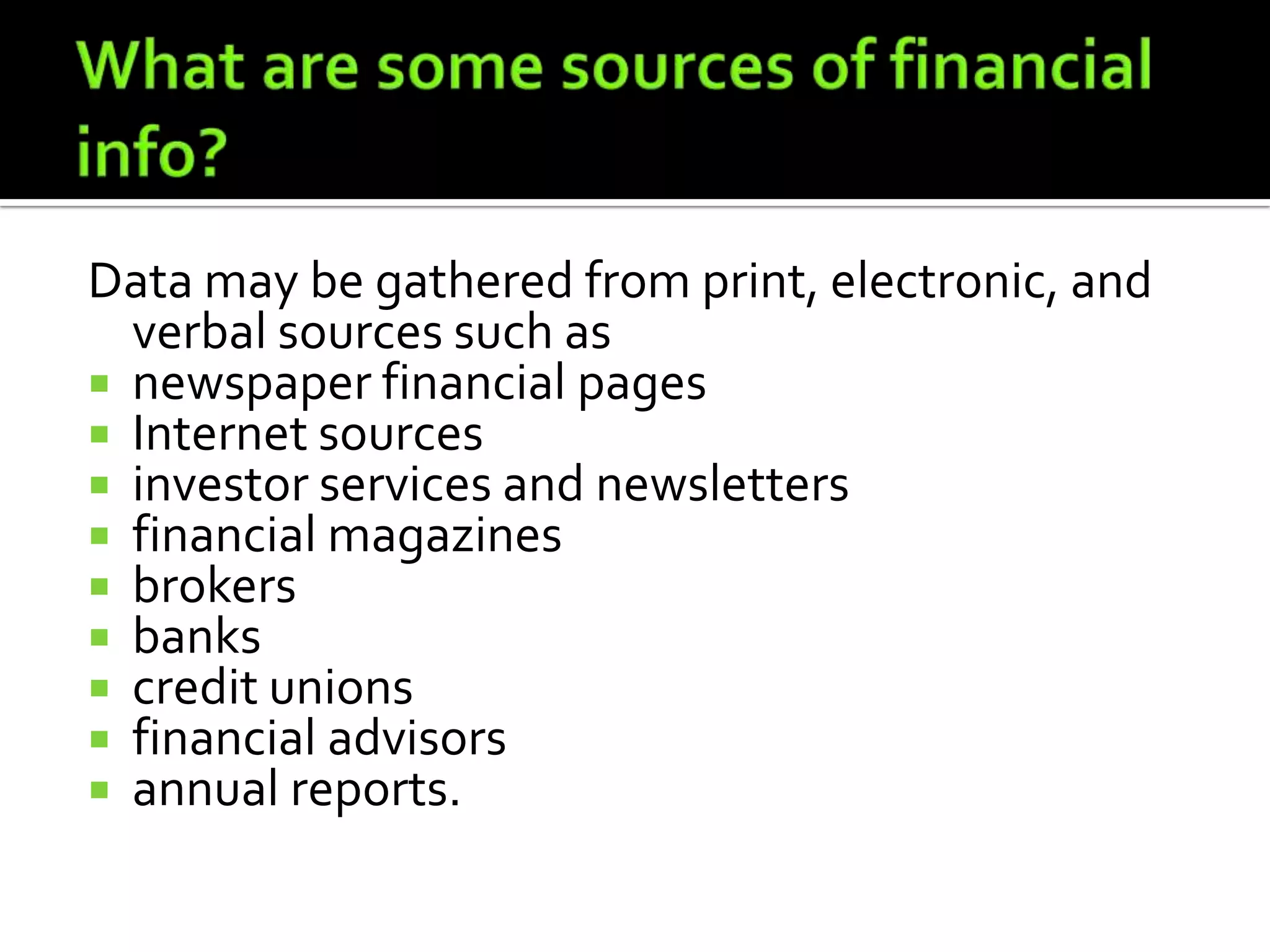

Financial institutions include banks, credit unions, savings and loans, and non-bank institutions that offer services like checking and savings accounts. Over time, institutions have expanded their services and events like the Great Depression and recessions have shaped the banking system. It's important for consumers to access reliable financial information from trustworthy sources when making decisions.