FNB_House Price Indices by Segment

•

0 likes•57 views

FNB_House Price Indices by Segment

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to FNB_House Price Indices by Segment

Similar to FNB_House Price Indices by Segment (20)

More from Berty Van Staaden

More from Berty Van Staaden (20)

Recently uploaded

Recently uploaded (20)

FNB_House Price Indices by Segment

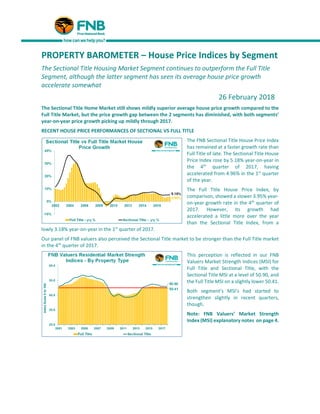

- 1. PROPERTY BAROMETER – House Price Indices by Segment The Sectional Title Housing Market Segment continues to outperform the Full Title Segment, although the latter segment has seen its average house price growth accelerate somewhat 26 February 2018 The Sectional Title Home Market still shows mildly superior average house price growth compared to the Full Title Market, but the price growth gap between the 2 segments has diminished, with both segments’ year-on-year price growth picking up mildly through 2017. RECENT HOUSE PRICE PERFORMANCES OF SECTIONAL VS FULL TITLE The FNB Sectional Title House Price Index has remained at a faster growth rate than Full Title of late. The Sectional Title House Price Index rose by 5.18% year-on-year in the 4th quarter of 2017, having accelerated from 4.96% in the 1st quarter of the year. The Full Title House Price Index, by comparison, showed a slower 3.95% year- on-year growth rate in the 4th quarter of 2017. However, its growth had accelerated a little more over the year than the Sectional Title Index, from a lowly 3.18% year-on-year in the 1st quarter of 2017. Our panel of FNB valuers also perceived the Sectional Title market to be stronger than the Full Title market in the 4th quarter of 2017. This perception is reflected in our FNB Valuers Market Strength Indices (MSI) for Full Title and Sectional Title, with the Sectional Title MSI at a level of 50.90, and the Full Title MSI on a slightly lower 50.41. Both segment’s MSI’s had started to strengthen slightly in recent quarters, though. Note: FNB Valuers’ Market Strength Index (MSI) explanatory notes on page 4.

- 2. SECTIONAL TITLE SUB-SEGMENT PERFORMANCES Within the Sectional Title segment, “smaller was still better” in the 4th quarter of 2017 when one compares the relative strength of the various sub-segments’ price growth. The smallest sized Sectional Title sub- segment, namely the “Less than 2 Bedroom” segment, showed the strongest price inflation to the tune of 7.3% in the 4th quarter of 2017. Then came the 2 Bedroom sub-segment with 6.4% price growth, while the largest “3 Bedroom and More” category was the slowest sub- segment with 3.6% average price growth. However, it was the 2 Bedroom Sub-Segment that was the onlyone of the 3 to be showing house price growth acceleration through 2017, from 4.9% in the final quarter of 2016 to 6.4% by the end of 2017, the other 2 sub-segments showing slowing price growth through the year. FULL TITLE SUB-SEGMENT PERFORMANCES In the Full Title segment, the popular 3 Bedroom segment has shown the highest average price growth of the 3 sub- segments, to the tune of 4.2% year-on- year in the 4th quarter of 2017. The relatively expensive 4 Bedroom and More Full Title Segment saw a slower growth rate of 3.7%, while the smallest sized 2 Bedroom-and-Less segment was the weakest with 3.3%. AVERAGE PRICE GAP BETWEEN FULL TITLE AND SECTIONAL TITLE MARKETS CONTINUES TO NARROW Taking a simple percentage differential between the average Full Title house price and that of Sectional Title, the outperformance of Sectional Title in recent years has reduced the gap by which the average Full Title house price exceeds that of the smaller-sized Sectional Title category, from a revised 26.6% as at the end of 2013 to 22.2% by the 4th quarter of 2017.

- 3. LONG TERM PERFORMANCES OF MAJOR HOUSING MARKET SEGMENTS In a view of the long term performance of our major FNB Segment House Price Indices, the smaller sized Sectional Title homes with their more efficient use of land have clearly been the cumulative outperformers since the beginning of 2001 around the time when the data series’ started. This is hardly surprising, given the mounting scarcity of available urban land and infrastructure (including scarcity of new transport infrastructure, which limits urban sprawl potential) for new residential development. Top performer has been the Sectional Title Less than 2 Bedroom Segment, with cumulative average price inflation of 496.89% from the 1st quarter of 2001 to the 4th quarter of 2017. This far outstrips the 2nd placed Sectional Title 2 Bedroom Segment’s 376.36% and the Sectional Title 3 Bedroom and More Segment’s 352.98%. The 3 Full Title Segments have “underperformed”, the more popular 3 Bedroom Segment’s 331.41% neck and neck with the 4 Bedroom and More Segment’s 336.71%, but outstripping the far more affordable 2 Bedrooms and Less Segment’s 284.46%. CONCLUSION The FNB Valuers perceive the Sectional Title market to be stronger than that of Full Title, and superior average house price growth in the Sectional Title market appears to reflect this. However, the year-on-year price growth rates in both Sectional and Full Title segments accelerated as 2017 progressed, the latter’s growth accelerating more than the former off a lower base. The pattern of smaller-sized unit segments outperforming the larger ones is becoming less clear as of late, however. In the Full Title Segment, the smallest average sized segment, the “2-Bedroon and Less” segment has recently shown the slowest growth in the main Full Title sub-segments, while in the Sectional Title segment it is the mid-sized 2-Bedroom sub-segment which has been the only one recently showing average house price growth acceleration. It may be that, after some years of smaller sized sub-segments outperforming the larger ones in terms of price growth, larger sized home now begin to offer relatively better value for money, which could mean that in 2018 we don’t smaller segments clearly outperforming on price growth.

- 4. ADDENDUM - NOTES: Key notes with regard to the FNB Segment House Price Indices by Title and Room Number: • The Indices are constructed using transaction price data from homes financed by FNB. • The minimum size cut-off for full title stands is 200 square metres, and the maximum size is 4000 square metres • The maximum price cut-off is R10m, and the lower price cut-off is R20,000 (largely to eliminate major outliers and glaring inputting errors). • The indices are very lightly smoothed using a Hodrick-Prescott smoothing function with a Lambda of 5. Note on the FNB Valuers’ Market Strength Index: *When an FNB valuer values a property, he/she is required to provide a rating of demand as well as supply for property in the specific area. The demand and supply rating categories are a simple “good (100)”, “average (50)”, and “weak (0)”. From all of these ratings we compile an aggregate demand and an aggregate supply rating, which are expressed on a scale of 0 to 100. After aggregating the individual demand and supply ratings, we subtract the aggregate supply rating from the demand rating, add 100 to the difference, and divide by 2, so that the FNB Valuers’ Residential Market Strength Index is also depicted on a scale of 0 to 100 with 50 being the point where supply and demand are equal. JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za The information in this publication is derived from sources which are regarded as accurate and reliable, is of a general nature only, does not constitute advice and may not be applicable to all circumstances. Detailed advice should be obtained in individual cases. No responsibility for any error, omission or loss sustained by any person acting or refraining from acting as a result of this publication is accepted by Firstrand Group Limited and / or the authors of the material. First National Bank – a division of FirstRand Bank Limited. An Authorised Financial Services provider. Reg No. 1929/001225/06

- 5. SEGMENT PERFORMANCES • Sectional Title vs Full Title • Full Title

- 6. • Sectional Title • Sectional Title Per Square Metre • Home Size Segments 50.38 52.11 50.88 35 40 45 50 55 60 65 2001 2003 2005 2007 2009 2011 2013 2015 2017 IndexScale0to100 FNB Valuers Residential Market Strength Indices - Sectional Title 3 Bedrooms Less than 2 Bedrooms 2 Bedrooms

- 7. • Existing Homes vs Vacant Land

- 8. 2015 2016 2017 Q1-2017 Q2-2017 Q3-2017 Q4-2017 FULL TITLE SEGMENT Full Title Average Price (Rand) 1 093 590 1 149 616 1 189 453 1 171 655 1 183 276 1 195 148 1 207 733 - year-on-year % change 6.4% 5.1% 3.5% 3.2% 3.2% 3.5% 3.9% - quarter-on-quarter % change 0.8% 1.0% 1.0% 1.1% 2 Bedrooms and Less (Rand) 601 037 640 736 658 645 649 920 655 199 661 652 667 811 - year-on-year % change 7.7% 6.6% 2.8% 2.8% 2.4% 2.7% 3.3% - quarter-on-quarter % change 0.5% 0.8% 1.0% 0.9% 3 Bedroom (Rand) 1 107 127 1 164 908 1 208 484 1 189 766 1 202 779 1 214 609 1 226 782 - year-on-year % change 5.9% 5.2% 3.7% 3.4% 3.5% 3.9% 4.2% - quarter-on-quarter % change 1.0% 1.1% 1.0% 1.0% 4 Bedrooms and More (Rand) 1 724 817 1 776 845 1 831 652 1 805 077 1 820 920 1 839 816 1 860 795 - year-on-year % change 4.4% 3.0% 3.1% 2.6% 2.8% 3.2% 3.7% - quarter-on-quarter % change 0.6% 0.9% 1.0% 1.1% AVERAGE HOUSE PRICE BY MAJOR FULL TITLE SEGMENT

- 9. 2015 2016 2017 Q1-2017 Q2-2017 Q3-2017 Q4-2017 SECTIONAL TITLE SEGMENT AVERAGE HOUSE PRICE Sectional Title Average House Price (Rand) 815 463 875 988 924 796 951 996 964 613 976 706 988 626 - year-on-year % change 7.1% 7.4% 5.6% 5.0% 5.1% 5.2% 5.2% - quarter-on-quarter % change 1.3% 1.3% 1.3% 1.2% Less than 2 Bedroom (Rand) 637 723 712 314 772 213 752 704 767 368 779 258 789 523 - year-on-year % change 12.6% 11.7% 8.4% 9.3% 8.9% 8.3% 7.3% - quarter-on-quarter % change 2.3% 1.9% 1.5% 1.3% 2 Bedroom (Rand) 766 827 809 616 855 724 835 625 848 761 862 124 876 386 - year-on-year % change 7.3% 5.6% 5.7% 5.0% 5.5% 5.9% 6.4% - quarter-on-quarter % change 1.4% 1.6% 1.6% 1.7% 3 Bedrooms and More (Rand) 1 158 774 1 213 531 1 262 171 1 245 295 1 257 285 1 268 281 1 277 825 - year-on-year % change 6.1% 4.7% 4.0% 4.3% 4.2% 3.9% 3.6% - quarter-on-quarter % change 1.0% 1.0% 0.9% 0.8% SECTIONAL TITLE PER SQUARE METRE Sectional Title Average Price (Rand/square metre) 9 780 10 499 11 209 10 939 11 117 11 295 11 484 - year-on-year % change 8.3% 7.3% 6.8% 6.8% 6.8% 6.8% 6.8% - quarter-on-quarter % change 1.7% 1.6% 1.6% 1.7% Less than 2 Bedroom (Rand/square metre) 12 277 13 819 15 255 14 754 15 099 15 419 15 749 - year-on-year % change 12.4% 12.6% 10.4% 11.0% 10.7% 10.3% 9.7% - quarter-on-quarter % change 2.7% 2.3% 2.1% 2.1% 2 Bedroom (Rand/square metre) 9 781 10 413 11 096 10 810 10 996 11 186 11 391 - year-on-year % change 7.5% 6.5% 6.6% 6.0% 6.4% 6.7% 7.1% - quarter-on-quarter % change 1.6% 1.7% 1.7% 1.8% 3 Bedrooms and More (Rand/square metre) 8 660 9 108 9 474 9 354 9 430 9 513 9 600 - year-on-year % change 7.3% 5.2% 4.0% 4.5% 4.2% 3.8% 3.6% - quarter-on-quarter % change 0.9% 0.8% 0.9% 0.9% AVERAGE HOUSE PRICE BY MAJOR SECTIONAL TITLE SEGMENT

- 10. 2015 2016 2017 Q1-2017 Q2-2017 Q3-2017 Q4-2017 HOUSE PRICES BY HOME SIZE Large Homes (Rand) 1 898 346 1 953 320 2 085 953 2 027 753 2 069 185 2 105 596 2 141 277 - year-on-year % change 3.8% 2.9% 6.8% 5.5% 6.7% 7.4% 7.6% - quarter-on-quarter % change 1.9% 2.0% 1.8% 1.7% Medium Sized Homes (Rand) 1 050 226 1 106 532 1 145 067 1 130 479 1 141 033 1 150 195 1 158 559 - year-on-year % change 6.4% 5.4% 3.5% 3.7% 3.5% 3.4% 3.4% - quarter-on-quarter % change 0.9% 0.9% 0.8% 0.7% Small Sized Homes (Rand) 566 176 613 802 651 383 637 507 647 115 656 043 664 866 - year-on-year % change 8.4% 8.4% 6.1% 6.3% 6.1% 6.1% 6.0% - quarter-on-quarter % change 1.6% 1.5% 1.4% 1.3% AVERAGE HOUSE PRICE BY SIZE CATEGORY