Recommended

More Related Content

Viewers also liked

Similar to JLL Cleveland Office Insight - Q2 2015

Similar to JLL Cleveland Office Insight - Q2 2015 (20)

More from JLL_Midwest_Great_Lakes_Research

More from JLL_Midwest_Great_Lakes_Research (20)

Recently uploaded

Recently uploaded (20)

JLL Cleveland Office Insight - Q2 2015

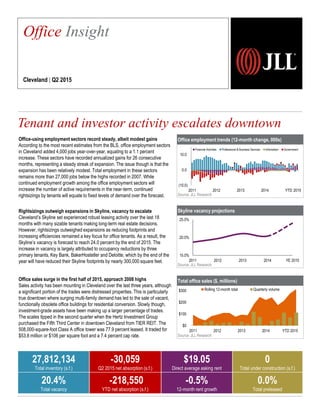

- 1. Office employment trends (12-month change, 000s) Source: JLL Research Skyline vacancy projections Source: JLL Research Total office sales ($, millions) Source: JLL Research Office-using employment sectors record steady, albeit modest gains According to the most recent estimates from the BLS, office employment sectors in Cleveland added 4,000 jobs year-over-year, equating to a 1.1 percent increase. These sectors have recorded annualized gains for 26 consecutive months, representing a steady streak of expansion. The issue though is that the expansion has been relatively modest. Total employment in these sectors remains more than 27,000 jobs below the highs recorded in 2007. While continued employment growth among the office employment sectors will increase the number of active requirements in the near-term, continued rightsizings by tenants will equate to fixed levels of demand over the forecast. Rightsizings outweigh expansions in Skyline, vacancy to escalate Cleveland’s Skyline set experienced robust leasing activity over the last 18 months with many sizable tenants making long-term real estate decisions. However, rightsizings outweighed expansions as reducing footprints and increasing efficiencies remained a key focus for office tenants. As a result, the Skyline’s vacancy is forecast to reach 24.0 percent by the end of 2015. The increase in vacancy is largely attributed to occupancy reductions by three primary tenants, Key Bank, BakerHostetler and Deloitte, which by the end of the year will have reduced their Skyline footprints by nearly 300,000 square feet. Office sales surge in the first half of 2015, approach 2008 highs Sales activity has been mounting in Cleveland over the last three years, although a significant portion of the trades were distressed properties. This is particularly true downtown where surging multi-family demand has led to the sale of vacant, functionally obsolete office buildings for residential conversion. Slowly though, investment-grade assets have been making up a larger percentage of trades. The scales tipped in the second quarter when the Hertz Investment Group purchased the Fifth Third Center in downtown Cleveland from TIER REIT. The 508,000-square-foot Class A office tower was 77.9 percent leased. It traded for $53.8 million or $106 per square foot and a 7.4 percent cap rate. Tenant and investor activity escalates downtown 2,257 Office Insight Cleveland | Q2 2015 27,812,134 Total inventory (s.f.) -30,059 Q2 2015 net absorption (s.f.) $19.05 Direct average asking rent 0 Total under construction (s.f.) 20.4% Total vacancy -218,550 YTD net absorption (s.f.) -0.5% 12-month rent growth 0.0% Total preleased (10.0) 0.0 10.0 2011 2012 2013 2014 YTD 2015 Financial Activities Professional & Business Services Information Government 15.0% 20.0% 25.0% 2011 2012 2013 2014 YE 2015 $0 $100 $200 $300 2011 2012 2013 2014 YTD 2015 Rolling 12-month total Quarterly volume

- 2. Current conditions – submarket Historical leasing activity (s.f.) Source: JLL Research Source: JLL Research Total net absorption (s.f.) Source: JLL Research Total vacancy rate (%) Source: JLL Research Direct average asking rent ($ p.s.f.) Source: JLL Research 542,471 -274,386 458,867 -622,126 -551,674 29,238 226,632 570,893 273,709 -41,538 -800,000 -400,000 0 400,000 800,000 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 $19.77 $19.94 $19.45 $19.74 $19.46 $19.13 $19.05 $18.93 $18.98 $19.05 $18.50 $19.00 $19.50 $20.00 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 16.6% 18.6% 17.1% 19.8% 21.8% 22.3% 21.7% 21.2% 20.3% 20.4% 14.0% 17.0% 20.0% 23.0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 Landlordleverage Tenantleverage Peaking market Falling market Bottoming market Rising market 1,500,000 1,700,000 2,000,000 1,500,000 600,000 0 750,000 1,500,000 2,250,000 2011 2012 2013 2014 YTD 2015 ©2015 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Andrew Batson | andrew.batson@am.jll.com Cleveland CBD Suburbs