Recommended

More Related Content

What's hot

What's hot (19)

Similar to JLL Detroit Office Insight - Q2 2015

Similar to JLL Detroit Office Insight - Q2 2015 (20)

More from JLL_Midwest_Great_Lakes_Research

More from JLL_Midwest_Great_Lakes_Research (20)

Recently uploaded

Recently uploaded (20)

JLL Detroit Office Insight - Q2 2015

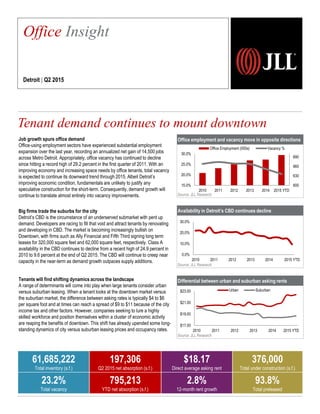

- 1. Office employment and vacancy move in opposite directions Source: JLL Research Availability in Detroit’s CBD continues decline Source: JLL Research Differential between urban and suburban asking rents Source: JLL Research Tenant demand continues to mount downtown 2,257 Office Insight Detroit | Q2 2015 61,685,222 Total inventory (s.f.) 197,306 Q2 2015 net absorption (s.f.) $18.17 Direct average asking rent 376,000 Total under construction (s.f.) 23.2% Total vacancy 795,213 YTD net absorption (s.f.) 2.8% 12-month rent growth 93.8% Total preleased 600 630 660 690 15.0% 20.0% 25.0% 30.0% 2010 2011 2012 2013 2014 2015 YTD Office Employment (000s) Vacancy % 0.0% 10.0% 20.0% 30.0% 2010 2011 2012 2013 2014 2015 YTD $17.00 $19.00 $21.00 $23.00 2010 2011 2012 2013 2014 2015 YTD Urban Suburban Job growth spurs office demand Office-using employment sectors have experienced substantial employment expansion over the last year, recording an annualized net gain of 14,500 jobs across Metro Detroit. Appropriately, office vacancy has continued to decline since hitting a record high of 29.2 percent in the first quarter of 2011. With an improving economy and increasing space needs by office tenants, total vacancy is expected to continue its downward trend through 2015. Albeit Detroit’s improving economic condition, fundamentals are unlikely to justify any speculative construction for the short-term. Consequently, demand growth will continue to translate almost entirely into vacancy improvements. Big firms trade the suburbs for the city Detroit’s CBD is the circumstance of an underserved submarket with pent up demand. Developers are racing to fill that void and attract tenants by renovating and developing in CBD. The market is becoming increasingly bullish on Downtown, with firms such as Ally Financial and Fifth Third signing long term leases for 320,000 square feet and 62,000 square feet, respectively. Class A availability in the CBD continues to decline from a recent high of 24.9 percent in 2010 to 9.6 percent at the end of Q2 2015. The CBD will continue to creep near capacity in the near-term as demand growth outpaces supply additions. Tenants will find shifting dynamics across the landscape A range of determinants will come into play when large tenants consider urban versus suburban leasing. When a tenant looks at the downtown market versus the suburban market, the difference between asking rates is typically $4 to $6 per square foot and at times can reach a spread of $9 to $11 because of the city income tax and other factors. However, companies seeking to lure a highly skilled workforce and position themselves within a cluster of economic activity are reaping the benefits of downtown. This shift has already upended some long- standing dynamics of city versus suburban leasing prices and occupancy rates.

- 2. Current conditions – submarket Historical leasing activity (s.f.) Source: JLL Research Source: JLL Research Total net absorption (s.f.) Source: JLL Research Total vacancy rate (%) Source: JLL Research Direct average asking rent ($ p.s.f.) Source: JLL Research -1,247,120 -1,304,860 -476,545 -1,953,820 -1,767,490 1,277,568 1,510,536 176,382 1,288,053 795,213 -2,500,000 -1,000,000 500,000 2,000,000 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 $21.05 $20.75 $19.73 $19.31 $19.10 $18.56 $18.15 $17.76 $17.99 $18.17 $17.00 $18.50 $20.00 $21.50 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 23.7% 25.9% 26.7% 30.0% 32.9% 30.8% 28.3% 28.0% 25.3% 23.2% 20.0% 25.0% 30.0% 35.0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 Northern I-275, Washtenaw Landlordleverage Tenantleverage Peaking market Falling market Bottoming market Rising market CBD Downriver, Dearborn 5,000,000 5,000,000 5,300,000 5,100,000 2,000,000 0 2,000,000 4,000,000 6,000,000 2011 2012 2013 2014 YTD 2015 Southfield, Macomb Farmington Hills ©2015 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Andrew Batson | andrew.batson@am.jll.com Royal Oak Southern I-275 North Oakland Birmingham New Center