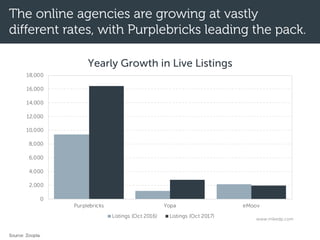

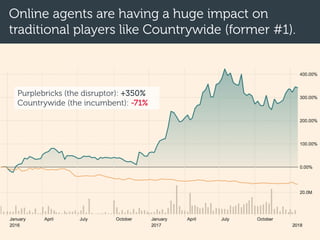

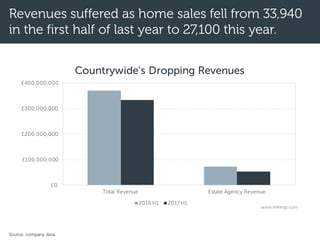

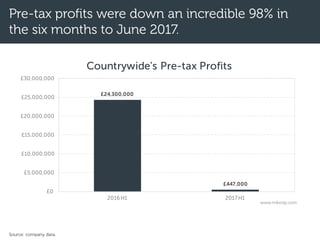

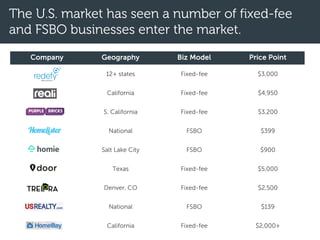

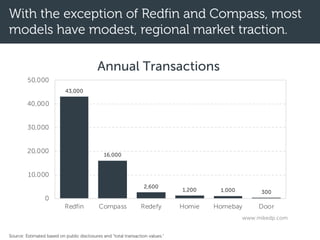

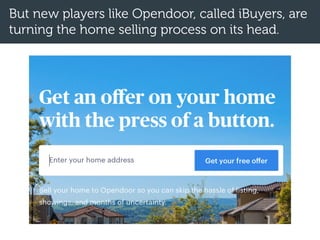

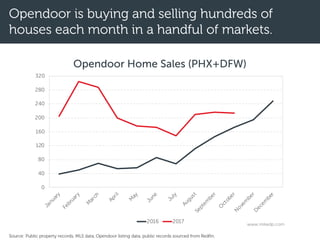

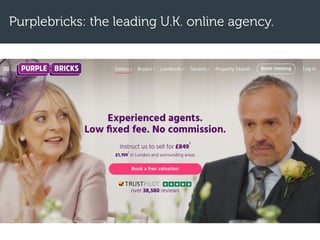

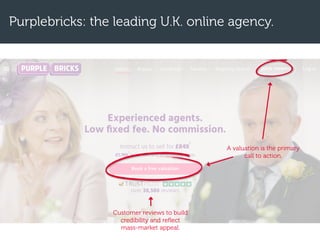

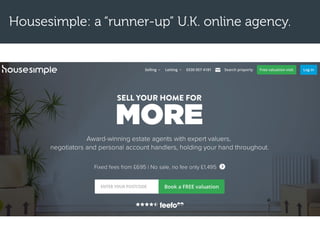

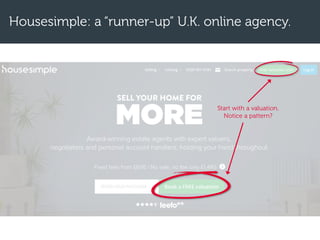

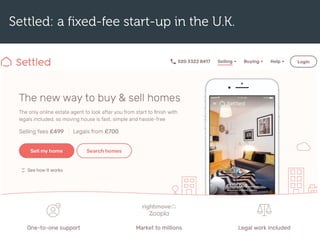

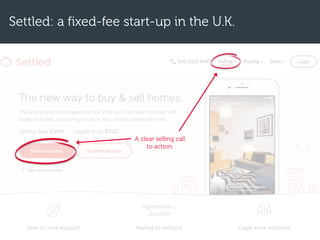

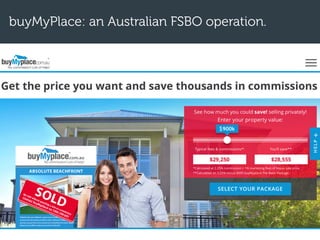

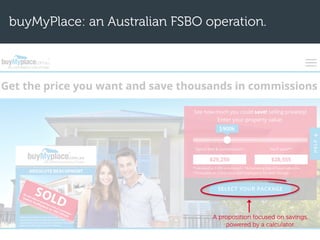

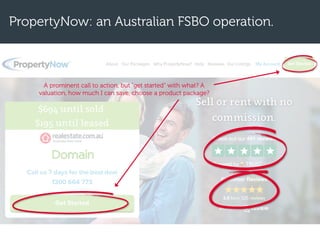

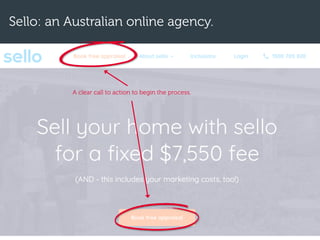

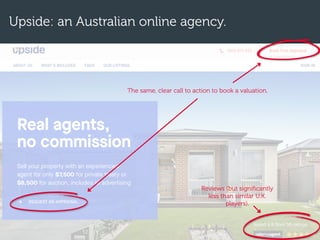

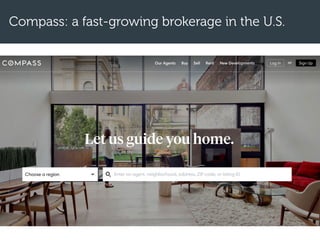

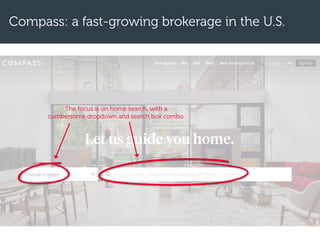

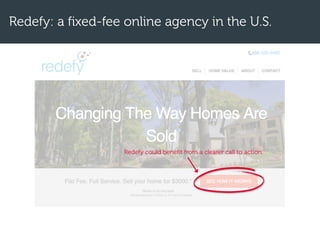

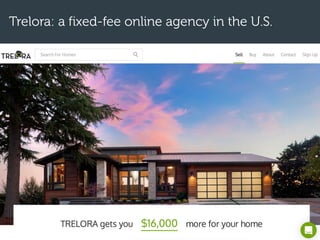

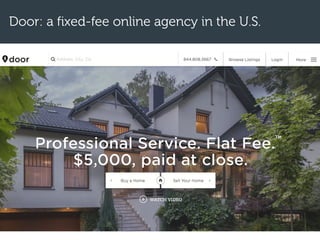

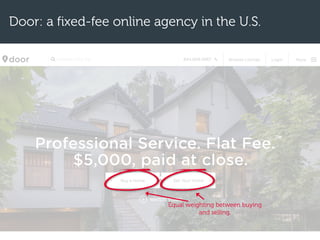

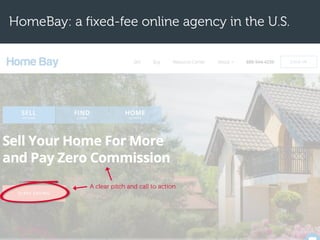

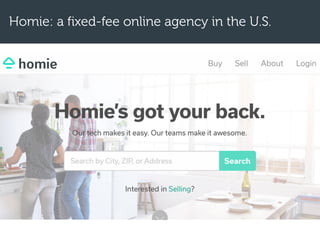

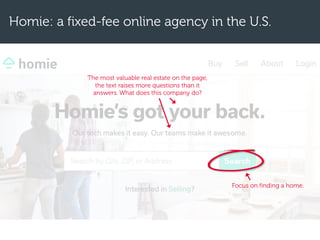

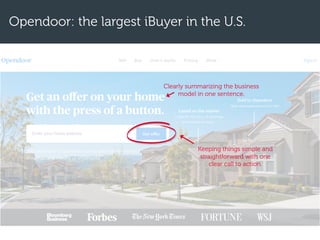

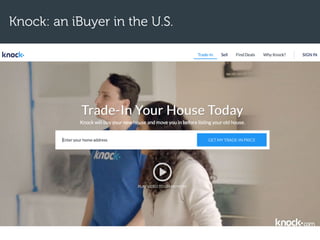

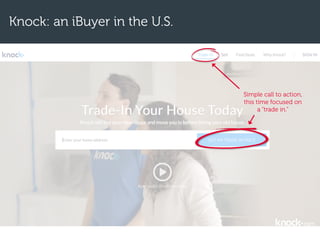

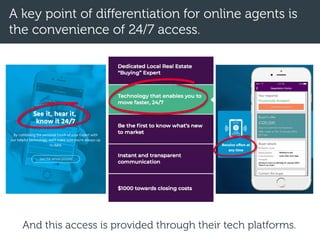

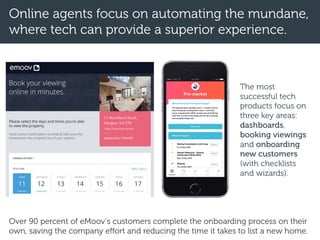

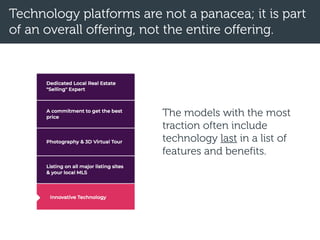

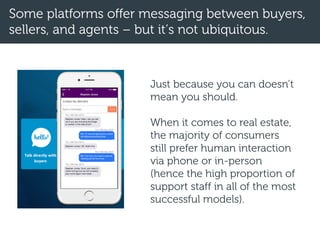

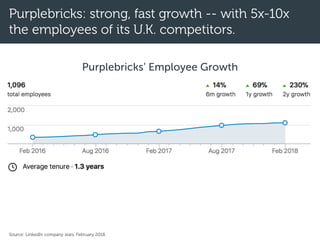

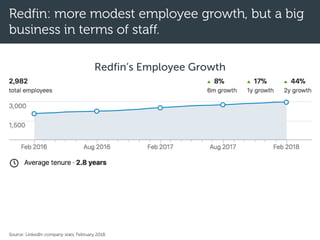

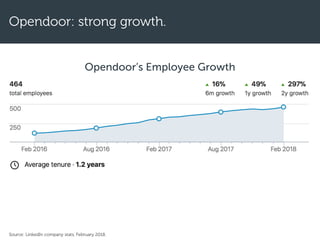

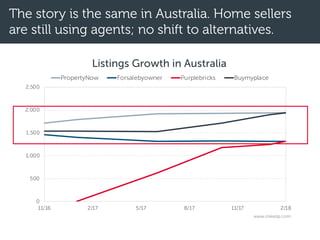

This document provides an overview and analysis of emerging models in the global real estate industry. It covers trends seen in markets like the UK, US, Australia, and Canada. In the UK, online fixed-fee agencies like Purplebricks have gained significant market share, with Purplebricks becoming the largest overall agency. Traditional incumbents like Countrywide have struggled with falling revenues and profits as their business model is disrupted. In the US, there is fragmentation with many new models testing different approaches, though Redfin and Compass have more substantial market share. A new model called iBuyers, led by Opendoor, is also emerging, providing certainty by purchasing homes directly from sellers for a fee. Overall the industry is being innovated through