This document discusses three topics related to personal finance and taxes:

1) Potential tax deductions and credits that can reduce tax liability such as deductions for local taxes, student loans, charitable contributions, and mortgage interest as well as tax credits for energy efficient purchases.

2) The purpose and content of a W-2 form which provides information to complete tax forms including an employee's gross income and tax withholdings.

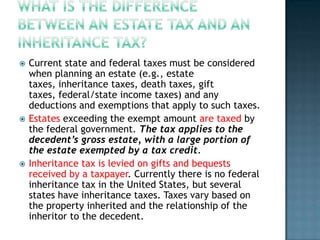

3) Similarities and differences between state and federal taxation of inheritances such as estate taxes, inheritance taxes, exemptions that vary by state, and whether taxes are levied on the estate or gifts received.