Downloaded 147 times

![BMAC5203/JAN2012/F - AA

1

PART A

INSTRUCTIONS: 1. THERE ARE TWO (2) QUESTIONS IN THIS PART.

2. ANSWER BOTH QUESTIONS.

Question 1

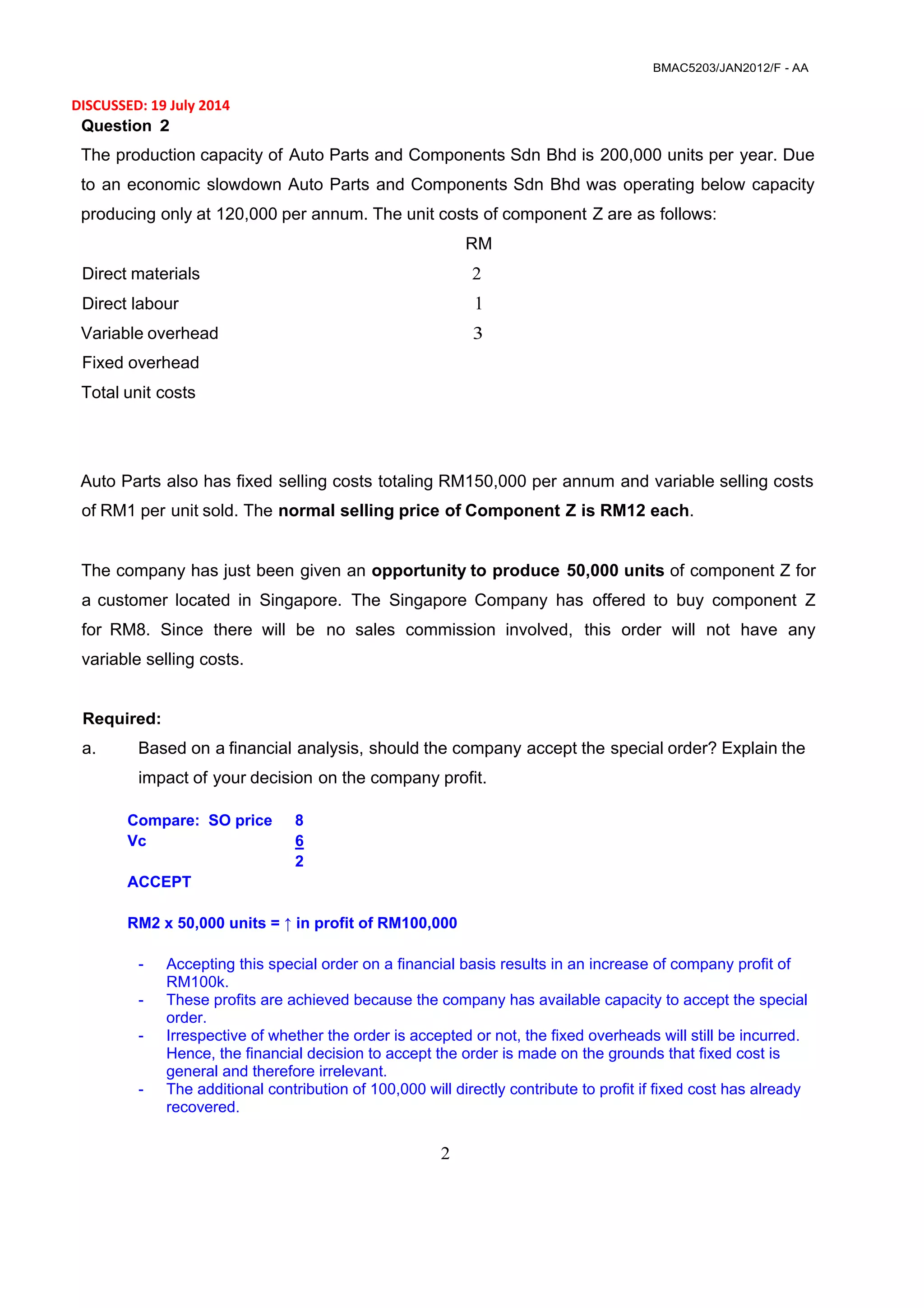

Apex Sdn Bhd designs and manufactures special decorative porcelain vases. A highly

sophisticated machinery was purchased for the production of the vases. The production

department established the following standards for the product's variable input.

Standard costs per unit

RM

Direct materials 18kg at RM5.25 94.50

Direct labour 2hours at RM7.50 15.00

Variable overhead 2hours at RM3.00 6.00

Total unit cost 115.50

During the month, Apex had the following actual results:

Units produced 9,000

Actual labour hours 16200 hours

Actual labour costs RM129,600

Materials purchased and used 161,000 at RM5.50

Variable overheadcosts RM55,500

Required:

a. Compute and explain the material price and usage variances.

b. Compute and explain the labour rate and efficiency variances.

[7 marks]

[7 marks]

c. Compute and explain the variable overhead expenditure and efficiency variances.

[6 marks]

[TOTAL: 20 MARKS]](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-1-2048.jpg)

![BMAC5203/JAN2012/F - AA

3

b. What qualitative factors might impact on the decisions?

[to elaborate more]

1. there’s spare capacity available, therefore doesn’t affect normal sales

2. the acceptance of the special order doesn’t affect the relationship with

your normal customers.

[8

marks]

c. Explain why is knowledge of cost behaviour important for managerial decision making?

[to elaborate more]

Variable cost per unit is constant.

Any cost that is avoidable is important for decision making.

However, variable cost because unavoidable, is irrelevant.

[6 marks]

[TOTAL: 20 MARKS]](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-3-2048.jpg)

![BMAC5203/JAN2012/F - AA

4

PARTB

INSTRUCTIONS: 1. THERE ARE FIVE (5) QUESTIONS IN THIS PART.

2. ANSWER THREE (3} QUESTIONS ONLY.

Question 1

AZ Bank has requested an analysis of checking account profitability by customer type.

Customers are categorized according to geographical location: Inner city, Outer city and

Suburb. The activities associated with the three different customer categories and their

associated annual costs are as follows:

RM

Opening and closing statements 50,000

Issuing monthly statements 75,000

Processing transactions 512,500

Customer inquiries 100,000

Providing ATM services 280,000

Total cost 1,017,500

Additional data concerning the usage of the activities by the various customers are also

provided:

Account Balance

Inner city Outer city Suburb

Number of accounts opened/closed 3,750 750 500

Number of statements issued 112,500 25,000 12,500

Processing transactions 4,500,000 500,000 125,000

Number of telephone minutes 250,000 150,000 100,000

Number of ATM transactions 337,500 50,000 12,500

Number of accounts 9,500 2,000 1,000

Required:

a. Calculate the cost per account by customer category using activity based costing.

[14 marks]

b. AZ Bank offers free checking to all its customers. The interest revenues earned per

account by category are RM95, RM115, and RM180 from the Inner city, Outer city and

Suburb accounts, respectively. Calculate the profit earned per account for each of the

three customer categories.

[6 marks]

[TOTAL: 20 MARKS]](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-4-2048.jpg)

![BMAC5203/JAN2012/F - AA

5

Question 2

Phoenix Sdn Bhd

Projected Income Statement

For the Year Ending 31 December 2012

RM RM

Sales (18,000 units)

Less variable costs:

Variable manufacturing costs

Variable selling costs

Total variable costs

Contribution margin

Less fixed costs:

Fixed manufacturing costs

Fixed selling and administrative costs

Total fixed costs

Operating income

90,000

54,000

127,500

52,500

360,000

144,000

216,000

180,000

36.000

Required:

a. Determine the breakeven point in sales units and dollars and explain your answer.

BEP (units) = RM180,000

RM12

= 15,000 units

BEP (RM) = 15,000 units x RM20*

*360,000 =RM20

18,000

= RM300,000

Phoenix needs to sell 15,000 units in order to break even. This is equivalent to 300,000. any units

sold below 15,000 units will result in loses to the company, while any units sold above 15,000 units

will be profits made by the company.

[6 marks]

b. Explain the term margin of safety and determine Phoenix's margin of safety for the year

2012.

(maybe answered either in units or RM)

Margin of safety is a measure of risk.

MOS = 18,000 units – 15,000 units

= 3,000 units

The marginal safety of phoenix is 3,000 units which is equivalent to 20%.

Any fall in the expected sales will reduce the marginal of safety hence increasing the business risks.

[5 marks]](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-5-2048.jpg)

![BMAC5203/JAN2012/F - AA

6

c. The sales- manager believed the company could increase sales by 2,000 units if

advertising expenditures were increased by RM22,500. By how much will operating

income increase or decrease if the advertising is increased as suggested? Calculate the

revised break-even point.

per unit

sales 20,000.00 20.00 400,000.00

vc per unit 20,000.00 8.00 160,000.00

cost/unit 20,000.00 12.00 240,000.00

fc: current 180,000.00

additional 22,500.00

202,500.00

net income 37,500.00

↑ in income 15,000.00

BEP = RM180,000 + RM22,500

RM12

16,875 units

[4 marks]

d. Assuming the additional advertising expenditure is incurred, what is the target sales that

Phoenix need to achieve a profit of RM57,500? Critically discuss your answer.

Target sales = RM202,500 + RM57,500

RM12

= 21,667 units

Although the target sales is 21667 for a required profit 57500 there is no guaranteed that phoenix can

sell at additional 1675 because there’s no reduction in price offered.

(20k – 16875 = 3125

4800 – 3125 = 1675)

[5 marks]

[TOTAL: 20 MARKS]](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-6-2048.jpg)

![BMAC5203/JAN2012/F - AA

7

Question 3

a. What are the advantages of budgeting?

[4 marks]

b. Miller Corporation has the following sales budget for the first four months of the current

year:

Month

January

February

March

April

Sales

RM

800,000

640,000

880,000

720,000

Historically, the following trend has been established regarding cash collection of sales:

65 percent in month of sale

25 percent in month following sale

8 percent in second month following sale

2 percent uncollectible

The company allows a 2 percent cash discount for payments made by customers during the

month of the sale. November and December sales were RM800,000 and RM480,000,

respectively.

Required:

i) Prepare a schedule of budgeted cash collections from sales for January, February,

and March.

ii) Does a not-for-profit agency need to budget? Why or why not?

[12 marks]

[4 marks]

[TOTAL: 20 MARKS]](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-7-2048.jpg)

![BMAC5203/JAN2012/F - AA

9

Required:

a. Prepare a flexible budget for Hilite Sdn Bhd for the month of December and explain the

weaknesses of the existing report.

[8 marks]

b. Determine the variance between the flexible budget and actual cost for each cost item.

[5 marks]

c. Define static budget and flexible budget. What is each type used for?

[7 marks]

[TOTAL: 20 MARKS]

Question 5 [discussed 19/7/2014]

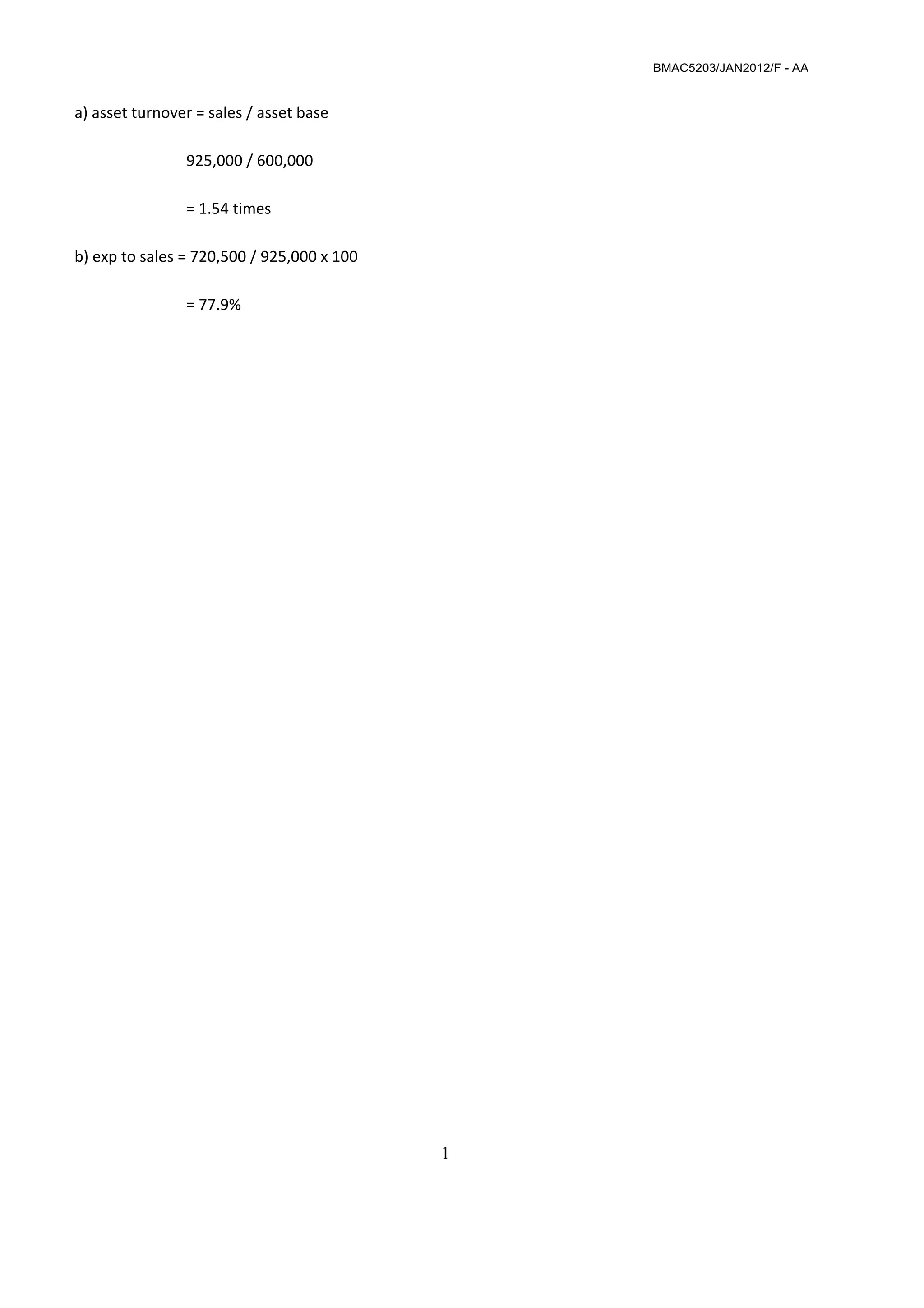

a. The following information is related to the Emas Division:

Asset base [denominator]

Sales Revenues

Expenses [COGS + other expenses]

RM600,000

RM925,000

RM720,500

Required:

i) Calculate the net profit margin, and return on investment (ROI) for Emas Division?

ROI = operating income / cost of investment x 100

ROI = 204,500 / 600,000 x 100

= 34.08%

[4 marks]

ii) Emas has an option to make an additional investment that would add RM100,000 to

the asset base. It would generate an additional RMSO,OOO in sales revenue and no

additional expenses. What would be the effect on net profit margin, and ROI?

Net profit margin = operating income / sales x 100

= 204,500 / 925,000 x 100

= 22.11%

[6 marks]

iii) Another alternative (independent of alternative ii) for Emas is to run an advertising](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-9-2048.jpg)

![BMAC5203/JAN2012/F - AA

1

campaign that would require additional advertising expenses of RM37,500, but the

best estimate is the campaign would generate an additional RM75,000 of revenue.

What would be the effect on net profit margin, and ROI?

Net profit margin = 254,500 / [925,000 + 50,000] x 100

= 26.1%

ROI = 254,500 / [600,000 + 100,000] X 100

= 36.36%

The propotion increased in profit (204 to 254) is greater that

increased in asset based.

ROI = [204,500 + 75,000 – 37,500] / 600,000 X 100

= 40.3%

NP margin = [204,500 + 75,000 – 37,500] / [925,000 + 75,000] x 100

= 24.3%

b. What are the advantages and disadvantages of return on investment (ROI)?

[TOTAL: 20 MARKS]

c. Explain your answer.

- ROI is an accounting measure which can be manipulated by managers.

- Manager’s bonus/reward may be typed to divisional performance using ROI.

Managers can manipulate their performance by deferring the replacement of

fixed assets which have been returned down to their ‘0’ value, hence keeping

the denominator in the formula low. This can artificially inflate the

performance given that revenue and expenses (numerator of the formula) has

not changed significantly from previous years.

- The ROI must be used together with alternative measures when assessing the

performance of division/managers.

d. Calculate the residual income (RI) given 25% cost of capital.

RM

Operating income 204,500

Less: cost of capital

(10% x total assets) (150,000)

Residual income 54,500

So long as RI is positive, the divisional performance is acceptable.

QUESTION PAPER ENDS HERE](https://image.slidesharecdn.com/bmac5203-april2012-140823125404-phpapp01/75/MBA-Accounting-for-Business-Decision-Making-10-2048.jpg)

The document consists of various accounting and finance-related questions, covering topics such as production costs, variance analysis, budgeting, and profitability assessments for different companies. It includes specific scenarios like calculating variances for Apex Sdn Bhd and analyzing special orders for Auto Parts and Components Sdn Bhd, as well as evaluating checking account profitability for AZ Bank. The document also discusses the importance of flexible budgeting and the calculation of return on investment and residual income for Emas Division.