Downloaded 45 times

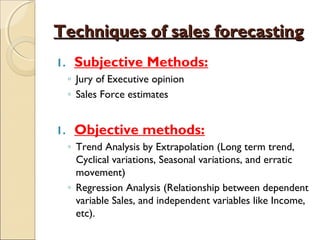

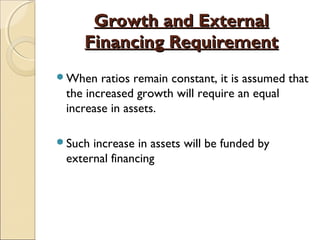

This document provides an overview of financial forecasting. Financial forecasting involves making projections about a company's future financial performance based on assumptions about economic conditions, sales forecasts, and planned financing. Key techniques for financial forecasting include creating pro forma financial statements like income statements and balance sheets, as well as cash budgets and operating budgets. Pro forma statements are created using the percentage of sales method or budgeted expense method to project line items. Forecasting sales involves techniques like trend analysis, regression analysis, and executive opinion. Financial projections are used to assess future performance, examine operational changes, anticipate financing needs, and estimate cash flows.

![Promacs ppt Tamplate 2022[53] - Read-Only.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/promacsppttamplate202253-read-only-221218182756-a524ca6f-thumbnail.jpg?width=640&height=640&fit=bounds)