This document provides an introduction to cash flow statements, including:

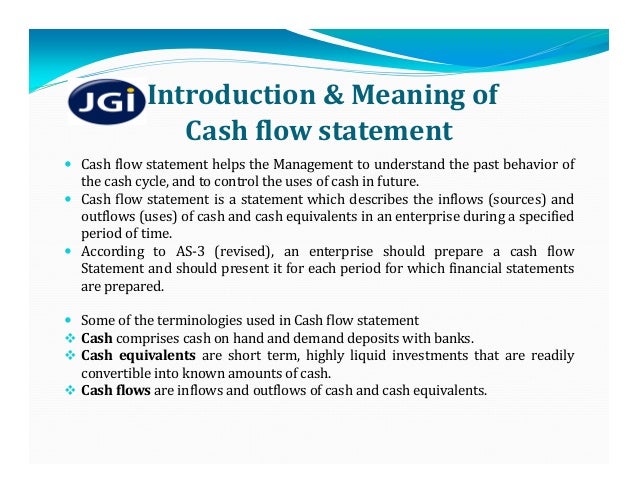

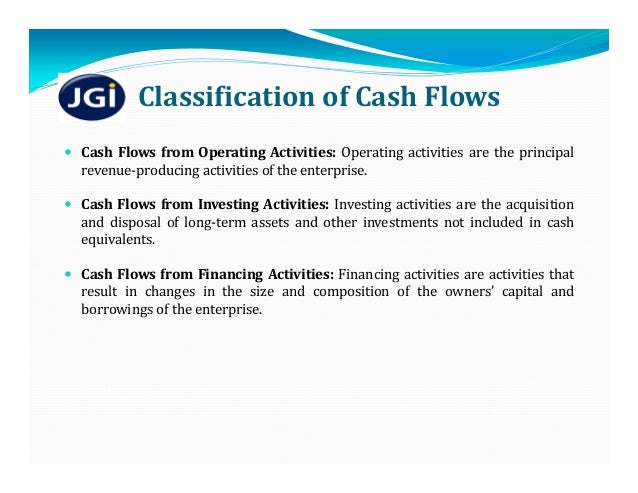

1. It defines a cash flow statement as a statement that describes cash inflows and outflows over a period of time, and explains that cash flow statements classify cash flows into operating, investing and financing activities.

2. It discusses some key terms used in cash flow statements such as cash, cash equivalents, and cash flows.

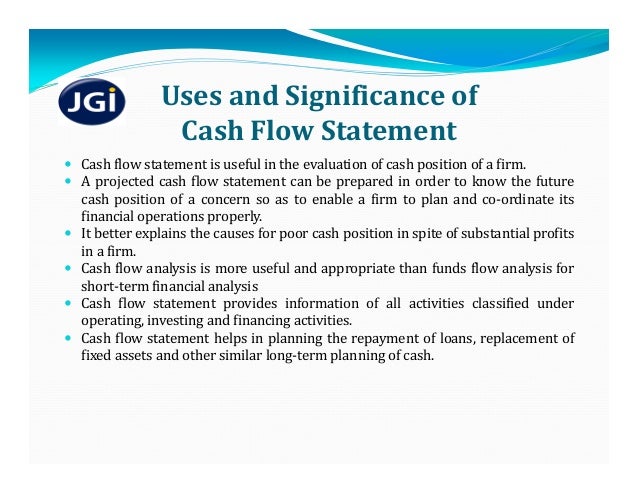

3. It explains the uses and significance of cash flow statements, such as evaluating a firm's cash position, planning future cash needs, and explaining causes of poor cash position despite profits.