Simple balance sheet

•Download as PPTX, PDF•

1 like•903 views

Simple classified balance sheet

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Simple balance sheet

Similar to Simple balance sheet (20)

More from Dyann Barras

More from Dyann Barras (20)

Recently uploaded

Recently uploaded (20)

Simple balance sheet

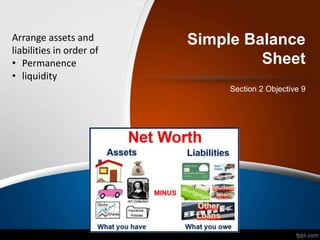

- 1. Classified Balance Sheet Section 2 Objective 9 o Arrange assets and liabilities in order of • Permanence • Liquidity o Prepare balance sheet

- 2. Classified Balance Sheet • The Balance Sheet shows a listing of a firm’s assets, liabilities and capital at a particular date • Assets and Liabilities in a balance sheet are classified and shown in categories • The assets and liabilities can be arranged in order of permanence or liquidity

- 5. • Assets – Assets are classified into two categories. • Current assets are assets owned by the business for a short period time. They are quickly turned into cash within one year. Examples of current assets include cash in hand, cash at bank, inventory and accounts receivable (debtors) • Non-currents assets are those which a business intends to keep and used to generate income for a long period of time (for more than one year). Examples of non- current assets include premises, machinery, equipment and vehicles Classified Balance Sheet

- 7. • Liabilities – Liabilities are classified into two categories. • Current liabilities are sums of money owed to individuals or firms which will be settled in less than one year. Examples of current liabilities are accounts payable (creditors) and bank overdraft • Non-current liabilities are sums of money owed to individuals or firms which will be settled in more than one year. Examples of non-current liabilities are mortgage loans and bank loans Classified Balance Sheet

- 9. The date at which it is being prepared e.g. as at February 28, 2017 When preparing the balance sheet, show the following information in the heading: The name of the organisation e.g. DB Enterprises The name of the financial statement e.g. Balance Sheet (ask you self these questions?) Classified Balance Sheet

- 10. • Presentation of the Balance Sheet – Style – Assets and Liabilities in a Balance Sheet can be arranged in two styles. – The styles are order of permanence and order of liquidity: • Order of permanence presentation in the balance sheet, assets are placed first. • It reflects the length of time each asset is expected to benefit. Classified Balance Sheet

- 11. • Non-current assets are placed first, starting with the asset that will last longer than one year • Current assets are shown in the following order of permanency – Inventory – Receivables (Debtors) – Bank – Cash • In the other half of the balance sheet, the capital and liabilities categories are shown in the following order permanency: • Capital • Non-current liabilities • Current liabilities Classified Balance Sheet

- 12. Classified Balance Sheet order of permanenceEXAMP LE OF S IMP LE B ALAN CE S H EET SB. E n terprises $ $ $ Ba la n ce Sh eet a s a t 31 J u ly 2018 N o n -c u rre n t As s e ts La n d & Bu ildin g * F ixtu res a n d F ittin gs * E qu ipm en t * ** Cu rre n t As s e ts In ven tory * Accou n ts receiva ble * Ca sh a t ba n k * Ca sh in h a n d * ** *** Ca pita l ** N o n -Cu rre n t Lia bility Mortga ge * Ba n k Loa n * ** Cu rre n t Lia bility Accou n ts pa ya bles * Ba n k overdra ft * ** ***

- 13. • Balance sheet style of presentation for order of liquidity: – shows the assets (that is current assets) which are already in cash form first – and the assets which are more difficult to convert to cash in the near future last. • The order of presentation starts with cash in hand and ends with inventories or prepaid expenses. • For the other half of the balance sheet, current liabilities will be shown before non-current liabilities and capital will be placed last. Classified Balance Sheet

- 14. Classified Balance Sheet order of liquidity EXAMP LE OF S IMP LE B ALAN CE S H EET SB. E n terprises $ $ $ Ba la n ce Sh eet a s a t 31 J u ly 2018 Cu rre n t As s e ts Ca sh in h a n d * Ca sh a t ba n k * Accou n ts receiva bles * In ven tory * ** N o n -c u rre n t As s e ts E qu ipm en t * F ixtu res a n d F ittin gs * La n d a n d Bu ildin g * ** *** Cu rre n t Lia bility Accou n ts pa ya bles * Ba n k overdra ft * ** N o n -Cu rre n t Lia bility Ba n k Loa n * Mortga ge * ** Ca pita l ** ***

- 15. When preparing a Balance Sheet • Show the following information on the balance sheet – The name of the firm – The name of the financial statement – The date at which it is being prepared • Use either the style of order or presentation or order for liquidity (not both together) • Total each part of the balance sheet Classified Balance Sheet

- 16. • Look at the link on the next slide and watch the video on creating a simple balance sheet • Create a Simple Balance Sheet Ptionline division https://www.youtube.com/w atch?v=QYA0GiSQ524 Simple Balance Sheet