JSW Steel: Strong operating performance; Upgrade to Buy - Motilal Oswal

•

1 like•313 views

Recommended

Recommended

More Related Content

What's hot

What's hot (9)

Similar to JSW Steel: Strong operating performance; Upgrade to Buy - Motilal Oswal

Similar to JSW Steel: Strong operating performance; Upgrade to Buy - Motilal Oswal (20)

More from IndiaNotes.com

More from IndiaNotes.com (20)

Recently uploaded

Recently uploaded (20)

JSW Steel: Strong operating performance; Upgrade to Buy - Motilal Oswal

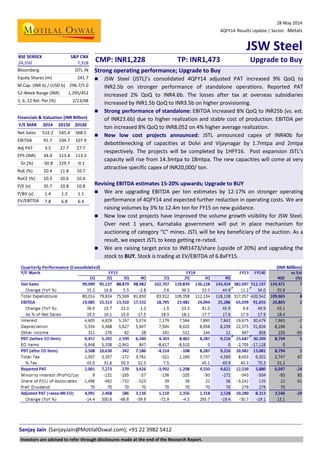

- 1. 28 May 2014 4QFY14 Results Update | Sector: Metals JSW Steel Sanjay Jain (SanjayJain@MotilalOswal.com); +91 22 3982 5412 BSE SENSEX S&P CNX CMP: INR1,228 TP: INR1,473 Upgrade to Buy24,550 7,318 Bloomberg JSTL IN Equity Shares (m) 241.7 M.Cap. (INR b) / (USD b) 296.7/5.0 52-Week Range (INR) 1,295/452 1, 6, 12 Rel. Per (%) 2/13/48 Financials & Valuation (INR Billion) Y/E MAR 2014 2015E 2016E Net Sales 512.2 545.4 568.5 EBITDA 91.7 104.7 107.9 Adj PAT 3.5 27.7 27.7 EPS (INR) 34.4 113.4 113.3 Gr.(%) -30.8 229.7 -0.1 RoE (%) 10.4 11.8 10.7 RoCE (%) 10.3 10.6 10.4 P/E (x) 35.7 10.8 10.8 P/BV (x) 1.4 1.2 1.1 EV/EBITDA ( ) 7.8 6.8 6.4 Strong operating performance; Upgrade to Buy JSW Steel (JSTL)’s consolidated 4QFY14 adjusted PAT increased 9% QoQ to INR2.5b on stronger performance of standalone operations. Reported PAT increased 2% QoQ to INR4.6b. The losses after tax at overseas subsidiaries increased by INR1.5b QoQ to INR3.5b on higher provisioning. Strong performance of standalone: EBITDA increased 8% QoQ to INR25b (vs. est. of INR23.6b) due to higher realization and stable cost of production. EBITDA per ton increased 8% QoQ to INR8,052 on 4% higher average realization. New low cost projects announced: JSTL announced capex of INR40b for debottlenecking of capacities at Dolvi and Vijaynagar by 1.7mtpa and 2mtpa respectively. The projects will be completed by 1HFY16. Post expansion JSTL’s capacity will rise from 14.3mtpa to 18mtpa. The new capacities will come at very attractive specific capex of INR20,000/ ton. Revising EBITDA estimates 15-20% upwards; Upgrade to BUY We are upgrading EBITDA per ton estimates by 12-17% on stronger operating performance of 4QFY14 and expected further reduction in operating costs. We are raising volumes by 3% to 12.4m ton for FY15 on new guidance. New low cost projects have improved the volume growth visibility for JSW Steel. Over next 1 years, Karnataka government will put in place mechanism for auctioning of category “C” mines. JSTL will be key beneficiary of the auction. As a result, we expect JSTL to keep getting re-rated. We are raising target price to INR1473/share (upside of 20%) and upgrading the stock to BUY. Stock is trading at EV/EBITDA of 6.8xFY15. Investors are advised to refer through disclosures made at the end of the Research Report.

- 2. 28 May 2014 2 JSW Steel Consolidated: Stronger S/A performance offset higher overseas losses Consolidated adjusted PAT increased 9% QoQ to INR2.5b on stronger performance of standalone operations. Reported PAT increased 2% QoQ to INR4.6b. The losses after tax at overseas subsidiaries increased by INR1.5b QoQ to INR3.5b on higher provisioning. All subsidiaries together contributed INR323m to EBITDA (- 70% QoQ. JSW coated reported improved operating performance. Tax rate was higher at 49.9% due to consolidation of loss making subsidiaries. Consolidated net debt (including acceptances) was flat during 2HFY14 at INR422b. Acceptances declined by USD473m to USD1.4b during same period. Standalone: Strong results on margin expansion Net sales increased 4% QoQ to INR125b driven by higher steel realization. Net sales realization increased 4% QoQ to INR40,288/t due to price hikes. Share of exports in revenue declined 600bps to 20%. Sale volumes were flat QoQ at 3.1m tons, while crude steel production declined 1% QoQ to 3.1mt. Export sales tonnage was ~876kt (down 13% QoQ). Inventories came down by 100kt during the quarter. Flat steel sales volume decreased 3% QoQ to 2.47m ton, while long steel sales volume increased 16% QoQ to 0.5m ton. EBITDA increased 8% QoQ to INR25b (vs. est. of INR23.6b) due to higher realization and stable cost of production. EBITDA per ton increased 8% QoQ to INR8,052. Average raw material cost was stable despite increase in iron ore prices. Iron ore cost increased by INR490/t QoQ to INR3,820/t. Adjusted standalone PAT increased 24% QoQ to INR8b. E: MOSL Estimates; Note: JSW Ispat is excluded until 4QFY13 Long product sales increased 16% QoQ

- 3. 28 May 2014 3 JSW Steel Subsidiaries: performance remains a drag JSW coated (100% subs.) sold 0.44m tons of value added products and reported EBITDA of INR940m (up 19% QoQ). EBITDA per ton increased 14% QoQ to INR2136/ton. EBITDA contribution from other subsidiaries was loss of INR617m against gain of INR272m in 3QFY14. Chile iron ore operations reported USD1.3m EBITDA (USD5.2m in 3QFY14) on sale of 149kt iron ore. CoP was USD103/t. US plate and pipe mill utilization remains low yet improved 5 percentage points to 44%, while EBITDA loss was USD4m. Quarterly Performance (Subsidiaries) Y/E March FY13 FY14 FY13 FY14E 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Net Sales 8,723 6,428 5,955 6,073 9,125 14,982 16,583 18,530 27,179 59,220 EBITDA 1,357 61 175 359 1,303 1,141 1,062 323 1,951 3,829 JSW coated 790 780 790 940 US Mills 351 160 -41 25 34 -127 -107 -248 Chile iron ore 460 -4 44 359 48 332 324 82 US coal -20 -21 55 -450 PAT -2,821 -2,508 -2,352 -2,413 -2,476 -4,266 -4,125 -5,435 -10,094 -16,303 Source: Company, MOSL Announced new phase of capacity expansion at low specific capex During 4QFY14, JSW Steel has commissioned number of projects i.e. 2.3mtpa CRM phase-2, 4mtpa Pellet plant and 1mtpa coke oven at Dolvi, and new 6 Hi CRM at Kalmeshwar. 1.5mtpa Steel melt shop-3 has been commissioned in the month of April, 2014. Bar rod mill -2 will be commissioned during 1HFY15. JSTL announced capex of INR40b for debottlenecking of capacities at Dolvi and Vijaynagar by 1.7mtpa and 2mtpa respectively. The projects will be completed by 1HFY16. Post expansion JSW Steel’s capacity will rise from 14.3mtpa to 18mtpa. The new capacities will come at very attractive specific capex of INR20,000/ ton. Another INR40b will be spent on sustenance (INR15b), Jharkhand mines (INR7.5b), US coal mines (USD125m), Chile iron ore beneficiation plant (USD60m). Including left over INR40b capex towards outstanding CRM-II projects, a total of INR120b will be spent over FY15-16 on various projects. JSTL has revised upwards FY15 CapEx to INR75b (from INR55b) to undertake new projects.

- 4. 28 May 2014 4 JSW Steel Raising EBITDA by 15-20%. Upgrade to BUY Despite challenges in iron ore sourcing and lackluster domestic steel demand, JSTL operating performance continues to surprise us positively. The operating performance of Dolvi unit is now nearly matching the performance of Vijaynagar. EBITDA per ton of standalone business has expanded to robust INR8000/t. The margins are likely to expand further on benefit of higher share of value added products, step up in long product production, and cost benefits on account of lower coking coal prices, and operating efficiencies from new pellet and coke ovens at Dolvi. We are upgrading estimates by 12% and 17% to INR8052/t and INR7960/t for FY15 and FY16 respectively. We are also upgrading the volume estimates by 3% to 12.4m tons and 12.9m tons for FY15 and FY16. As a result, standalone EBITDA is upgraded by 16% and 21% to INR99.6b and INR102.7b respectively. Consolidated EBITDA is raised by 15% and 20% respectively. Although capex guidance has been raised from INR55b to INR75b, the net debt will start declining in FY15 and FY16 on improved operating cash flows. We believe that Indian steel demand growth has hit the bottom with mere 0.6% growth in FY14. We expect steel demand growth to accelerate to 4% and 6% in FY15 and FY16. New low cost projects have improved the volume growth visibility for JSW Steel. Over next 1 years, Karnataka government will put in place mechanism for auctioning of category “C” mines. JSTL will be key beneficiary of the auction. As a result, we expect JSTL to keep getting re-rated. We are raising target price to INR1473/share (upside of 20%) and upgrading the stock to BUY. Stock is trading at EV/EBITDA of 6.8xFY15. JSW STEEL: Target price calculations Year 2012 2013 2014 2015E 2016E A. S/A volumes 7.8 8.9 11.9 12.4 12.9 B. EBITDA per ton 7,197 7,105 7,405 8,040 7,960 C. S/A EBITDA (AxB) 56,238 63,088 87,826 99,692 102,681 D. Sub. EBITDA 4,781 1,951 3,829 5,058 5,219 E. Cons. EBITDA (C+D) 61,019 65,039 91,655 104,750 107,900 F. Target EV/EBITDA (x) 6.5 6.5 G. Target EV (FxG) 680,873 701,348 less: Net Debt (Rs m) 261,397 292,123 421,688 410,744 394,241 add: CWIP 35,703 65,972 90,972 85,972 70,972 Equity value 356,101 378,079 No. of shares 242 242 Target price 1473 1564 EBITDA per ton estimates raised by 12-17% Volumes estimate raised by 3% Indian steel demand to start accelerating New low cost projects to improve the return ratios. Upgrade to BUY

- 5. 28 May 2014 5 JSW Steel JSW Steel: an investment profile Company description JSTL demonstrated excellent project execution skills over the past decade, growing its annual capacity 6x to 10m tons through Brownfield expansions at Vijaynagar. With the acquisition of Ispat Industries and Salem Steel, it controls annual capacity of 14.3mtpa. Its main production facilities are located in proximity to rich iron ore reserves in Karnataka. It has investments in iron ore mining in Chile. Its other overseas investments include plate and pipe mill operations and coal mines in the US. Key investment arguments JSTL has the lowest conversion cost due to operational efficiencies. Its strategic location near the iron ore rich Bellary-Hospet belt helps it to keep iron ore purchase costs low. However, the restricted iron ore mining in Bellary and Odisha has posed major challenges for company. New CRM-II at Vijaynagar will enrich product mix. Pellet and Coke oven facilities will bring down the cost of production at Dolvi unit Key investment risks Iron ore availability and costing is key risk to margins. Recent developments India’s most sophisticated 2.3mtpa CRM-II complex was commissioned on 25th April. This mill is equipped with latest technology to produce continuously annealed CR upto 980 MPA (UTS) for auto sector Valuation and view Stock is trading at EV/EBITDA of 6.8xFY15. Upgrade to BUY on higher volumes and better margins Sector outlook We believe that Indian steel demand growth has hit bottom in FY14. We expect Indian steel demand growth to accelerate to 4% in FY15 and 6% in FY16. The conversion spreads for steel mills are expanding on global demand (ex-China) growth and oversupply of iron ore and coking coal. Comparative valuations JSW Steel SAIL TATA STEEL P/E (x) FY15E 10.8 12.8 8.8 FY16E 10.8 10.3 6.5 P/BV (x) FY15E 1.2 0.8 1.5 FY16E 1.1 0.8 1.2 EV/Sales (x) FY15E 1.3 1.3 0.8 FY16E 1.2 1.3 0.8 EV/EBITDA (x) FY15E 6.8 9.4 6.3 FY16E 6.4 7.7 5.6 EPS: MOSL forecast v/s consensus (INR) MOSL Consensus Variation Forecast Forecast (%) FY15 113.4 97.7 16.0 FY16 113.3 110.0 3.0 Target price and recommendation Current Target Upside Reco. Price (INR) Price (INR) (%) 1,228 1,473 20.0 BUY Shareholding pattern (%) Mar-14 Dec-13 Mar-13 Promoter 39.0 37.8 38.6 Domestic Inst 3.6 4.4 4.5 Foreign 38.9 38.4 40.8 Others 18.5 19.4 16.1 Stock performance (1-year)

- 6. 28 May 2014 6 JSW Steel Financials and valuation Income statement (INR Billion) Y/E March 2013 2014 2015E 2016E Net Sales 382.1 512.2 545.4 568.5 Change (%) 11.2 34.0 6.5 4.2 EBITDA 65.0 91.7 104.7 107.9 EBITDA Margin (%) 17.0 17.9 19.2 19.0 Depreciation 22.4 31.8 34.3 36.0 EBIT 42.7 59.8 70.4 71.9 Interest 19.7 30.5 31.3 33.0 Other Income 0.7 0.9 1.3 1.5 Extraordinary items -4.3 -17.1 0.0 0.0 PBT 19.4 13.1 40.4 40.4 Tax 8.5 9.2 12.2 12.2 Tax Rate (%) 43.6 70.3 30.1 30.2 Reported PAT 10.9 3.9 28.2 28.2 Adjusted PAT 15.2 21.0 28.2 28.2 Change (%) -34.3 37.9 34.4 -0.1 Min. Int. & Assoc. Share -2.0 -0.4 -0.5 -0.5 Adj Cons PAT 11.1 8.3 27.4 27.4 Balance sheet (INR Billion) Y/E March 2013 2014 2015E 2016E Share Capital 2.2 2.4 2.4 2.4 Reserves 168.4 217.0 241.0 265.0 Net Worth 170.6 219.4 243.4 267.4 Debt 310.1 429.0 429.0 429.0 Deferred Tax 32.7 21.2 25.3 29.5 Total Capital Employed 515.4 671.3 698.7 726.2 Gross Fixed Assets 458.7 691.2 771.2 831.2 Less: Acc Depreciation 111.5 217.7 252.0 288.0 Net Fixed Assets 347.2 473.5 519.2 543.2 Capital WIP 66.0 91.0 86.0 71.0 Investments 16.1 5.9 5.9 5.9 Current Assets 120.6 206.0 224.5 245.8 Inventory 55.0 81.6 89.7 93.5 Debtors 21.1 22.9 22.4 23.4 Cash & Bank 18.0 7.3 18.3 34.8 Loans & Adv, Others 26.6 94.2 94.2 94.2 Curr Liabs & Provns 34.3 105.1 136.9 139.8 Curr. Liabilities 30.9 35.4 67.2 70.1 Provisions 3.5 69.7 69.7 69.7 Net Current Assets 86.2 100.9 87.6 106.0 Total Assets 515.4 671.3 698.7 726.2 E: MOSL Estimates Ratios Y/E March 2013 2014 2015E 2016E Basic (INR) EPS 49.7 34.4 113.4 113.3 Cash EPS 148.7 164.9 254.2 260.9 Book Value 764.8 907.5 1,006.9 1,106.2 DPS 10.0 11.0 11.0 11.0 Payout (incl. Div. Tax.) 20.5 37.4 12.4 12.4 Valuation(x) P/E 24.7 35.7 10.8 10.8 Cash P/E 8.3 7.4 4.8 4.7 Price / Book Value 1.6 1.4 1.2 1.1 EV/Sales 1.5 1.4 1.3 1.2 EV/EBITDA 8.7 7.8 6.8 6.4 Dividend Yield (%) 0.8 0.9 0.9 0.9 Profitability Ratios (%) RoE 7.7 10.4 11.8 10.7 RoCE 8.4 10.3 10.6 10.4 Turnover Ratios (%) Asset Turnover (x) 0.8 0.9 0.8 0.8 Debtors (No. of Days) 20.1 16.3 15.0 15.0 Inventory (No. of Days) 52.5 58.1 60.0 60.0 Creditors (No. of Days) 35.5 30.8 55.7 55.5 Leverage Ratios (%) Net Debt/Equity (x) 1.8 2.0 1.8 1.6 Cash flow statement (INR Billion) Y/E March 2013 2014 2015E 2016E OP/(Loss) before Tax 23.0 29.4 39.1 39.0 Depreciation 22.4 31.8 34.3 36.0 Others -0.7 -0.9 -1.3 -1.5 Interest 19.7 30.5 31.3 33.0 Direct Taxes Paid -5.1 -2.6 -8.1 -8.1 (Inc)/Dec in Wkg Cap 5.9 -44.2 24.2 -1.9 CF from Op. Activity 57.7 44.0 118.0 95.0 (Inc)/Dec in FA & CWIP -56.3 -56.9 -75.0 -45.0 (Pur)/Sale of Invt 0.8 0.0 0.0 0.0 Others 1.1 0.9 1.3 1.5 CF from Inv. Activity -54.5 -56.0 -73.7 -43.5 Inc/(Dec) in Net Worth 0.0 0.0 0.0 0.0 Inc / (Dec) in Debt 9.5 34.1 0.0 0.0 Interest Paid -15.2 -30.5 -31.3 -33.0 Divd Paid (incl Tax) -2.3 -3.1 -3.4 -3.4 CF from Fin. Activity -7.2 1.4 -33.4 -34.9 Inc/(Dec) in Cash -3.9 -10.7 10.9 16.5 Add: Opening Balance 22.5 18.0 7.3 18.3 Closing Balance 18.6 7.3 18.3 34.8

- 7. 28 May 2014 7 JSW Steel N O T E S

- 8. 28 May 2014 8 JSW SteelDisclosures This report is for personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducement to invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOSt or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays. The information contained herein is based on publicly available data or other sources believed to be reliable. While we would endeavour to update the information herein on reasonable basis, MOSt and/or its affiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates or employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. MOSt or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations. This report is intended for distribution to institutional investors. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of Interest Statement in this document. This should, however, not be treated as endorsement of the views expressed in the report. Disclosure of Interest Statement JSW STEEL LTD 1. Analyst ownership of the stock No 2. Group/Directors ownership of the stock No 3. Broking relationship with company covered No 4. Investment Banking relationship with company covered No Analyst Certification The views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsible for preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues. Regional Disclosures (outside India) This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions. For U.K. This report is intended for distribution only to persons having professional experience in matters relating to investments as described in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (referred to as "investment professionals"). This document must not be acted on or relied on by persons who are not investment professionals. Any investment or investment activity to which this document relates is only available to investment professionals and will be engaged in only with such persons. For U.S. Motilal Oswal Securities Limited (MOSL) is not a registered broker - dealer under the U.S. Securities Exchange Act of 1934, as amended (the"1934 act") and under applicable state laws in the United States. In addition MOSL is not a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the "Acts), and under applicable state laws in the United States. Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by MOSL, including the products and services described herein are not available to or intended for U.S. persons. This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutional investors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major institutional investors and will be engaged in only with major institutional investors. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S., MOSL has entered into a chaperoning agreement with a U.S. registered broker-dealer, Motilal Oswal Securities International Private Limited. ("MOSIPL"). Any business interaction pursuant to this report will have to be executed within the provisions of this chaperoning agreement. The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker- dealer, MOSIPL, and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account. For Singapore Motilal Oswal Capital Markets Singapore Pte Limited is acting as an exempt financial advisor under section 23(1)(f) of the Financial Advisers Act(FAA) read with regulation 17(1)(d) of the Financial Advisors Regulations and is a subsidiary of Motilal Oswal Securities Limited in India. This research is distributed in Singapore by Motilal Oswal Capital Markets Singapore Pte Limited and it is only directed in Singapore to accredited investors, as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. In respect of any matter arising from or in connection with the research you could contact the following representatives of Motilal Oswal Capital Markets Singapore Pte Limited: Anosh Koppikar Kadambari Balachandran Email : anosh.koppikar@motilaloswal.com Email : kadambari.balachandran@motilaloswal.com Contact: (+65) 68189232 Contact: (+65) 68189233 / 65249115 Office address: 21 (Suite 31), 16 Collyer Quay, Singapore 04931 Motilal Oswal Securities Ltd Motilal Oswal Tower, Level 9, Sayani Road, Prabhadevi, Mumbai 400 025 Phone: +91 22 3982 5500 E-mail: reports@motilaloswal.com