Download to read offline

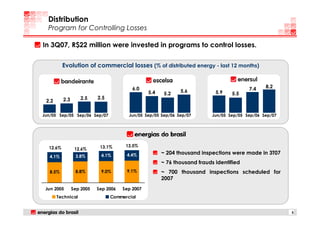

Energias do Brasil reported its third quarter 2007 earnings results in a conference call. The company's CEO, CFO, and investor relations officer presented operating and financial performance for the quarter. Energias do Brasil saw growth in energy distributed and volume sold, while facing challenges from rising costs and expenses. Overall, the company reported higher revenues but lower EBITDA compared to the previous year.