Download as PDF, PPTX

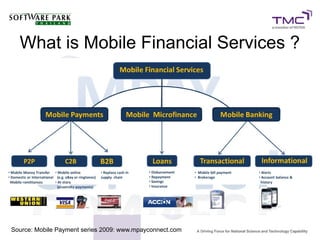

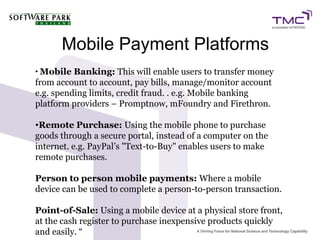

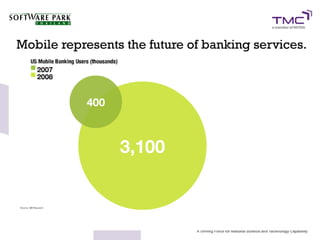

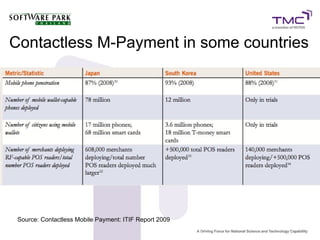

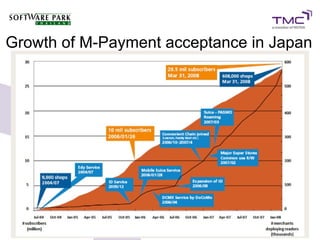

The document discusses mobile financial services, emphasizing the crucial convergence of payment systems and mobile communications, highlighting various technologies such as mobile banking, remote purchases, and NFC. It outlines the current landscape of mobile payment adoption, trends, challenges, and potential future developments. The implications on banking operations, security concerns, and consumer behavior are also addressed, showcasing case studies and regional developments in mobile payment technology.