Downloaded 54 times

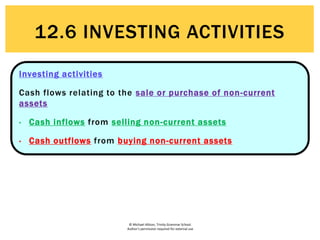

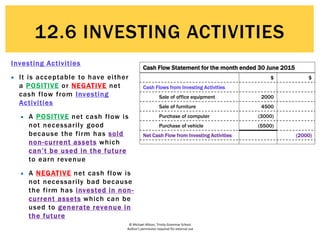

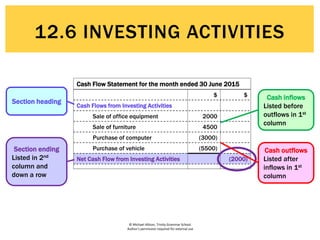

Investing activities relate to cash flows from the sale or purchase of non-current assets. Cash inflows come from selling non-current assets, while cash outflows result from buying non-current assets. A cash flow statement example is provided for the month ended June 30, 2015, which shows a net cash outflow from investing activities of $2,000, with cash inflows of $6,500 from selling equipment and furniture, and cash outflows of $8,500 for purchasing a computer and vehicle.

![Credit Training[Finall]](https://cdn.slidesharecdn.com/ss_thumbnails/credittrainingfinall-091227073414-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)