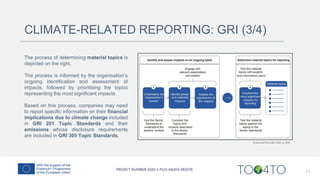

The document discusses climate-related reporting and futures studies, emphasizing their importance in addressing climate change and promoting sustainability. It outlines key instruments such as the Global Reporting Initiative (GRI), Carbon Disclosure Project (CDP), and Task Force on Climate-related Financial Disclosures (TCFD) used for reporting climate risks and opportunities. Additionally, it introduces various futures studies techniques that organizations can utilize to navigate uncertainties and develop strategic plans for a sustainable future.

![REFERENCES

CDP (2022) Scoring Introduction 2022. Available at: https://cdn.cdp.net/cdp-production/cms/guidance_docs/pdfs/000/000/233/original/Scoring-

Introduction.pdf?

Faldi, G. and Macchi, S. (2017) ‘Knowledge for transformational adaptation planning: Comparing the potential of forecasting and backcasting methods for

assessing people’s vulnerability’, in Tiepolo, M., Alessandro, P., and Vieri, T. (eds) Green Energy and Technology, pp. 265–283. doi: 10.1007/978-3-319-

59096-7_13

GRI (2022) Consolidated Set of the GRI Standards. Available at: https://www.globalreporting.org/

Herbohn, K. F., Clarkson, P. M. and Wallis, M. (2022) ‘The state of climate change-related risk disclosures and the way forward’, in Adams, C. A. (ed.)

Handbook of Accounting and Sustainability. Edward Elgar Publishing Ltd., pp. 343–364. doi: https://doi.org/10.4337/9781800373518.00029.

Inayatullah in Metafuture (2016) What Works in Futures Studies (Part 1) [Video]. YouTube. https://www.youtube.com/watch?v=WTuIttajBOc

Inayatullah, S. (2008) ‘Six pillars: Futures thinking for transforming’, Foresight, 10(1), pp. 4–21. doi: 10.1108/14636680810855991. Available at:

https://www.foresightfordevelopment.org/sobipro/54/760-six-pillars-futures-thinking-for-transforming

Inayatullah, S. (2012) There’s a Future: Vision for a Better World, There’s A Future Vision For A Better World. BBVA. Available at:

https://www.bbvaopenmind.com/wp-content/uploads/2013/01/BBVA-OpenMind-Book-There-is-a-Future_Visions-for-a-Better-World-1.pdf

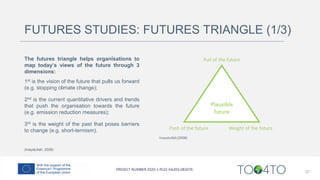

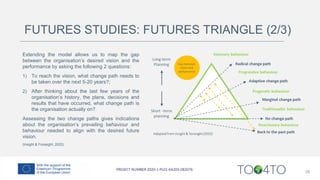

Insight & Foresight (2022) The Futures Triangle. Available at: https://www.insightandforesight.com.au/blog-foresights/futures-triangle

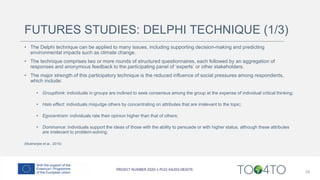

Mukherjee, N. et al. (2015) ‘The Delphi technique in ecology and biological conservation: Applications and guidelines’, Methods in Ecology and Evolution,

6(9), pp. 1097–1109. doi: 10.1111/2041-210X.12387

Neuvonen, A. et al. (2016) No Title. Helsinki. Available at: https://demoshelsinki.fi/julkaisut/nordic-cities-beyond-digital-disruption/ .

TCFD (2021) Task Force on Climate-related Financial Disclosures Implementing the Recommendations of the Task Force on Climate-related Financial

Disclosures. Available at: https://assets.bbhub.io/company/sites/60/2021/07/2021-TCFD-Implementing_Guidance.pdf

36](https://image.slidesharecdn.com/too4tomodule3part3-230725122218-72626ff2/85/TOO4TO-Module-3-Climate-Change-and-Sustainability-Part-3-36-320.jpg)