting entries. Adjusting entries follow accrual accounting principles. The adjusted trial balance incorporates these adjustments. Finally, closing entries transfer temporary account balances to permanent accounts, allowing preparation of financial statements from the post-closing trial balance.

More Related Content

What's hot

Final Account Adjustments

Balance Sheet Inc is a leading tax service provider in the West Palm Beach area. Having an experience of more than 26 years on our side, we have been providing exceptional services to our client in preparing and filling forms to strategic tax planning. We also offer audit related services and can also represent you before IRS cases of audit and collection.

Some of our tax services are

1. Payroll returns

2. Individual Income

3. Business

4. Non Profit Returns

5. Offers in compromise

6. Direct IRS Communication

So, whether you hate preparing your tax returns or find taxes to be time consuming, we can help you out. We can also help you if you need 100% accuracy in your taxes or are facing issues related with IRS debt/audit.

Adjustments of Final Accounts

The different types of adjustments that should be made in the preparation of final accounts are given and how the how the adjustment should be treated.

Final Account

This document summarizes the final steps in the accounting process. It includes preparing a trial balance to check account balances, a trading profit and loss account to determine profit or loss, and a balance sheet to present the company's financial position by listing assets, liabilities, and capital. The document provides an example trial balance, shows the calculations to prepare a profit and loss statement, and presents an illustrated balance sheet. The final accounts are the last step of the accounting cycle and ensure the accuracy of the financial records.

Final accounts adjustments- students

The document discusses various adjustments that need to be made at the end of the accounting period before preparing the final accounts. These include adjustments for prepaid expenses, outstanding expenses, unearned revenue, accrued income, provisions for doubtful debts and discounts, depreciation, goods distributed as free samples, and loss from fire. The adjustments involve debiting/crediting relevant accounts in the trading, profit and loss accounts and reclassifying related balances in the balance sheet.

Introduction to final accounts

This document introduces the key financial statements prepared at the end of an accounting period: the trading account, profit and loss account, and balance sheet. It explains that the trial balance is prepared first using debit and credit columns to show asset/expense and liability/income balances. The trading account calculates gross profit by subtracting the cost of goods sold from net sales. The profit and loss account then calculates net profit by subtracting total expenses from total profits including gross profit and other income. Finally, the balance sheet presents the financial position by showing assets, liabilities, and capital/net assets.

Final Accounts of a Sole Trade Business

This document provides instructions for preparing final accounting statements, including a profit and loss account and balance sheet. It defines key terms like gross profit, cost of goods sold, direct expenses, and indirect expenses. It explains how to prepare a trading and profit and loss account, showing gross profit, expenses, net profit or loss. It also defines current and fixed assets and notes that a balance sheet shows the financial position of a business by reporting asset and liability balances. The overall purpose is to explain the accounting cycle and the process of preparing final accounting statements.

Final account

Final accounts refers to a company's financial position at the end of its accounting period, usually a year. At the end of the period, a company prepares final accounts including a trading account, profit and loss account, and balance sheet to understand if it made a profit or loss. The trading and profit and loss accounts calculate gross and net profits/losses based on accounting principles for a specified period. The balance sheet recognizes assets and liabilities on a specified date and defines items such as non-current assets, intangible assets, current assets, current and long-term liabilities, working capital, and capital employed and owned, showing their interrelationships.

Topic 9 final accounts

Learner will be able to prepare final statement of a business - Profit and loss account and Balance Sheet

Final acc

The trial balance provides financial information for Jain Bros as of March 31, 2006. Key figures include:

- Gross sales of Rs. 4,30,950 and purchases of Rs. 2,47,400

- Opening stock of Rs. 18,000 and creditors of Rs. 24,000

- Fixed assets including freehold property of Rs. 2,10,000, plant and machinery of Rs. 3,80,000, and computers of Rs. 1,22,000

- Capital account of Rs. 6,50,000 and bank overdraft of Rs. 16,500

Final account

The document provides information about the final steps in the accounting process which include preparing final accounts such as trading account, profit and loss account, and balance sheet. It explains that these final accounts are needed to determine the profit or loss for the year and the year-end financial position of the business. The document then goes into detail about how to prepare each of these final accounts, the key components that make up each account, and various adjustments and accounting entries needed to accurately capture the financial activities and position of the business.

Final accounts of banks & companies

The document discusses the key aspects of final accounts of banks and companies. It explains that final accounts comprise the income statement (trading and profit & loss account) and balance sheet. It provides details on various expenses like direct, indirect, administrative etc. It also discusses elements of assets and liabilities like fixed assets, current assets, owners' funds, reserves, secured and unsecured loans. Key adjustments in final accounts like closing stock, outstanding expenses, depreciation etc. are also summarized.

Presentation on Final Accounts- SOMS, TU

This document provides an overview of key concepts related to final accounts, including manufacturing account, trading account, profit and loss account, and balance sheet. It discusses the purpose and treatment of various adjustments that must be considered when preparing final accounts, such as prepaid expenses, accrued income, depreciation, and provisions. The document also explains common transactions like insurance claims, appropriation of profit to reserves, and manager's commission. Overall, it serves as a guide to understanding the accounting process for finalizing financial statements at the end of an accounting period.

Adjustments to the final accounts of business organisations 12

This document discusses adjustments made to business accounts, including capital vs revenue expenditures and incomes, accruals and prepayments, bad debts, depreciation, and provisions for doubtful debts. Capital expenditures are expenses related to long-term assets that are capitalized on the balance sheet rather than expensed immediately. Revenue expenditures are day-to-day operating costs that are expensed in the period incurred. Accruals and prepayments ensure expenses and revenues are recorded in the appropriate period based on when they are incurred rather than when payment is made. Bad debts are customer balances written off as uncollectible, while provisions for doubtful debts account for expected future bad debts.

Final account trading account pl acc balance sheet

The document provides details about the final accounts process in accounting. It explains that final accounts include the preparation of trading, profit & loss, and balance sheet statements. These statements are prepared from the trial balance to determine the profit/loss for the year and the year-end financial position. The document outlines the key components of the trading account, profit & loss account, and balance sheet, and provides examples of their format and various adjustments made in their preparation.

Adjusting entries

Adjusting entries are used to match expenses and revenues to the correct accounting period. There are two types of adjustments - accruals and deferrals. Accruals recognize revenues or expenses that were earned or incurred in the current period but not yet recorded, like accrued interest. Deferrals move revenues or expenses that were already recorded to the proper period, like prepaid insurance being moved to the period of coverage. Adjusting entries are journal entries posted to the general ledger at the end of each period to ensure accurate financial reporting.

Final accounts

The document provides study notes on final accounts, including trading account, profit and loss account, and balance sheet.

It defines final accounts as the set of financial statements that include a trading account, profit and loss account, and balance sheet. The trading account shows gross profit or loss, the profit and loss account shows net profit or loss, and the balance sheet shows the financial position of the business.

Specimen templates are provided for a trading account, profit and loss account, and balance sheet. Key features and purposes of each statement are also summarized, such as the trading account determining gross profit/loss, the profit and loss account determining net profit/loss, and the balance sheet showing assets, liabilities, and

Final accounts

The document summarizes the key steps in preparing final accounts from a trial balance:

1. The final accounts include a trading account, profit and loss account, and balance sheet. These are prepared using figures from the trial balance.

2. Items in the trial balance are written against the final account(s) in which they appear. Each item is only used once.

3. Closing stock does not appear in the trial balance but is noted separately. It is used twice - in the trading account and balance sheet.

4. Preparing the final accounts involves transferring figures from the double-entry accounts to the appropriate statement, using the trial balance as a summary.

Final accounts

- The document discusses key steps in the accounting process including preparing trial balance, final accounts (trading account, profit & loss account, balance sheet), and various adjustments needed for the financial statements.

- It provides examples and explanations of key final account components like trading account, profit & loss account, balance sheet, and adjustments for closing stock, outstanding expenses, prepaid expenses, accrued income, and more.

- The purpose is to explain how to close accounts and prepare final financial statements that show the profit/loss for the period and current financial position.

Adjusting Entries

Adjusting entries are journal entries made at the end of an accounting period to allocate revenues and expenses to the appropriate period. This is necessary because under the accrual basis of accounting, revenues are reported in the period they are earned and expenses in the period they are incurred. Some accounts, like prepaid expenses and unearned revenue, require adjustment to adhere to the revenue recognition and matching principles. The document provides examples of accounts that need adjustment, the cash versus accrual accounting methods, and the purpose of adjusting entries in ensuring financial statements reflect the proper period's financial activity.

What's hot (19)

Adjustments to the final accounts of business organisations 12

Adjustments to the final accounts of business organisations 12

Final account trading account pl acc balance sheet

Final account trading account pl acc balance sheet

Similar to Adjustment in final accounts

5. FINAL ACCOUNTS WITH ADJUSTMENTS.pptx

The document discusses various accounting adjustments that may be required before finalizing financial statements at the end of an accounting period. Some key adjustments mentioned include closing stock, outstanding expenses, prepaid expenses, accrued income, unearned income, depreciation, bad debts, and provisions. The effects of each adjustment on the trading account, profit and loss account, and balance sheet are explained. Common adjustments like interest on capital, drawings, and loans are also covered. The purpose of adjustments is to determine the true profit/loss for the period and accurate financial position of the business.

Final account

The document discusses the three main financial statements prepared during the final accounting process:

1) The trading account determines gross profit or loss and includes only direct expenses and revenues.

2) The profit and loss account determines net profit or loss and includes indirect expenses and revenues. It begins with the trading account balance.

3) The balance sheet discloses total assets, liabilities, and capital on a given date. It includes adjustments for prepaid/accrued items and closing balances from other statements.

Accounting cycle

The accounting cycle is a series of steps to record, classify, and summarize a business's financial transactions over an accounting period. It begins with analyzing transactions and recording them in a journal. The journal entries are then posted to ledger accounts, where balances are calculated. An unadjusted trial balance lists the ledger account balances before adjusting entries. Adjusting entries follow accrual accounting principles. The adjusted trial balance incorporates these adjustments. Finally, closing entries transfer temporary account balances to permanent accounts, allowing preparation of financial statements from the post-closing trial balance.

How to-solve-difficult-adjustments-and-journal-entries-in-financial-accounts-...

This document provides explanations and examples of accounting journal entries for various financial transactions including adjustments. It discusses entries for bad debts, provision for doubtful debts, rent and rent outstanding, income tax payments, indirect taxes, cash withdrawals, asset purchases and sales, expenses, revenues, and other common accounting topics. The document emphasizes applying the rules of double-entry accounting and selecting the appropriate debit and credit accounts based on whether an item is related to a personal, real, or nominal account.

The accounting cycle

The document discusses the accounting cycle and financial reporting process. It covers the key steps:

1. Preparing the basic financial statements - the balance sheet, income statement, and statement of retained earnings.

2. Making closing entries to reset temporary accounts to zero at the end of the period. This involves transferring account balances to income summary and then to retained earnings.

3. Evaluating the business performance using liquidity and profitability ratios calculated from the financial statements.

Bba i ita u 5.1 accounting for non-trading concern

This document discusses accounting procedures for non-trading concerns such as clubs, educational institutions, and societies. It explains that proper accounting avoids misappropriation of members' money. It describes how to prepare receipts and payments accounts, income and expenditure accounts, and the differences between income and expenditure. It provides guidance on preparing income and expenditure accounts from receipts and payments accounts, including treatment of various revenue and capital items, depreciation, gains and losses. Accounting procedures are important even for non-profit organizations to ensure accurate financial reporting.

FINAL Accounts.pptx

Final accounts include trading and profit and loss accounts and a balance sheet. They are prepared at the end of an accounting year to determine the profit or loss and financial position of a company.

The trading account shows the gross profit or loss from trading activities like purchases and sales. The profit and loss account determines the net profit or loss after deducting all expenses from income. The balance sheet lists the assets, liabilities, and capital as of a certain date to show the financial position.

Preparing final accounts involves making adjustments for prepaid expenses, outstanding expenses, closing stock, depreciation, and other items to accurately reflect the company's performance and position.

Powerpoint 3rev1

The document provides an overview of basic accounting concepts and procedures. It explains that accounting involves recording business transactions, adjusting account balances, and preparing financial statements. Key steps include journalizing transactions, posting to ledger accounts, taking a trial balance, compiling adjustment data, preparing a worksheet, making adjustments, and generating financial statements. The accounting equation, types of accounts, debit/credit rules, and accounting cycle are also outlined.

Xii acc chapter 1 Income and Expenditure Account

How to prepare Income and Expenditure Account and Differences between Receipt and Payment account and Income and Expenditure account

Types ofmajoraccounting

The document defines the five major types of accounts: assets, liabilities, equity, income, and expenses. Assets are resources owned by a business. Liabilities are obligations of a business. Equity represents the owner's claim and is a residual interest calculated by deducting liabilities from assets. Income increases equity and expenses decrease equity. Current assets are expected to convert to cash within one year while non-current assets are long-term. Similarly, current liabilities are due within one year and non-current liabilities are long-term.

Financial accounting

This presentation is based on the subject Financial Accounting which helps the beginners to know the basic concept of accounting . This is according to the syllabus of Pt. Ravishankar University , Raipur and Durg University, Durg.

Ac process

The document discusses key accounting concepts including the accounting equation, accounting cycle, adjusting entries, trial balance, financial statements, and closing process. It provides examples to illustrate preparing adjusting entries for prepaid expenses, accrued liabilities, depreciation, and estimates. It also discusses the use of worksheets, reversing entries, subsidiary ledgers, and special journals.

Bca i fma u 2 final account

The document discusses final accounts and their importance in accounting. It explains that final accounts like trading account, profit and loss account, and balance sheet are prepared from the trial balance and provide key financial information. The trading account shows gross profit or loss, while the profit and loss account provides net profit or loss. The balance sheet presents the assets and liabilities of the business at a point in time. Adjustment entries and the worksheet help ensure accurate preparation of final accounts.

Mca i fma u 2 final account

The document discusses the preparation of final accounts, which provide information on the profit/loss and financial position of a business. It describes the objectives and components of final accounts, including trading account, profit and loss account, and balance sheet. It explains the purpose of each account, the key items included on their debit and credit sides, and their importance. It also covers topics like adjustment entries, manufacturing account, and the use of a worksheet to prepare adjusted trial balance for the final accounts.

Presentation on Final Accounts

This document provides an overview of key concepts related to final accounts, including manufacturing account, trading account, profit and loss account, and balance sheet. It discusses the purpose and treatment of various adjustments that must be considered when preparing final accounts, such as prepaid expenses, accrued income, depreciation, and provisions. The document also explains common transactions like insurance claims, appropriation of profit to reserves, and manager's commission. Overall, it serves as a guide to understanding the accounting process for finalizing financial statements at the end of an accounting period.

Balance sheet

This document provides an overview of balance sheet analysis and profit and loss account concepts. It discusses the key components of the balance sheet including sources of funds like capital, reserves, and liabilities, and uses of funds like fixed assets, current assets, and intangible assets. It also covers the key line items in a profit and loss account, such as gross sales, cost of goods sold, operating profit, and net profit. Notes are provided on accounting conventions and qualitative factors to consider in analyzing financial statements.

Caiib fmmodbbsa nov08

This document provides an overview of balance sheet analysis and profit and loss account concepts. It discusses the key components of the balance sheet including sources of funds like capital, reserves, and liabilities, and uses of funds like fixed assets, current assets, and intangible assets. It also covers the key line items in a profit and loss statement including sales, cost of goods sold, operating expenses, operating profit, and net profit. Notes are provided on accounting conventions and qualitative factors to consider in analyzing financial statements.

Bba i ita u 3 final account

The document discusses the preparation of final accounts, which provide key financial information about a business. It describes the objectives and components of final accounts, including the trading account, profit and loss account, balance sheet, and manufacturing account. It outlines the items and format of each account, and explains the importance and purpose of preparing a worksheet to help prevent errors in compiling the final accounts from the trial balance.

Financial statement analysis

Financial statement analysis (or financial analysis) is the process of reviewing and analyzing a company's financial statements to make better economic decisions. These statements include the income statement, balance sheet, statement of cash flows, and a statement of changes in equity.

BKMSH Introduction to Income Statement

Financial statements are used by managers, shareholders, investors, lenders, and the government for different reasons and purposes. Essentially, financial statements show the financial status of an entity and are comprised of income statement, balance sheet, and cash flow statement.

Similar to Adjustment in final accounts (20)

How to-solve-difficult-adjustments-and-journal-entries-in-financial-accounts-...

How to-solve-difficult-adjustments-and-journal-entries-in-financial-accounts-...

Bba i ita u 5.1 accounting for non-trading concern

Bba i ita u 5.1 accounting for non-trading concern

More from Shubhrat Sharma

Statistical tools in research

marketing research statistical tools. hypothesis testing, factor analysis,correlation, regression, chi square test

Top Indian Advertisement Agencies

Advertisement agencies of India Rated for the year 2010-13.

and include various ad campaigns by them and brief introduction.

Crm Activities by SBI

The presentation is about the CRM activities of SBI. This ppt also provide various statistics on why CRM is importance.

Service marketing (demand & capacity,pricing and distribution)

demand and capacity management of services, pricing a service and distribution of service. service marketing

Managing inventory and work

it gives an insight about how to manage work and inventory in the industry, also discuss about the productivity and efficiency in the industry.

Amazon.com vs flipkart.com

Amazon and Flipkart are two major online retailers in India. Amazon was founded in 1994 by Jeff Bezos and is now a global company headquartered in Seattle. Flipkart was founded in 2007 by Sachin and Binny Bansal and is headquartered in Bangalore. Both companies started as online book retailers and have now diversified into various product categories. They have grown significantly through acquisitions and innovations such as fast delivery and easy return policies. However, Amazon maintains an edge through superior pricing and customer experience.

Human capital and its various trends

The presentation is about Human Capital, difference between capital n resource , new trend in human capital and also its about human resource management analogy with financial management. it also find out the reason by their was reason to human capital management

Motivation Theories

This document discusses different theories of motivation. It defines motivation and describes three main categories of motivational theories: internal theories that focus on individual factors, process theories that emphasize interactions between individuals and the environment, and external theories that focus on environmental elements. Two prominent motivation theories are discussed in more detail: Maslow's hierarchy of needs theory, which proposes that individuals must satisfy lower-level needs before pursuing higher needs; and expectancy theory, which suggests that motivation depends on expectations of effort leading to performance and performance leading to outcomes. The document also outlines Herzberg's two-factor theory of motivation and hygiene factors.

Production insight

Numerical control (NC) is a programmable automation method that uses coded alphanumeric data to control the relative positions of a machine tool's work head and work part. NC allows complex part geometries to be machined through programs that direct linear and rotational axis movement. Common NC machine tools are milling machines, lathes, and drilling machines. NC programs can be stored, edited, and run on NC controllers connected to individual machine tools or through a central computer on a networked system.

coordination

defining coordination

requisites of coordination

features of coordination

sign and symptoms of lack of coordination

(view in slide show for better viewing)

Normal distribution

This document discusses key properties of several probability distributions including the binomial, Poisson, and normal distributions. It explains that the binomial distribution is defined by the number of trials (n) and probability of success (p), while the Poisson distribution is defined solely by its mean. The normal distribution is then described as being defined by its mean and standard deviation. It proceeds to outline several distinguishing features of the normal distribution, including being unimodal, symmetrical, and asymptotic.

Subliminal advertising

This document discusses subliminal messaging and advertising. It explains that subliminal messages are hidden messages that influence people's subconscious minds without their conscious awareness. The document notes that while subliminal advertising was common in the mid-20th century, it was banned in the 1970s because people were concerned it could wrongly influence their brains. Subliminal messages can be delivered through various senses like sight, sound, and smell to subtly influence consumer behavior and opinions.

More from Shubhrat Sharma (12)

Service marketing (demand & capacity,pricing and distribution)

Service marketing (demand & capacity,pricing and distribution)

Recently uploaded

在线办理(UVic毕业证书)维多利亚大学毕业证录取通知书一模一样

学校原件一模一样【微信:741003700 】《(UVic毕业证书)维多利亚大学毕业证》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

20240608 QFM019 Engineering Leadership Reading List May 2024

Everything I found interesting about Engineering Leadership in May 2024

12 steps to transform your organization into the agile org you deserve

During an organizational transformation, the shift is from the previous state to an improved one. In the realm of agility, I emphasize the significance of identifying polarities. This approach helps establish a clear understanding of your objectives. I have outlined 12 incremental actions to delineate your organizational strategy.

Enriching engagement with ethical review processes

New ethics review processes at the University of Bath. Presented at the 8th World Conference on Research Integrity by Filipa Vance, Head of Research Governance and Compliance at the University of Bath. June 2024, Athens

Addiction to Winning Across Diverse Populations.pdf

A anaysis dedicated to identify the addiction on winniing by diverse population

原版制作(澳洲WSU毕业证书)西悉尼大学毕业证文凭证书一模一样

学校原件一模一样【微信:741003700 】《(澳洲WSU毕业证书)西悉尼大学毕业证、文凭证书》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Comparing Stability and Sustainability in Agile Systems

Copy of the presentation given at XP2024 based on a research paper.

In this paper we explain wat overwork is and the physical and mental health risks associated with it.

We then explore how overwork relates to system stability and inventory.

Finally there is a call to action for Team Leads / Scrum Masters / Managers to measure and monitor excess work for individual teams.

Risk-Management-presentation for cooperatives

Power point presentation for risk management for cooperatives

Public Speaking Tips to Help You Be A Strong Leader.pdf

In the realm of effective leadership, a multitude of skills come into play, but one stands out as both crucial and challenging: public speaking.

Public speaking transcends mere eloquence; it serves as the medium through which leaders articulate their vision, inspire action, and foster engagement. For leaders, refining public speaking skills is essential, elevating their ability to influence, persuade, and lead with resolute conviction. Here are some key tips to consider: https://joellandau.com/the-public-speaking-tips-to-help-you-be-a-stronger-leader/

Ganpati Kumar Choudhary Indian Ethos PPT.pptx

Ganpati Kumar Choudhary Indian Ethos PPT.pptx, The Dilemma of Green Energy Corporation

Green Energy Corporation, a leading renewable energy company, faces a dilemma: balancing profitability and sustainability. Pressure to scale rapidly has led to ethical concerns, as the company's commitment to sustainable practices is tested by the need to satisfy shareholders and maintain a competitive edge.

Senior Project and Engineering Leader Jim Smith.pdf

I am a Project and Engineering Leader with extensive experience as a Business Operations Leader, Technical Project Manager, Engineering Manager and Operations Experience for Domestic and International companies such as Electrolux, Carrier, and Deutz. I have developed new products using Stage Gate development/MS Project/JIRA, for the pro-duction of Medical Equipment, Large Commercial Refrigeration Systems, Appliances, HVAC, and Diesel engines.

My experience includes:

Managed customized engineered refrigeration system projects with high voltage power panels from quote to ship, coordinating actions between electrical engineering, mechanical design and application engineering, purchasing, production, test, quality assurance and field installation. Managed projects $25k to $1M per project; 4-8 per month. (Hussmann refrigeration)

Successfully developed the $15-20M yearly corporate capital strategy for manufacturing, with the Executive Team and key stakeholders. Created project scope and specifications, business case, ROI, managed project plans with key personnel for nine consumer product manufacturing and distribution sites; to support the company’s strategic sales plan.

Over 15 years of experience managing and developing cost improvement projects with key Stakeholders, site Manufacturing Engineers, Mechanical Engineers, Maintenance, and facility support personnel to optimize pro-duction operations, safety, EHS, and new product development. (BioLab, Deutz, Caire)

Experience working as a Technical Manager developing new products with chemical engineers and packaging engineers to enhance and reduce the cost of retail products. I have led the activities of multiple engineering groups with diverse backgrounds.

Great experience managing the product development of products which utilize complex electrical controls, high voltage power panels, product testing, and commissioning.

Created project scope, business case, ROI for multiple capital projects to support electrotechnical assembly and CPG goods. Identified project cost, risk, success criteria, and performed equipment qualifications. (Carrier, Electrolux, Biolab, Price, Hussmann)

Created detailed projects plans using MS Project, Gant charts in excel, and updated new product development in Jira for stakeholders and project team members including critical path.

Great knowledge of ISO9001, NFPA, OSHA regulations.

User level knowledge of MRP/SAP, MS Project, Powerpoint, Visio, Mastercontrol, JIRA, Power BI and Tableau.

I appreciate your consideration, and look forward to discussing this role with you, and how I can lead your company’s growth and profitability. I can be contacted via LinkedIn via phone or E Mail.

Jim Smith

678-993-7195

jimsmith30024@gmail.com

原版制作(CDU毕业证书)查尔斯达尔文大学毕业证PDF成绩单一模一样

学校原件一模一样【微信:741003700 】《(CDU毕业证书)查尔斯达尔文大学毕业证PDF成绩单》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Integrity in leadership builds trust by ensuring consistency between words an...

Integrity in leadership builds trust by ensuring consistency between words and actions, making leaders reliable and credible. It also ensures ethical decision-making, which fosters a positive organizational culture and promotes long-term success. #RamVChary

Employment Practices

Regulation and Multinational Corporations

Employment Practices

Regulation and Multinational Corporations

Strategic decision making within MNCs constrained or determined by the implementation of laws and codes of practice and by pressure from political actors. Managers in MNCs have to make choices that are shaped by gvmt. intervention and the local economy.

Sethurathnam Ravi: A Legacy in Finance and Leadership

Sethurathnam Ravi, also known as S Ravi, is a distinguished Chartered Accountant and former Chairman of the Bombay Stock Exchange (BSE). As the Founder and Managing Partner of Ravi Rajan & Co. LLP, he has made significant contributions to the fields of finance, banking, and corporate governance. His extensive career includes directorships in over 45 major organizations, including LIC, BHEL, and ONGC. With a passion for financial consulting and social issues, S Ravi continues to influence the industry and inspire future leaders.

Strategic Org Design with Org Topologies™

Org Design is a core skill to be mastered by management for any successful org change.

Org Topologies™ in its essence is a two-dimensional space with 16 distinctive boxes - atomic organizational archetypes. That space helps you to plot your current operating model by positioning individuals, departments, and teams on the map. This will give a profound understanding of the performance of your value-creating organizational ecosystem.

The Management Guide: From Projects to Portfolio

A presentation on mastering key management concepts across projects, products, programs, and portfolios. Whether you're an aspiring manager or looking to enhance your skills, this session will provide you with the knowledge and tools to succeed in various management roles. Learn about the distinct lifecycles, methodologies, and essential skillsets needed to thrive in today's dynamic business environment.

在线办理(Murdoch毕业证书)莫道克大学毕业证电子版成绩单一模一样

学校原件一模一样【微信:741003700 】《(Murdoch毕业证书)莫道克大学毕业证电子版成绩单》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Recently uploaded (20)

20240608 QFM019 Engineering Leadership Reading List May 2024

20240608 QFM019 Engineering Leadership Reading List May 2024

12 steps to transform your organization into the agile org you deserve

12 steps to transform your organization into the agile org you deserve

CV Ensio Suopanki1.pdf ENGLISH Russian Finnish German

CV Ensio Suopanki1.pdf ENGLISH Russian Finnish German

Leadership Ethics and Change, Purpose to Impact Plan

Leadership Ethics and Change, Purpose to Impact Plan

Enriching engagement with ethical review processes

Enriching engagement with ethical review processes

Addiction to Winning Across Diverse Populations.pdf

Addiction to Winning Across Diverse Populations.pdf

Comparing Stability and Sustainability in Agile Systems

Comparing Stability and Sustainability in Agile Systems

Public Speaking Tips to Help You Be A Strong Leader.pdf

Public Speaking Tips to Help You Be A Strong Leader.pdf

Senior Project and Engineering Leader Jim Smith.pdf

Senior Project and Engineering Leader Jim Smith.pdf

Integrity in leadership builds trust by ensuring consistency between words an...

Integrity in leadership builds trust by ensuring consistency between words an...

Employment Practices

Regulation and Multinational Corporations

Employment Practices

Regulation and Multinational Corporations

Sethurathnam Ravi: A Legacy in Finance and Leadership

Sethurathnam Ravi: A Legacy in Finance and Leadership

Adjustment in final accounts

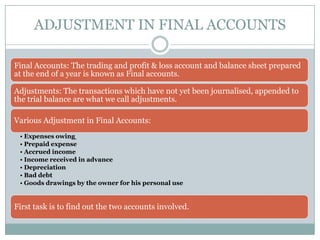

- 1. ADJUSTMENT IN FINAL ACCOUNTS Final Accounts: The trading and profit & loss account and balance sheet prepared at the end of a year is known as Final accounts. Adjustments: The transactions which have not yet been journalised, appended to the trial balance are what we call adjustments. Various Adjustment in Final Accounts: • Expenses owing • Prepaid expense • Accrued income • Income received in advance • Depreciation • Bad debt • Goods drawings by the owner for his personal use First task is to find out the two accounts involved.

- 2. Expenses - Outstanding/Prepaid •these are the expenses incurred during the year but not paid in cash •This amount will be paid in the near future (next year). •It is shown as current liability in balance sheets. •In two entry system: •Debit Expenses account •Credit Expenses owing account Outstanding expense: •This is the expense paid during the year for the benefit of the next year. •The portion of the expense which is prepaid is to be deducted from the total expenses already paid during the year •It is shown as current asset in the balance sheet. •In two entry system: •Debit Prepaid expense account and •Credit Expense account Prepaid expense:

- 3. Incomes - Outstanding/Pre-received •The income earned during the year but not received in cash is known as accrued income. •The amount of accrued income is to be considered as current year’s income and added with the concerned income received during the year •It is shown as current asset in balance sheet. •In double entry system: •Debit Accrued income account and •Credit Income account Outstanding Income: (Accrued income) •This is the income received during the year for the services to be rendered during the next year. •Since this income is not related to the current year, it should be deducted from the concerned income . •It is shown as current liability in balance sheet. •In double entry system: •Debit Income account and •Credit Income received in advance Pre-received Income:

- 4. Other Adjustments •The part of the cost of a fixed asset that is consumed by a business during the period of its use is known as depreciation. •It is considered as an expense in the business therefore shown as an expense in the profit & loss account . •It is deducted from the cost price of the concerned fixed asset in the balance sheet. •In double entry system: •Debit Profit & loss account and •Credit Depreciation account Depreciation: •The part of the amount of debtors which cannot be recovered is known as bad debt. •it is known as bad debt written off and shown in the profit & loss account only. •In the double entry system: •Debit Bad debt account and •Credit Debtors account Bad debt: