Recommended

Recommended

More Related Content

Similar to Week 3 Forecasting Assignment BackgroundThe Flexible-Budget Va.docx

Similar to Week 3 Forecasting Assignment BackgroundThe Flexible-Budget Va.docx (14)

More from cockekeshia

More from cockekeshia (20)

Recently uploaded

Recently uploaded (20)

Week 3 Forecasting Assignment BackgroundThe Flexible-Budget Va.docx

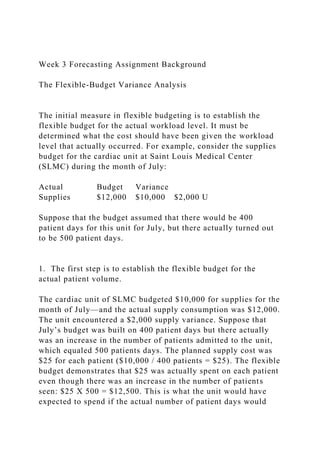

- 1. Week 3 Forecasting Assignment Background The Flexible-Budget Variance Analysis The initial measure in flexible budgeting is to establish the flexible budget for the actual workload level. It must be determined what the cost should have been given the workload level that actually occurred. For example, consider the supplies budget for the cardiac unit at Saint Louis Medical Center (SLMC) during the month of July: Actual Budget Variance Supplies $12,000 $10,000 $2,000 U Suppose that the budget assumed that there would be 400 patient days for this unit for July, but there actually turned out to be 500 patient days. 1. The first step is to establish the flexible budget for the actual patient volume. The cardiac unit of SLMC budgeted $10,000 for supplies for the month of July—and the actual supply consumption was $12,000. The unit encountered a $2,000 supply variance. Suppose that July’s budget was built on 400 patient days but there actually was an increase in the number of patients admitted to the unit, which equaled 500 patients days. The planned supply cost was $25 for each patient ($10,000 / 400 patients = $25). The flexible budget demonstrates that $25 was actually spent on each patient even though there was an increase in the number of patients seen: $25 X 500 = $12,500. This is what the unit would have expected to spend if the actual number of patient days would

- 2. have been known. For the cardiac unit, the total variance = $2,500. However, this volume variance is considered unfavorable because more spending occurred than was expected. Even though the increased number of patients admitted to the cardiac unit may represent more patient revenues, the excess cost is viewed as unfavorable. At this point, the variance in supplies has been explained by the fact that there was a different (higher) volume of patients than had been anticipated. Actual Flexible Original Budget Budget Budget Supplies $12,000 $12,500 $10,000 Flexible Volume Budget Variance Variance $500 $2,000 U Total Variance $2,500 U 2. The next step entails reviewing nursing labor costs to note whether there is a differences in the amount that was budgeted for in the month of July and the amount that actually occurred. Actual Budget Variance Salaries $110,000 $92,000 $18,000 U Flexible Budget $115,000 First, determine the flexible-budget salaries. The nursing salaries should vary in direct proportion to patient days. As more patients are admitted to the unit, more nursing care hours will be delivered to care for these extra patients. For example,

- 3. nursing salaries had been budgeted at $92,000 for the 400 patient days. This was a cost of $230 per patient. Instead, 500 patients were admitted to the unit during the month of March, which should equal $115,000 (500 X $230 = $115,000). Next, determine if there is a variance between the flexible- budget salary and actual budget amount that occurred. When the flexible salary costs are subtracted from the actual salary costs, it turns out that there is a $5,000 favorable variance ($115,000 - $110,000 = $5,000). The actual amount spent was less than the flexible budget. In fact, the manager should have expected to spend $5,000 more on nursing salaries than was in the original budget, given the 100 extra patient days. The cardiac unit actually spent $5,000 less than should have been expected. ` Goal: Acquire email access of an employee Break in/Entry (I) Learn the password (P) IT / Hacking (P) Find written password (I)

- 4. Get password from target (P) Get password from others (Executive Admin or IT) Laptop Present (P) Guess password (I) Infect PC with Malware / Key logger (P) Threaten (I) Eavesdrop (I)

- 5. Blackmail (I) Social Engineering (P) Add malware/ Key logger on PC (P) Password stated (I) Listen to conversation (P) Access email program (P) Attempt to login to device (I) Access files that may have the info (I)

- 6. Open email app and see if the password was saved (I) Look for data files that may contain password info (I) Social Engineering (P) Bribery (P) Threaten (I) Phishing email (P)

- 7. Attempt to reset password using recovery (I) Find written password (P) Laptop not signed in (P) Laptop signed in and accessible (P) and Read Bruce Schneier's paper on attack trees (https://www.schneier.com/paper-attacktrees-ddj-ft.html (Links to an external site.)). Note that he uses some technical jargon to make a point about good vs. bad security controls. Don't worry if this doesn't make sense, the overall article is very good. Come up with your own attack goal, and list some first level attacks that would allow an "evil doer" to achieve the attack

- 8. goal. The attack may involve a computer breach, or it may involve some other type of crime or even a non-criminal action that results in harm. After defining the single goal of the evil attacker, create a second level of different attack methods. One method might involve a computer intrusion, another a physical "break and enter", a third human persuasion (social engineering), etc. For each attack method, the next set of branches under the method may be the different tasks required to succeed at the method. Create a sample tree in a graphical format, as shown in the article. Remember, a tree has multiple levels, branches do not join (they only spread out) and there must be a single attack goal at the root. Indicate "and" cases where a combination of attacks are required to meet the next level's goal. Full credit for this project requires that you meet all these Forecasting Assignment Guidelines With Scoring Rubric Purpose The purposes of this assignment are to (a) identify and articulate key concepts of forecasting and budgeting strategies for your cardiac unit at Saint Louis Medical Center (SLMC), which includes evaluating variance analyses as they apply to nursing budgets within healthcare organizations (CO 2); and (b) formulate a revenue and expense budget for a nursing unit within a healthcare organization (CO 1) and communicate the information in a clear, succinct, and scholarly manner. Course Outcomes Through this assignment, the student will demonstrate the ability to (CO 1) Formulate a revenue and expense budget for a nursing unit within a healthcare organization. (PO 2 and PO 8) (CO 2) Evaluate variance analyses as they apply to nursing budgets within healthcare organizations. (PO 4) Due Date: Sunday 11:59 p.m. MT at the end of Week 3 into the CCN Dropbox

- 9. Total Points Possible: 200Requirements: 1. This paper will be graded on quality of paper information, use of citations, use of standard English grammar, sentence structure, and organization based on the required components. 2. Create this assignment using Microsoft Word, which is the required format for all Chamberlain documents. You can tell that the document is saved as an MS Word document because it will end in.docx. 3. Submit the paper to the appropriate CCN Dropbox by 11:59 p.m. MT on Sunday of the week due. Any questions about this paper may be discussed in the weekly Q & A Discussion topic. 4. The length of the paper is to be no greater than three pages, excluding title page and reference page. Extra pages will not be read by the instructor and will not count toward your grade. 5. APA format (6th edition) is required in this assignment, including a title page and reference page. Use APA level 1 headings for the organizational structure of this assignment. Remember that the introduction does not carry a heading that labels it as a level heading in APA format. The first part of your paper is assumed to be the introduction. See the APA manual for details. See the resource in Doc Sharing called Guidelines for Writing Professional Papers. Use the suggested format and headings to organize your assignment: a. Include an introduction (do not label it as a heading in APA format) b. Key concepts of forecasting budget c. Supporting evidence d. Budget strategies e. ConclusionPreparing the paper Note: Use the resources in Doc Sharing related to SLMC to assist in completion of this assignment; Week 3 Forecasting Background and SLMC information as needed. 1. Clear introduction of your forecasting assignment is in the introduction paragraph, including a sentence that states the purpose of your paper. 2. Clearly articulate key concepts of your forecasting budget for

- 10. the cardiac unit at SLMC. 3. Include of a minimum of three sources of scholarly, empirical evidence that supports your budget strategies for the cardiac unit at SLMC. See resources under Doc Sharing related to SLMC. 4. Identify budget strategies to keep your forecast for the cardiac unit at SLMC within budget. 5. Provide concluding statements that should summarize your overall forecasting assignment content. 6. The paper will be three pages maximum, excluding title and reference page(s). Note: If you go over the paper length, the information will not be graded by the instructor. 7. Title and reference page(s) must be in APA format (6th edition). 8. Use 12-point Times New Roman font and one-inch margins on all sides of the paper. Category Points % Description Introduction 30 15% Introduction clearly introduces your forecasting assignment and purpose of assignment. Forecasting Budget Concepts 45 22.5% Identification of key concepts of your forecasting budget for the cardiac unit at SLMC is clearly articulated. Evidence 30 15% Minimum of three scholarly, empirical evidence sources

- 11. supporting your budget strategies for the cardiac care unit at SLMC. Budget Strategies 40 20% Identify budget strategies to keep your forecast for the cardiac unit at SLMC within budget. Conclusion 30 15% Concluding statements summarizing content are present. Text, title page, and references are consistent with APA format 10 5% Text, title page, and references are consistent with APA format. Ideas and information from other sources are cited correctly 10 5% Ideas and information from other sources are cited correctly. Rules of grammar, word usage, and punctuation are followed 5 2.5% Rules of grammar, word usage, and punctuation are followed. Total 200 100 A quality assignment will meet or exceed all of the above requirements. Chamberlain College of Nursing NR533 Financial Management in Healthcare Organizations 1 Grading Rubric Assignment Criteria

- 12. Exceptional (100%) Outstanding or highest level of performance Exceeds (88%) Very good or high level of performance Meets (80%) Competent or satisfactory level of performance Needs Improvement (38%) Poor or failing level of performance Developing (0) Unsatisfactory level of performance Content Possible Points = 175 Points Introduction clearly introduces your forecasting assignment 30 Points 26 Points 24 Points 11 Points 0 Points Introduction clearly introduces your forecast and purpose of assignment. Introduction introduces your forecast with minor lack of clarity or elements. Introduction of forecast lacks occasional important element or specificity. Introduction of forecast has multiple instances of inaccuracies

- 13. Introduction is not present. Identification of key concepts of forecast budget is clearly articulated. 45 Points 40 Points 36 Points 17 Points 0 Points Identification of key concepts of your forecasting budget for the cardiac unit at SLMC is clearly articulated with no inaccuracy. Identification of key concepts of your forecasting budget for the cardiac unit at SLMC is clearly articulated with rare inaccuracy. Identification of key concepts of your forecasting budget for the cardiac unit at SLMC is clearly articulated but lacks occasional important elements or specificity. Identification of key concepts of your forecasting budget for the cardiac unit at SLMC is clearly articulated but has multiple instances of inaccuracies. Identification of key concepts of your forecasting budget for the cardiac unit at SLMC is not present. At least three empirical, scholarly evidence sources supporting your budget strategies for the cardiac care unit at SLMC included 30 Points 26 Points 24 Points 11 Points 0 Points At least three empirical, scholarly evidence sources supporting your budget strategies for the cardiac care unit at SLMC are

- 14. included. Empirical, scholarly evidence sources supporting your budget strategies for the cardiac care unit at SLMC are included with rare inaccuracy or only two sources are included. Empirical, scholarly evidence sources supporting your budget strategies for the cardiac care unit at SLMC lack an occasional important element or specificity or less than two sources are included. Empirical, scholarly evidence sources supporting your budget strategy for the cardiac care unit at SLMC have multiple instances of inaccuracies. Empirical, scholarly evidence sources supporting your budget strategy are not present. Identify budget strategies to keep your forecast for the cardiac unit at SLMC within budget. 40 Points 35 Points 32 Points 15 Points 0 Points Clearly identifies budget strategies to keep your forecast for the cardiac unit at SLMC within budget. Identifies budget strategies to keep your forecast for the cardiac unit at SLMC within budget, with missing elements. Identifies budget strategies with a moderate impact to keep your forecast for the cardiac unit at SLMC within budget. Identifies budget strategies with limited impact to keep your forecast for the cardiac unit at SLMC within budget. Budget strategies are not identified. Concluding statements summarizing content are present. 30 Points 26 Points 24 Points 11 Points 0 Points

- 15. Concluding statements summarizing content are present and accurate. Concluding statements summarizing content are present with rare inaccuracy or missing elements. Concluding statements summarizing content lack an occasional important element or specificity. Concluding statements summarizing content have multiple instances of inaccuracies. Concluding statements summarizing content are missing. Content Subtotal _____ of 175 points Format Possible Points = 20 points Text, title page, and references are consistent with APA format. 10 Points

- 16. 9 Points 8 Points 4 Points 0 Points Text, title page, and references are consistent with APA format. Text, title page, and references are consistent with APA format with 1-2 exceptions. There are 3-4 APA format errors in the text, title page, and/or reference page(s). There are 5 APA format errors in the text, title page, and/or reference page(s). There are 6 or more APA format errors in the text, title page, and reference page(s). Ideas and information from other sources are cited correctly. 10 Points 9 Points 8 Points 4 Points 0 Points Ideas and information from other sources are cited correctly. Ideas and information from other sources are cited correctly with one exception. Ideas and information from other sources are cited with two errors. Ideas and information from other sources are cited with 3 or more errors. Ideas and information from other sources are not cited. Grammar Possible Points = 5 points

- 17. Rules of grammar, word usage, and punctuation are followed. 5 points 4 points 3 points 2 points 0 points Rules of grammar, word usage, and punctuation are followed. Rules of grammar, word usage, and punctuation are followed with 1-2 exceptions. Rules of grammar, spelling, word usage, and punctuation are consistent with formal written work with 3-4 exceptions. Rules of grammar, spelling, word usage, and punctuation are consistent with formal written work with 5 exceptions. Rules of grammar, spelling, words usage, and punctuation are followed with more than 6 exceptions. Format Subtotal _____ of 25 points Total Points _____ of 200 points NR533 Directions & Rubric.docx 6