Downloaded 1,327 times

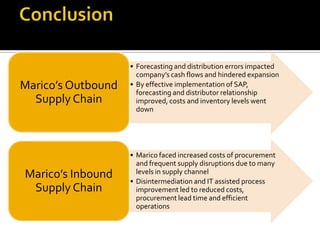

The document details a study of the inbound and outbound supply chains of Marico, an FMCG company based in Mumbai, focusing on its strategy of brand development and expansion into rural markets. It discusses challenges faced, including supply chain inefficiencies, forecasting errors, and distribution issues, which hindered the company's growth and operational effectiveness. Improvements through SAP implementation led to better forecasting, reduced costs, and strengthened distributor relationships, ultimately enhancing the company's supply chain performance.