Recommended

Recommended

More Related Content

Similar to GivenLOSS Sells a variety of equpiment including the executive off.pdf

Similar to GivenLOSS Sells a variety of equpiment including the executive off.pdf (20)

More from anjanaarts2014

More from anjanaarts2014 (20)

Recently uploaded

Recently uploaded (20)

GivenLOSS Sells a variety of equpiment including the executive off.pdf

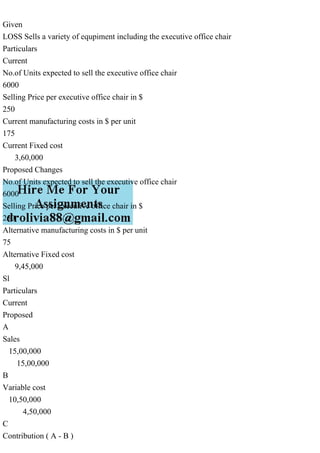

- 1. Given LOSS Sells a variety of equpiment including the executive office chair Particulars Current No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Current manufacturing costs in $ per unit 175 Current Fixed cost 3,60,000 Proposed Changes No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Alternative manufacturing costs in $ per unit 75 Alternative Fixed cost 9,45,000 Sl Particulars Current Proposed A Sales 15,00,000 15,00,000 B Variable cost 10,50,000 4,50,000 C Contribution ( A - B )

- 2. 4,50,000 10,50,000 D Fixed cost 3,60,000 9,45,000 E Profit ( C - D ) 90,000 1,05,000 F price Volume Ratio % ( C/A * 100 ) 30% 70% G Break even Point Volume ( D/F) 12,00,000 13,50,000 H Contribution Per Unit ( C/6000 ) 75 175 I Break even Point Units ( D/H) 4800 5400 J Margin of safety sales ( A -G ) 3,00,000 1,50,000 K Margin of safety in Units ( J / selling Price pu ) 1200 600 L Margin of safety in Percentage ( J / A )*100

- 3. 20% 10% Indiffernce point between two alternatives Indifference cost = point where there is no difference in cost between two alternatives Indifference point Units Assumptions Q = Quantity / units Cpu 1 = Contribution per unit for current alternative Cpu 2= Contribution per unit for proposed alternative FC 1 = fixed cost for current alternative FC 2 = fixed cost for Proposed alternative alternative Indifference point equation Cpu1 * Q - FC1 = Cpu2 * Q - FC2 = 75 * Q - 360,000 = 175 * Q -945,000 = 945,000 - 360,000 = Q ( 175 - 75 ) = 100 * Q = 585,000 = Q = 585,000/100 = Q = 5850 Units Therefore Indifference point is 5850 Units Given LOSS Sells a variety of equpiment including the executive office chair Particulars Current No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Current manufacturing costs in $ per unit 175 Current Fixed cost 3,60,000

- 4. Proposed Changes No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Alternative manufacturing costs in $ per unit 75 Alternative Fixed cost 9,45,000 Sl Particulars Current Proposed A Sales 15,00,000 15,00,000 B Variable cost 10,50,000 4,50,000 C Contribution ( A - B ) 4,50,000 10,50,000 D Fixed cost 3,60,000 9,45,000 E Profit ( C - D ) 90,000 1,05,000 F price Volume Ratio % ( C/A * 100 ) 30%

- 5. 70% G Break even Point Volume ( D/F) 12,00,000 13,50,000 H Contribution Per Unit ( C/6000 ) 75 175 I Break even Point Units ( D/H) 4800 5400 J Margin of safety sales ( A -G ) 3,00,000 1,50,000 K Margin of safety in Units ( J / selling Price pu ) 1200 600 L Margin of safety in Percentage ( J / A )*100 20% 10% Indiffernce point between two alternatives Indifference cost = point where there is no difference in cost between two alternatives Indifference point Units Assumptions Q = Quantity / units Cpu 1 = Contribution per unit for current alternative Cpu 2= Contribution per unit for proposed alternative FC 1 = fixed cost for current alternative FC 2 = fixed cost for Proposed alternative alternative Indifference point equation Cpu1 * Q - FC1 = Cpu2 * Q - FC2

- 6. = 75 * Q - 360,000 = 175 * Q -945,000 = 945,000 - 360,000 = Q ( 175 - 75 ) = 100 * Q = 585,000 = Q = 585,000/100 = Q = 5850 Units Therefore Indifference point is 5850 Units Solution Given LOSS Sells a variety of equpiment including the executive office chair Particulars Current No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Current manufacturing costs in $ per unit 175 Current Fixed cost 3,60,000 Proposed Changes No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Alternative manufacturing costs in $ per unit 75 Alternative Fixed cost 9,45,000 Sl

- 7. Particulars Current Proposed A Sales 15,00,000 15,00,000 B Variable cost 10,50,000 4,50,000 C Contribution ( A - B ) 4,50,000 10,50,000 D Fixed cost 3,60,000 9,45,000 E Profit ( C - D ) 90,000 1,05,000 F price Volume Ratio % ( C/A * 100 ) 30% 70% G Break even Point Volume ( D/F) 12,00,000 13,50,000 H Contribution Per Unit ( C/6000 ) 75 175 I

- 8. Break even Point Units ( D/H) 4800 5400 J Margin of safety sales ( A -G ) 3,00,000 1,50,000 K Margin of safety in Units ( J / selling Price pu ) 1200 600 L Margin of safety in Percentage ( J / A )*100 20% 10% Indiffernce point between two alternatives Indifference cost = point where there is no difference in cost between two alternatives Indifference point Units Assumptions Q = Quantity / units Cpu 1 = Contribution per unit for current alternative Cpu 2= Contribution per unit for proposed alternative FC 1 = fixed cost for current alternative FC 2 = fixed cost for Proposed alternative alternative Indifference point equation Cpu1 * Q - FC1 = Cpu2 * Q - FC2 = 75 * Q - 360,000 = 175 * Q -945,000 = 945,000 - 360,000 = Q ( 175 - 75 ) = 100 * Q = 585,000 = Q = 585,000/100 = Q = 5850 Units

- 9. Therefore Indifference point is 5850 Units Given LOSS Sells a variety of equpiment including the executive office chair Particulars Current No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Current manufacturing costs in $ per unit 175 Current Fixed cost 3,60,000 Proposed Changes No.of Units expected to sell the executive office chair 6000 Selling Price per executive office chair in $ 250 Alternative manufacturing costs in $ per unit 75 Alternative Fixed cost 9,45,000 Sl Particulars Current Proposed A Sales 15,00,000 15,00,000 B Variable cost 10,50,000 4,50,000 C Contribution ( A - B )

- 10. 4,50,000 10,50,000 D Fixed cost 3,60,000 9,45,000 E Profit ( C - D ) 90,000 1,05,000 F price Volume Ratio % ( C/A * 100 ) 30% 70% G Break even Point Volume ( D/F) 12,00,000 13,50,000 H Contribution Per Unit ( C/6000 ) 75 175 I Break even Point Units ( D/H) 4800 5400 J Margin of safety sales ( A -G ) 3,00,000 1,50,000 K Margin of safety in Units ( J / selling Price pu ) 1200 600 L Margin of safety in Percentage ( J / A )*100

- 11. 20% 10% Indiffernce point between two alternatives Indifference cost = point where there is no difference in cost between two alternatives Indifference point Units Assumptions Q = Quantity / units Cpu 1 = Contribution per unit for current alternative Cpu 2= Contribution per unit for proposed alternative FC 1 = fixed cost for current alternative FC 2 = fixed cost for Proposed alternative alternative Indifference point equation Cpu1 * Q - FC1 = Cpu2 * Q - FC2 = 75 * Q - 360,000 = 175 * Q -945,000 = 945,000 - 360,000 = Q ( 175 - 75 ) = 100 * Q = 585,000 = Q = 585,000/100 = Q = 5850 Units Therefore Indifference point is 5850 Units