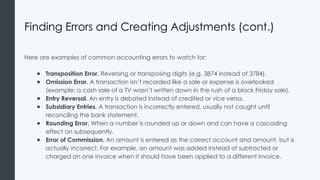

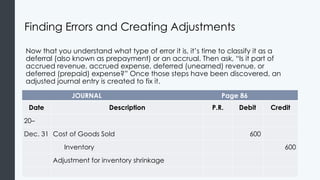

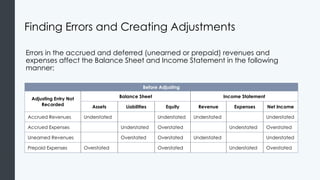

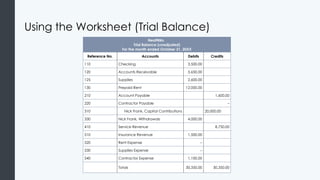

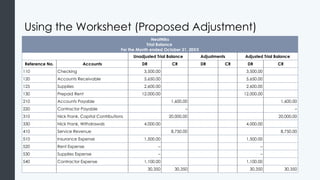

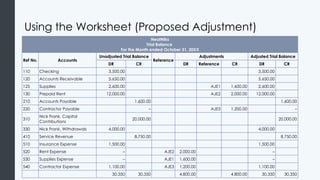

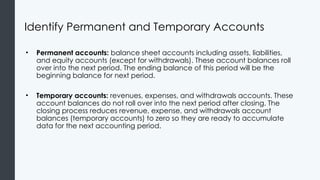

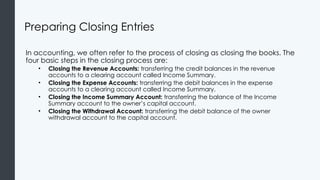

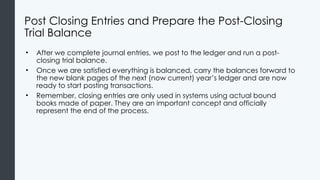

The document outlines the steps of completing the accounting cycle, focusing on the process of adjusting journal entries, creating an adjusted trial balance, preparing financial statements, and closing the books. It details the need for adjusting entries to ensure accuracy in financial reporting and distinguishes between accruals and deferrals. Additionally, it provides a thorough guide on preparing income statements, statements of owner's equity, and balance sheets, as well as the closing process for accounting periods.