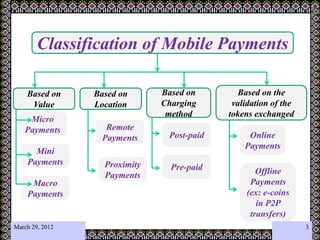

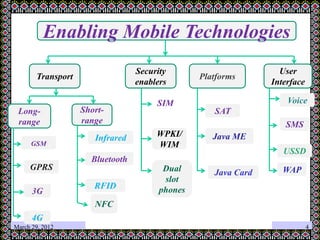

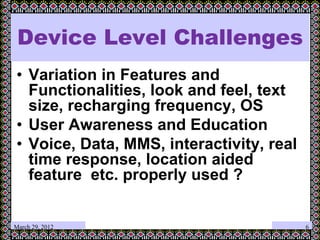

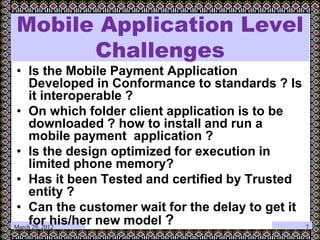

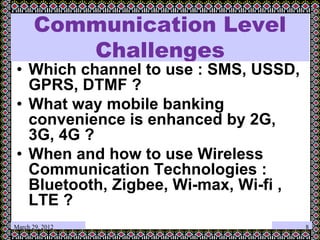

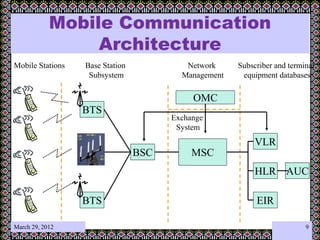

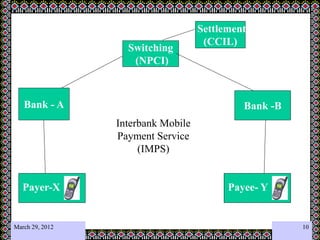

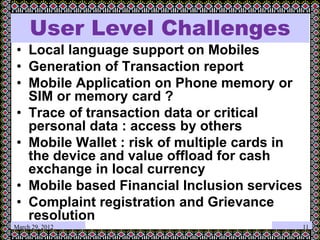

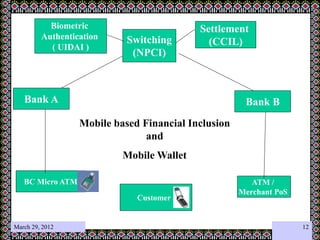

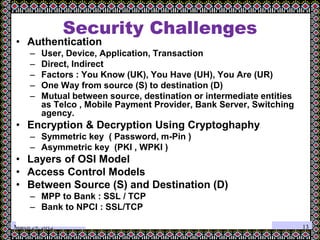

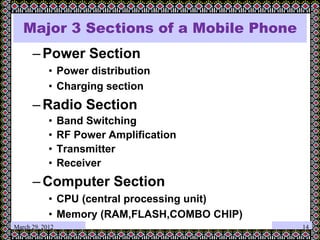

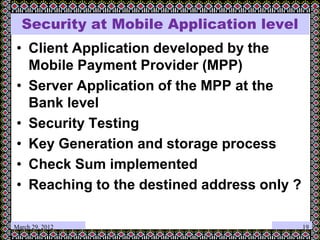

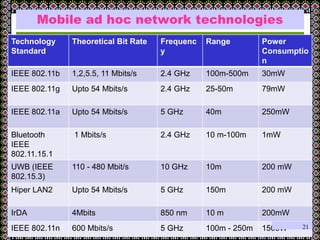

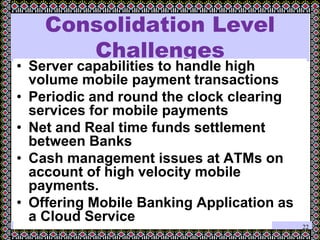

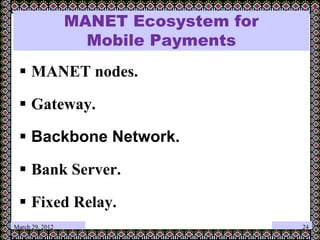

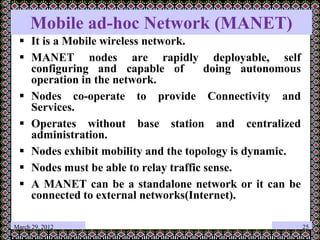

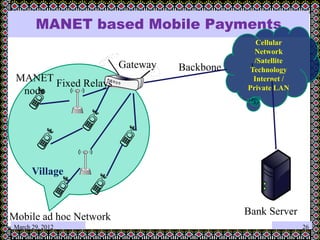

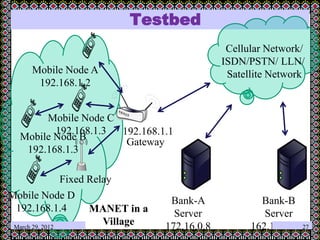

This document discusses technology challenges in mobile payments. It begins by classifying mobile payments based on value, charging method, location, and validation of tokens exchanged. It then discusses enabling mobile technologies like user interfaces, platforms, security, and transport layers. The document outlines several technology challenges including those at the device level, application level, communication level, user level, security level, standards level, and consolidation level. It provides examples of some of these challenges. Finally, it discusses some innovative mobile payment solutions developed in India and provides an overview of a mobile ad-hoc network ecosystem used to enable financial inclusion through mobile payments.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)