Download as PDF, PPTX

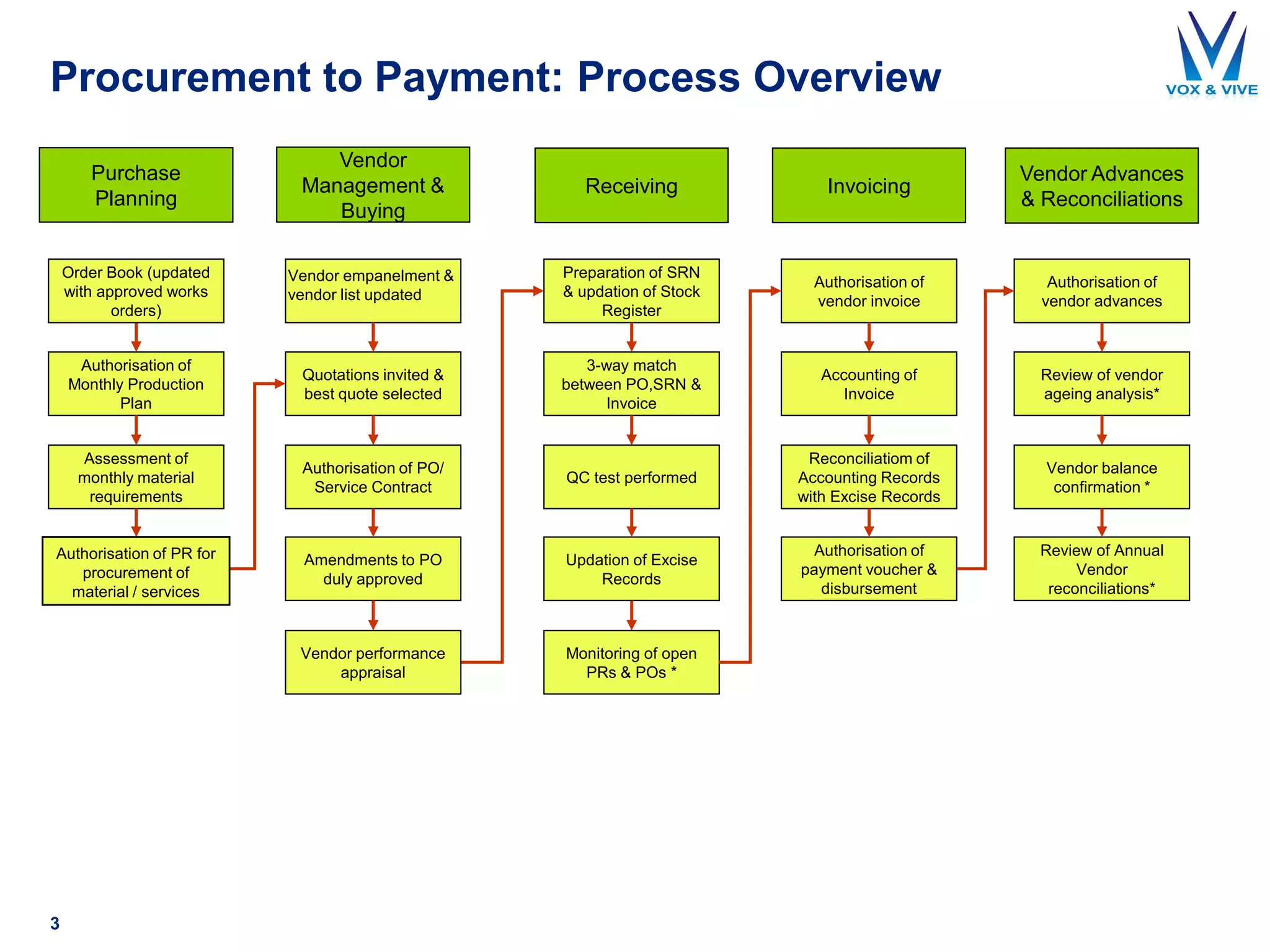

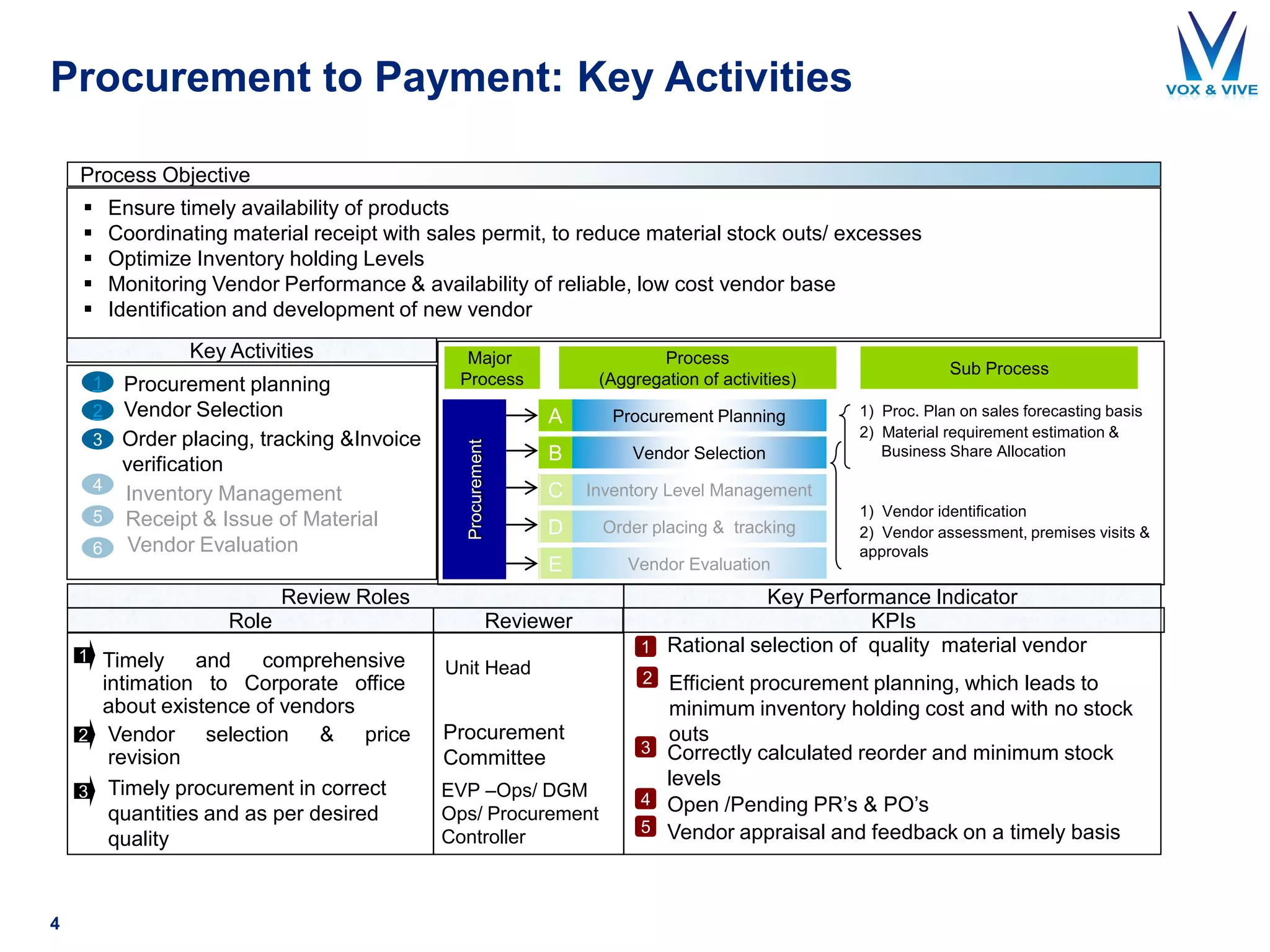

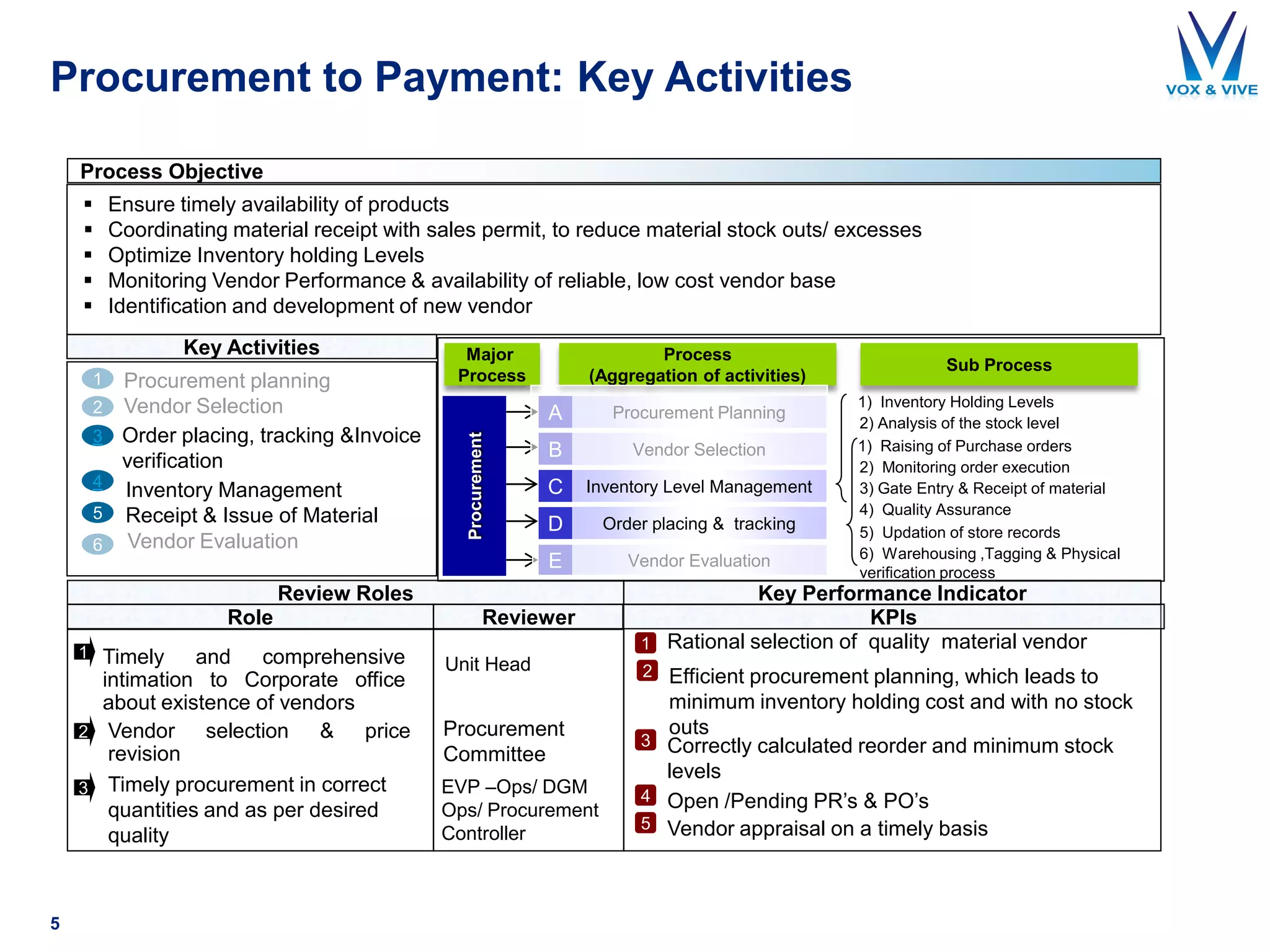

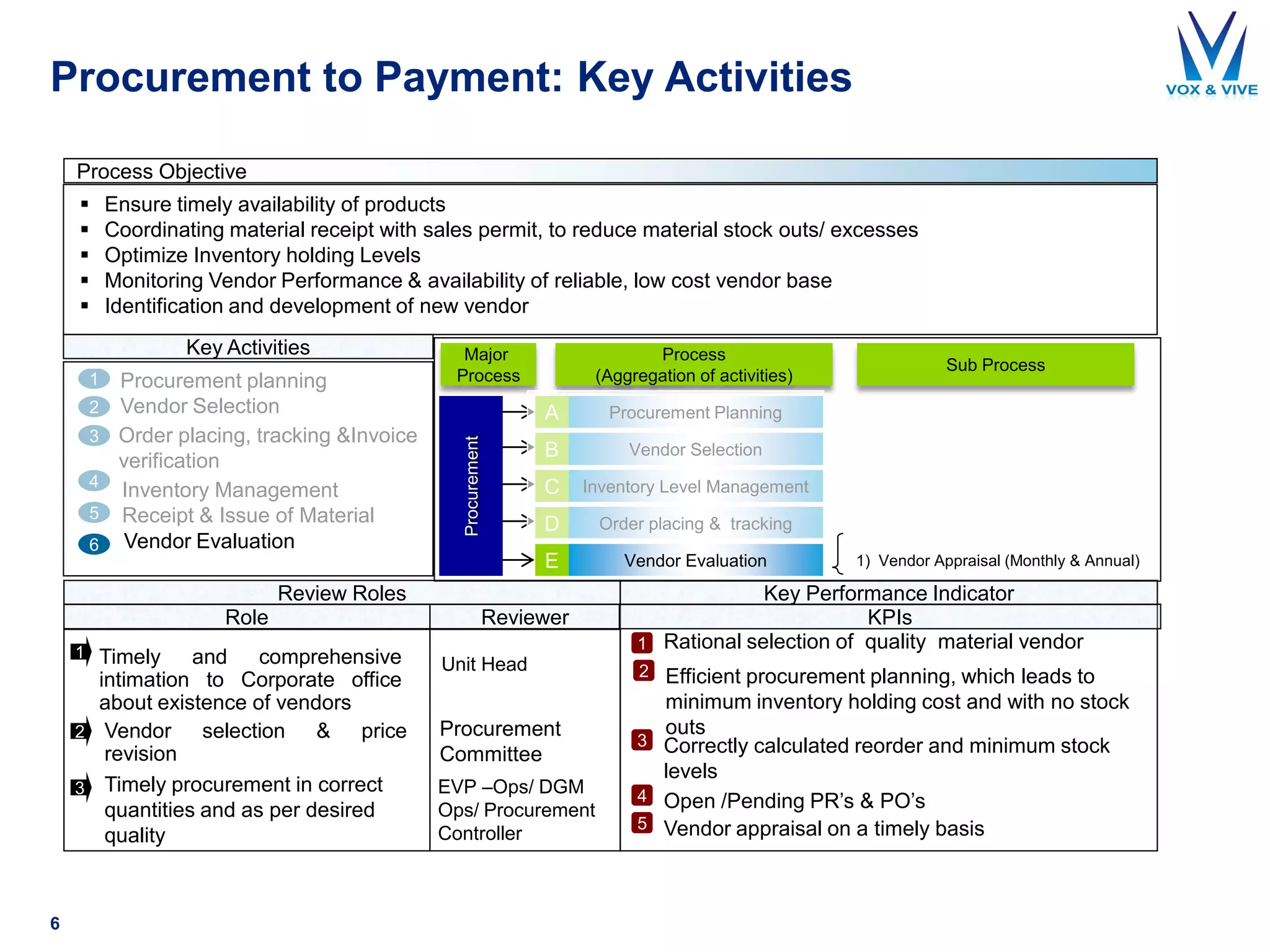

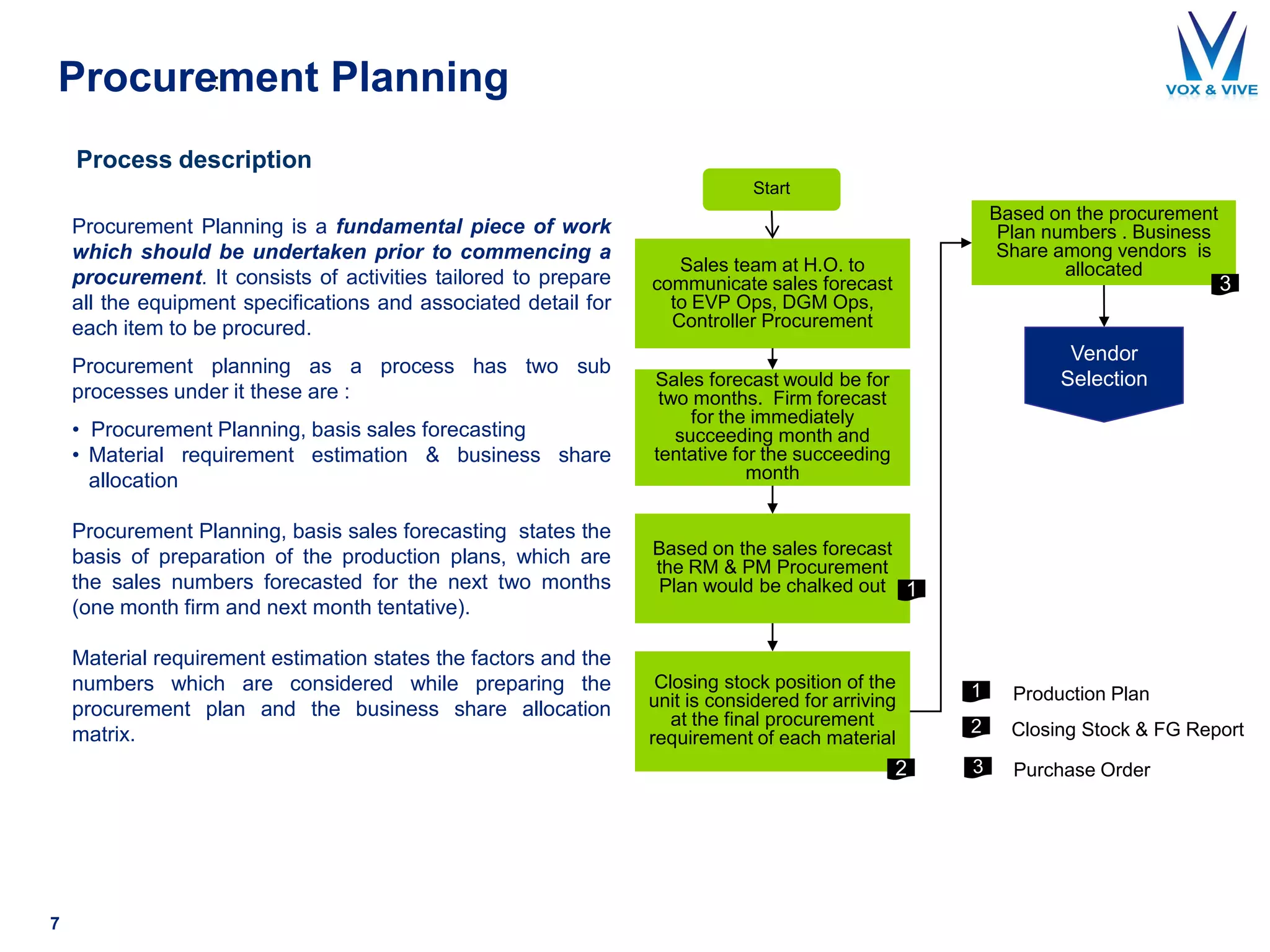

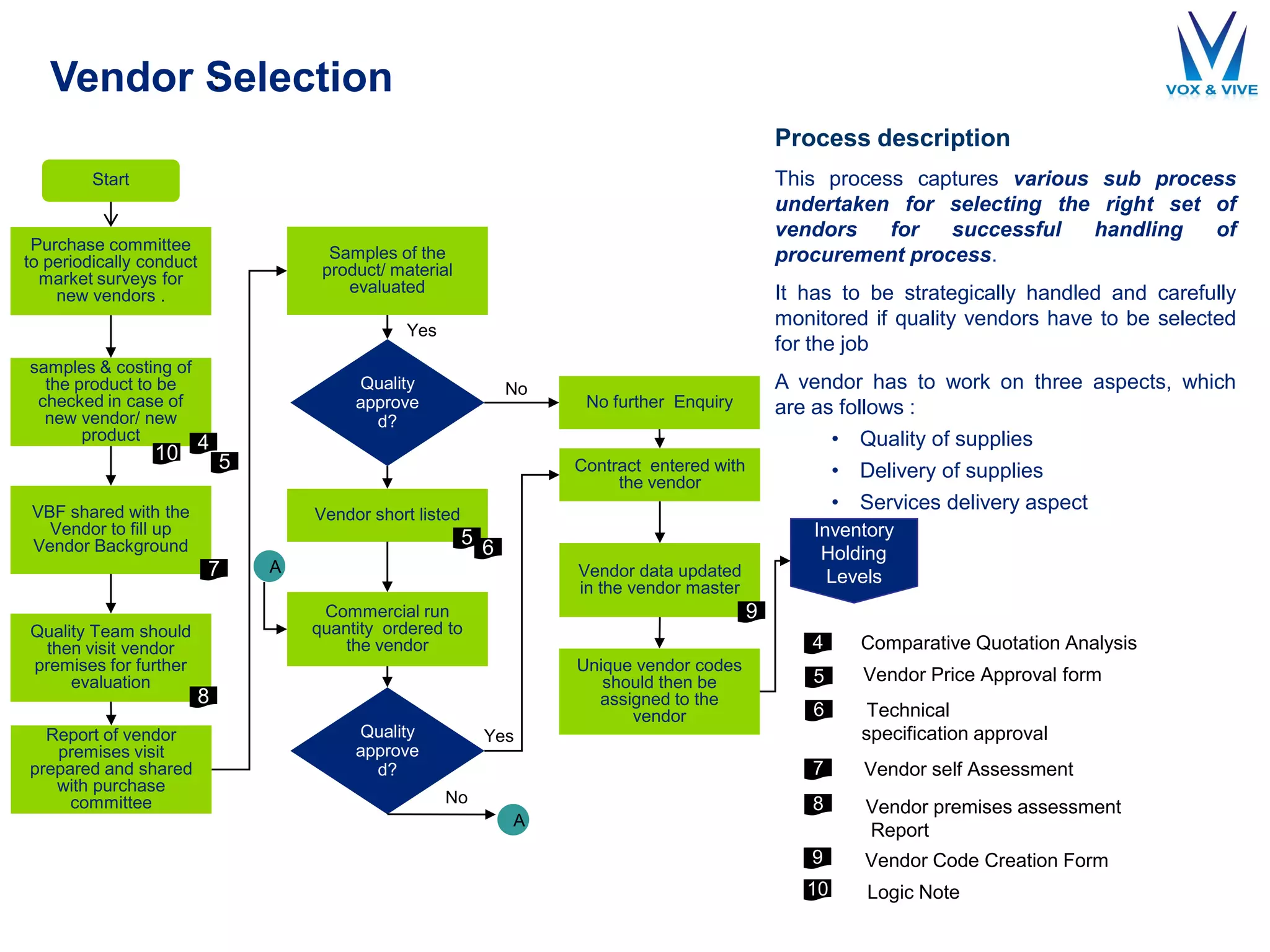

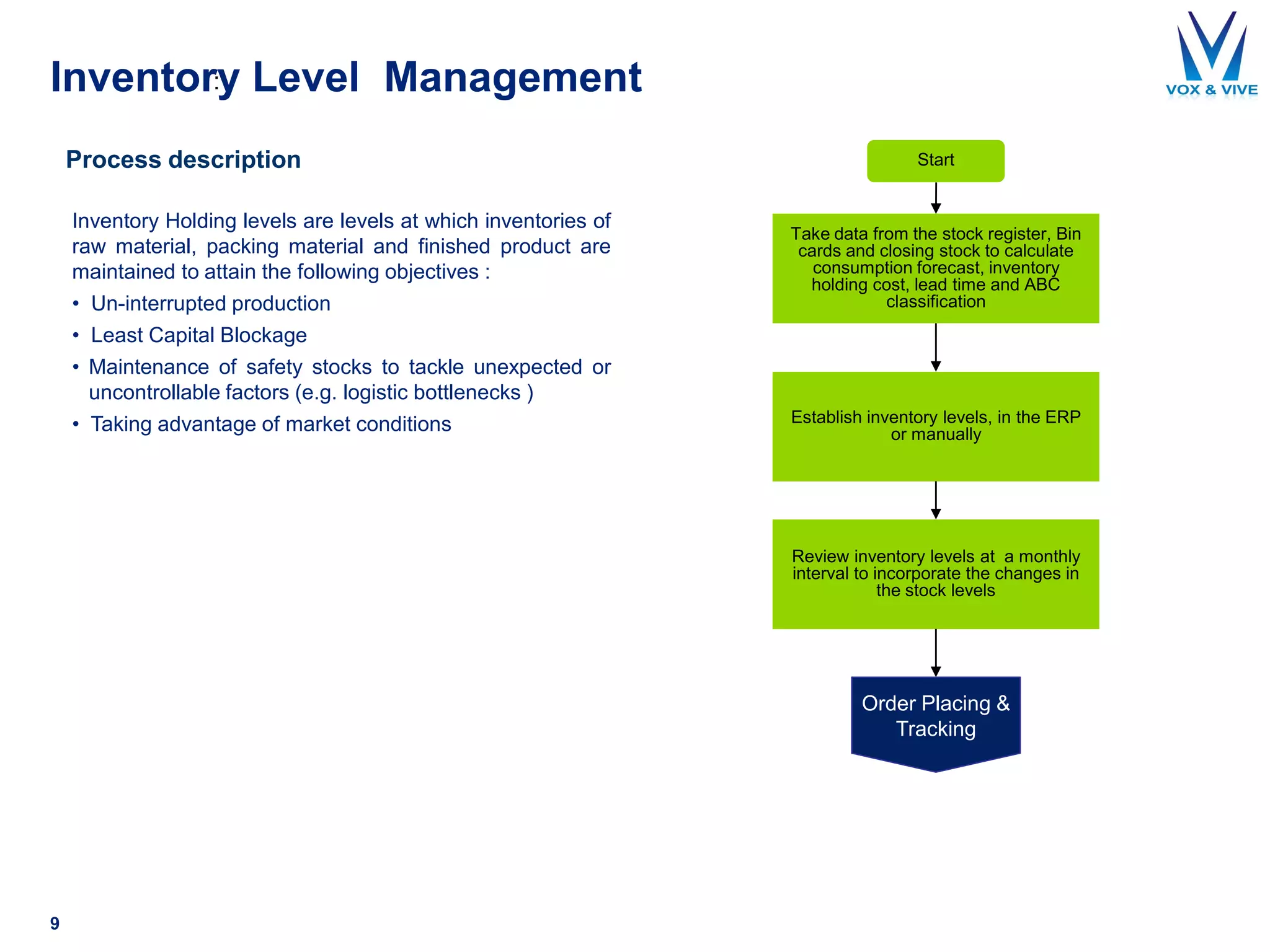

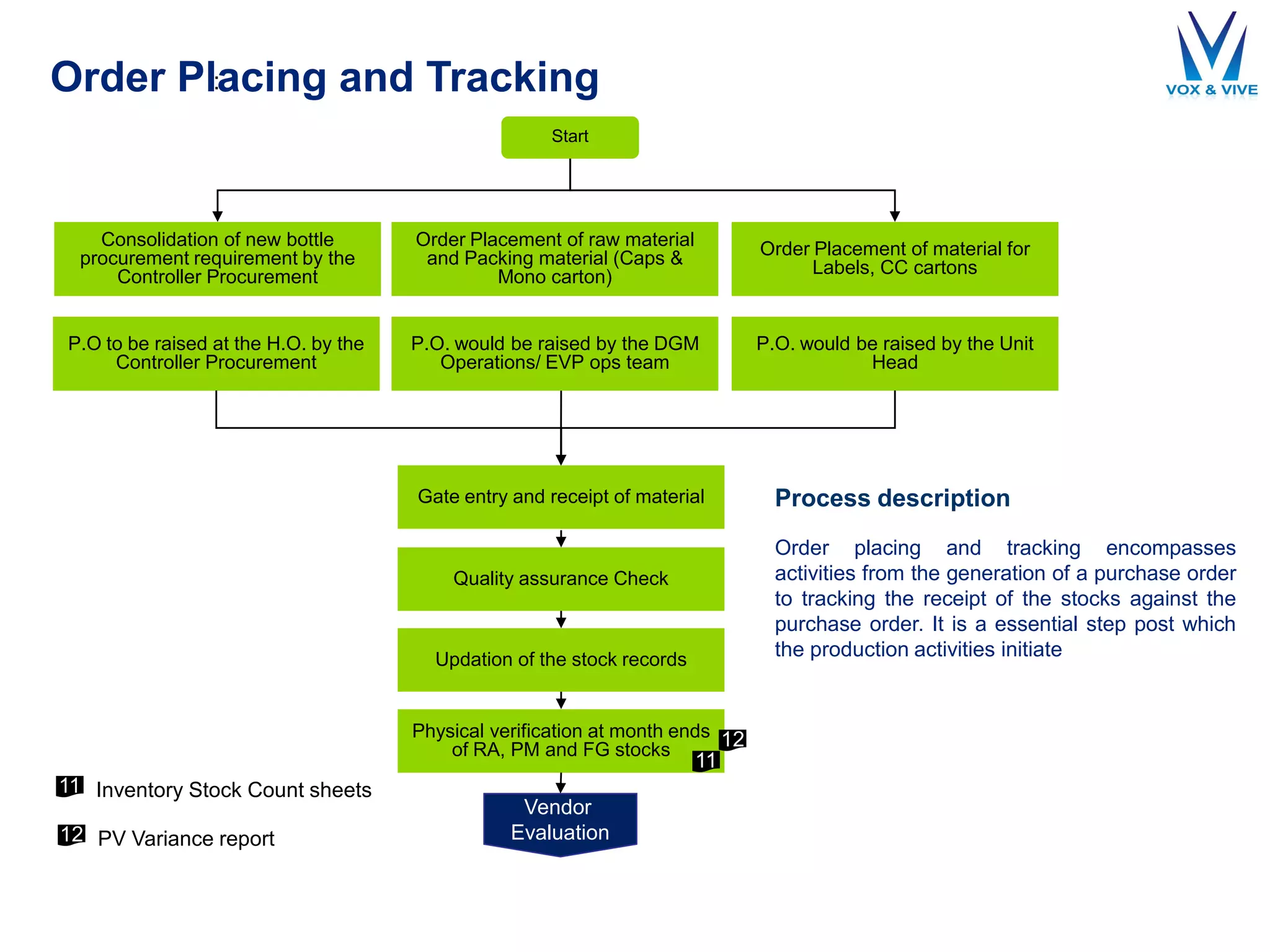

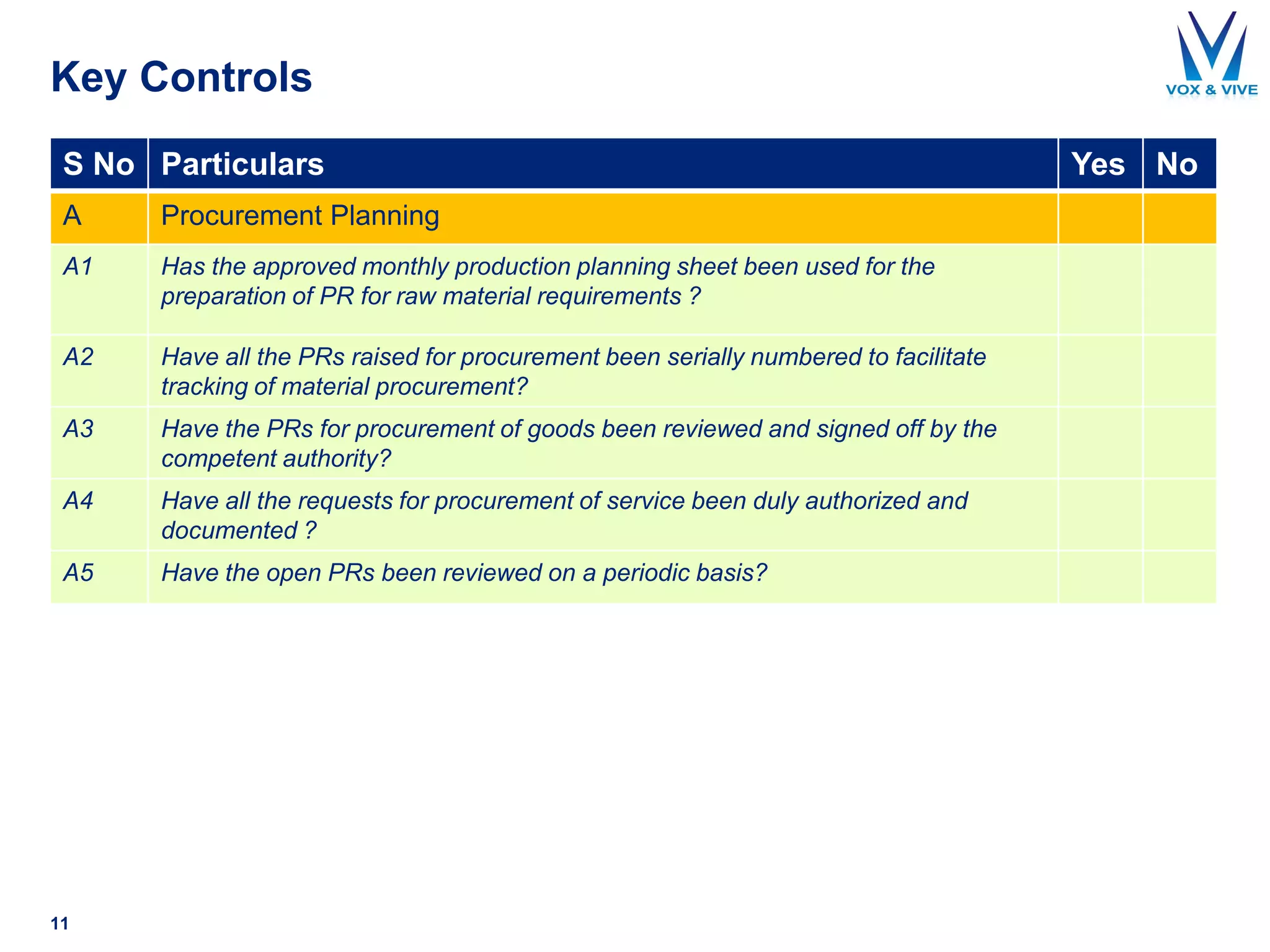

The document outlines the business process for procurement to payment, detailing the key activities, roles, and controls necessary for effective procurement management. It includes descriptions of vendor selection, inventory management, order placing, tracking, and invoice processing, emphasizing performance indicators for each activity. Additionally, the document highlights the importance of timely communication and rigorous monitoring of vendor and inventory levels to ensure efficient procurement processes.