Download to read offline

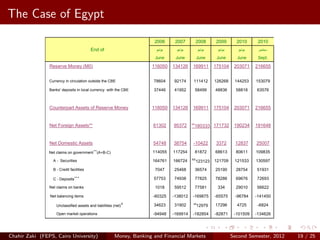

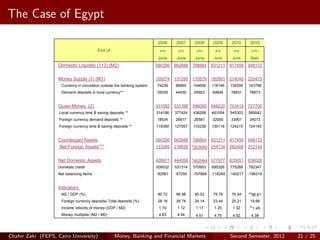

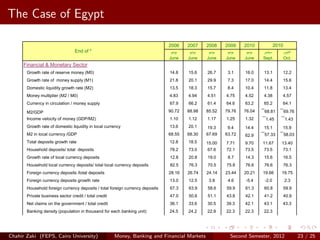

The document discusses monetary aggregates and the Egyptian case. It defines reserve money (M0) as composed of currency and bank deposits with the central bank. Counterpart assets of reserve money include net foreign assets and net domestic assets. For Egypt, data on reserve money and its counterpart assets from 2006-2011 is presented, showing trends in currency, bank deposits, foreign assets, government securities and more.