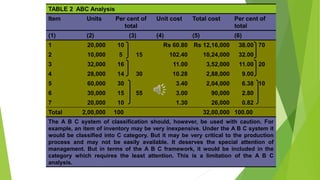

This document discusses ABC analysis, a classification technique that categorizes inventory items into groups A, B, and C based on their cost. Group A items have the largest monetary value but smallest number, accounting for 70% of total inventory cost while being only 15% of items. Group C items have the smallest monetary value but largest number, comprising 55% of items but only 10% of total cost. The document provides an example applying ABC analysis to classify seven inventory items for a firm. It notes that while ABC analysis is useful, it has limitations as some low-cost but critical items may be overlooked.