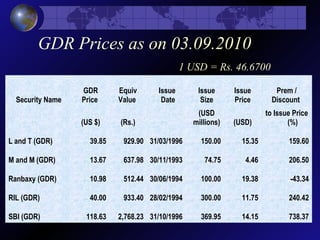

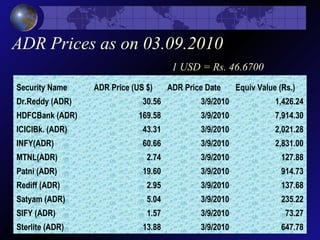

The document discusses various ways that companies can raise equity capital internationally, including listing shares on foreign stock exchanges, issuing depository receipts, and listing Indian Depository Receipts (IDRs) on Indian exchanges. It provides details on major stock exchanges worldwide, cross-listing of shares, American Depository Receipts (ADRs), Global Depository Receipts (GDRs), their uses and benefits, and gives examples of companies that have issued ADRs and GDRs. It also covers the first company to issue IDRs in India.