Cincinnati JLL Office Employment Update February 2015

Cincinnati office insight q2 2015

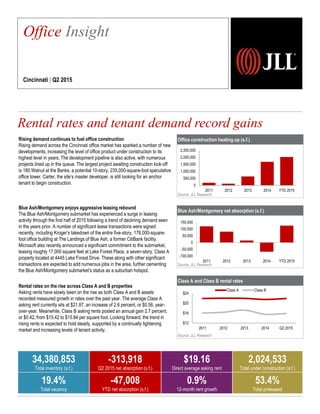

1. Office construction heating up (s.f.)

Source: JLL Research

Blue Ash/Montgomery net absorption (s.f.)

Source: JLL Research

Class A and Class B rental rates

Source: JLL Research

Rising demand continues to fuel office construction

Rising demand across the Cincinnati office market has sparked a number of new

developments, increasing the level of office product under construction to its

highest level in years. The development pipeline is also active, with numerous

projects lined up in the queue. The largest project awaiting construction kick-off

is 180 Walnut at the Banks, a potential 10-story, 235,000-square-foot speculative

office tower. Carter, the site’s master developer, is still looking for an anchor

tenant to begin construction.

Blue Ash/Montgomery enjoys aggressive leasing rebound

The Blue Ash/Montgomery submarket has experienced a surge in leasing

activity through the first half of 2015 following a trend of declining demand seen

in the years prior. A number of significant lease transactions were signed

recently, including Kroger’s takedown of the entire five-story, 176,000-square-

foot office building at The Landings of Blue Ash, a former CitiBank facility.

Microsoft also recently announced a significant commitment to the submarket,

leasing roughly 17,000 square feet at Lake Forest Place, a seven-story, Class A

property located at 4445 Lake Forest Drive. These along with other significant

transactions are expected to add numerous jobs in the area, further cementing

the Blue Ash/Montgomery submarket’s status as a suburban hotspot.

Rental rates on the rise across Class A and B properties

Asking rents have slowly been on the rise as both Class A and B assets

recorded measured growth in rates over the past year. The average Class A

asking rent currently sits at $21.87, an increase of 2.6 percent, or $0.56, year-

over-year. Meanwhile, Class B asking rents posted an annual gain 2.7 percent,

or $0.42, from $15.42 to $15.84 per square foot. Looking forward, the trend in

rising rents is expected to hold steady, supported by a continually tightening

market and increasing levels of tenant activity.

Rental rates and tenant demand record gains

2,257

Office Insight

Cincinnati | Q2 2015

34,380,853

Total inventory (s.f.)

-313,918

Q2 2015 net absorption (s.f.)

$19.16

Direct average asking rent

2,024,533

Total under construction (s.f.)

19.4%

Total vacancy

-47,008

YTD net absorption (s.f.)

0.9%

12-month rent growth

53.4%

Total preleased

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2011 2012 2013 2014 YTD 2015

-100,000

-50,000

0

50,000

100,000

150,000

2011 2012 2013 2014 YTD 2015

$12

$16

$20

$24

2011 2012 2013 2014 Q2 2015

Class A Class B