Downloaded 1,191 times

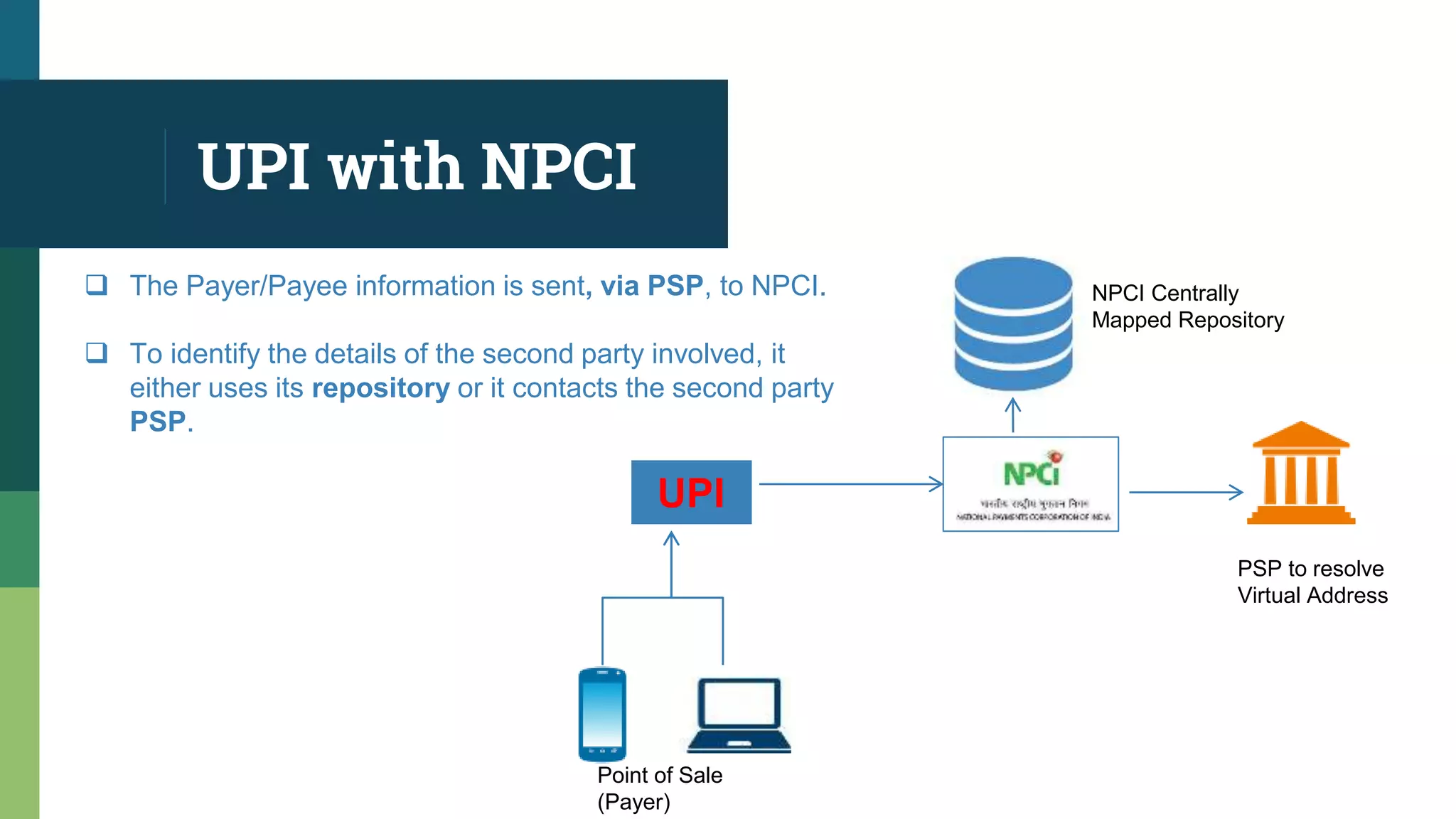

The document discusses the Unified Payments Interface (UPI) system in India. It provides the following key points: - UPI is an instant real-time payment system developed by NPCI that allows money transfers between bank accounts using a virtual payment address. - UPI offers features like being open source, mobile-first, interoperable, instantaneous, secure, cheap, simple, innovative and easily adaptable. - NPCI's central repository maps customers' Aadhaar numbers, mobile numbers and bank accounts to route payments based on these identifiers. - The UPI system uses a virtual payment address architecture to facilitate payments between parties using identifiers like bank account numbers, Aad

Introduction to NPCI and UPI, highlighting NPCI's role in retail payments and UPI's features like open-source and secure payments.

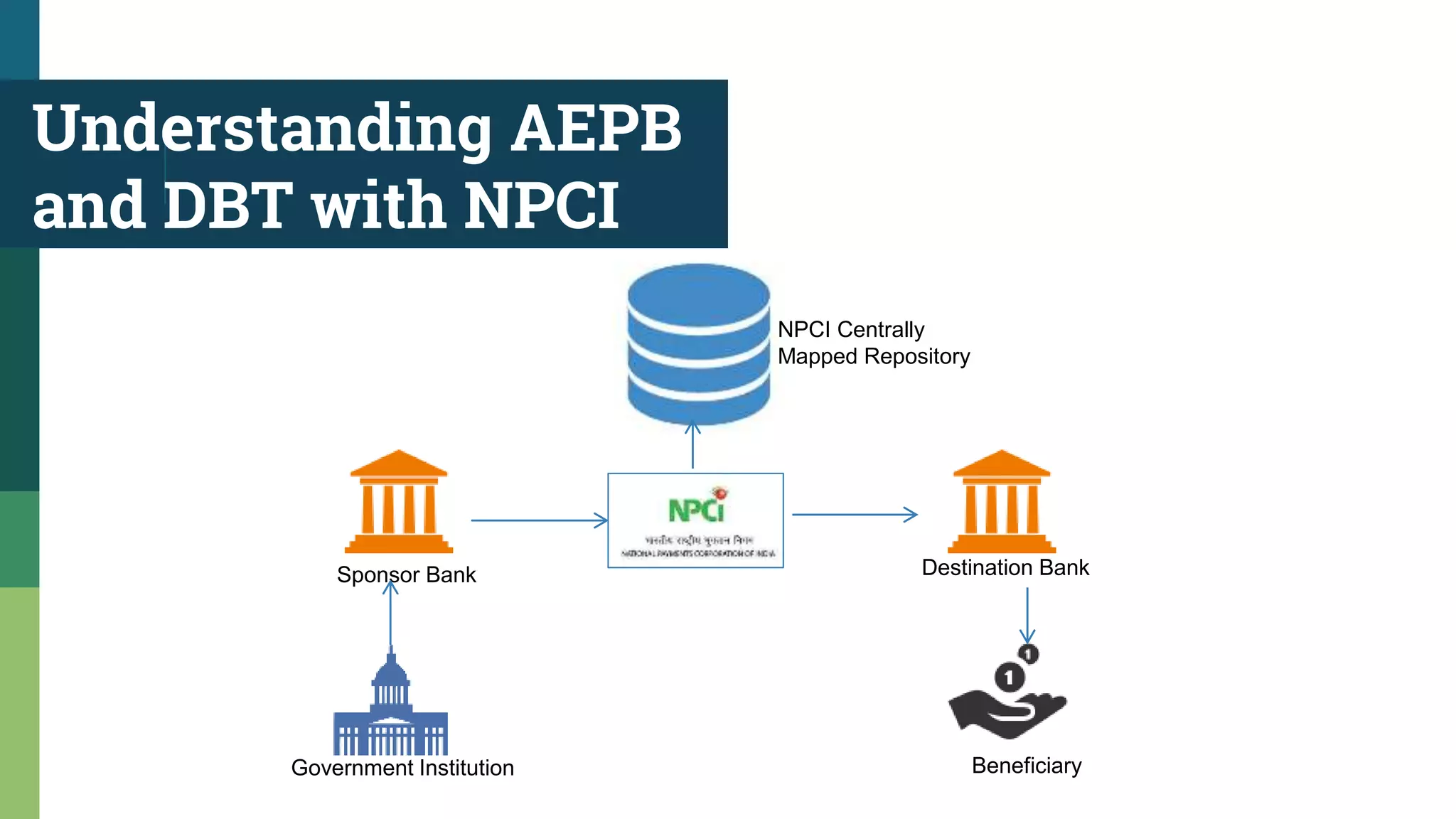

Explanation of AEPB and DBT systems in conjunction with NPCI, including customer identification using Adhaar and mobile numbers.

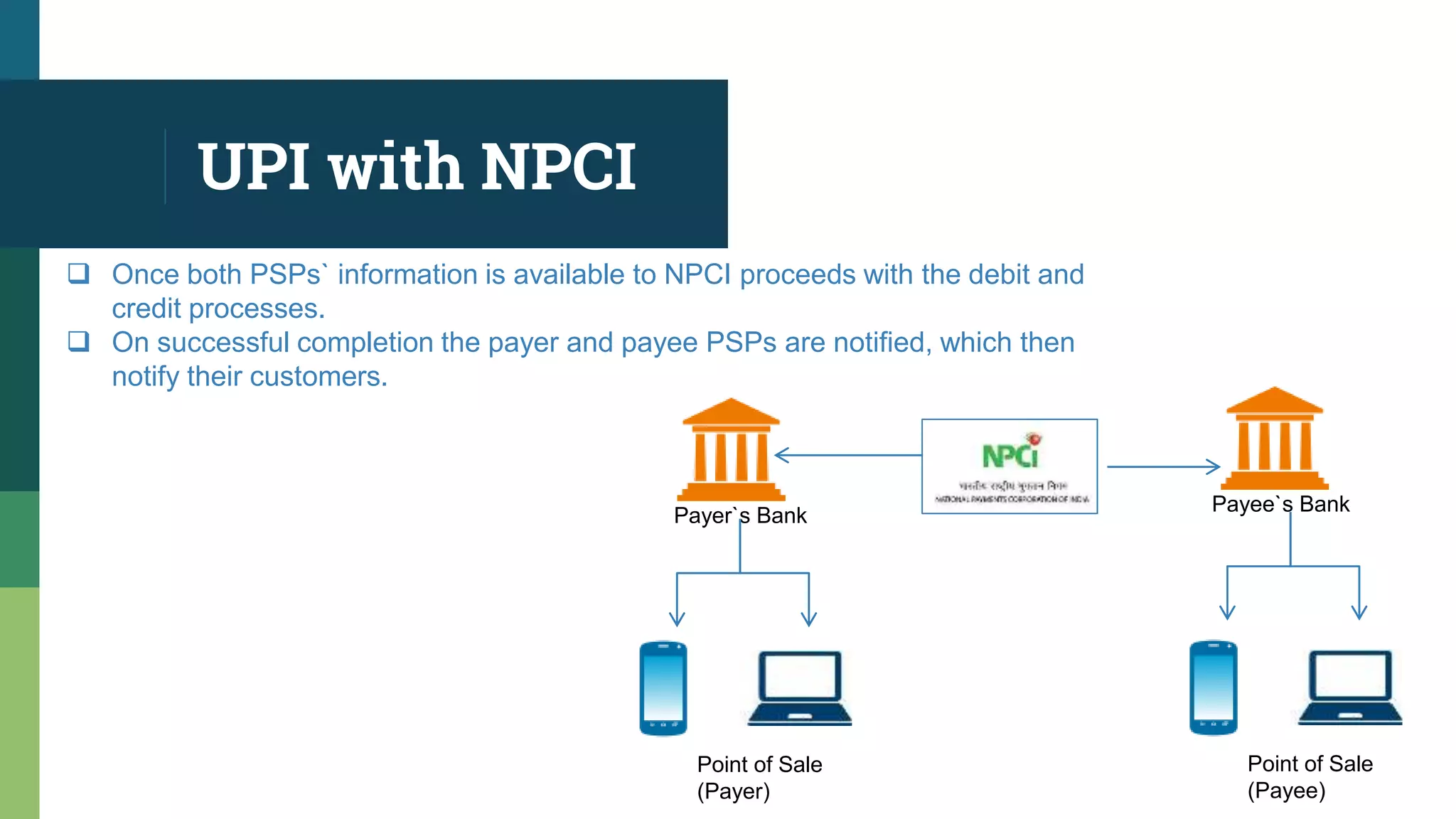

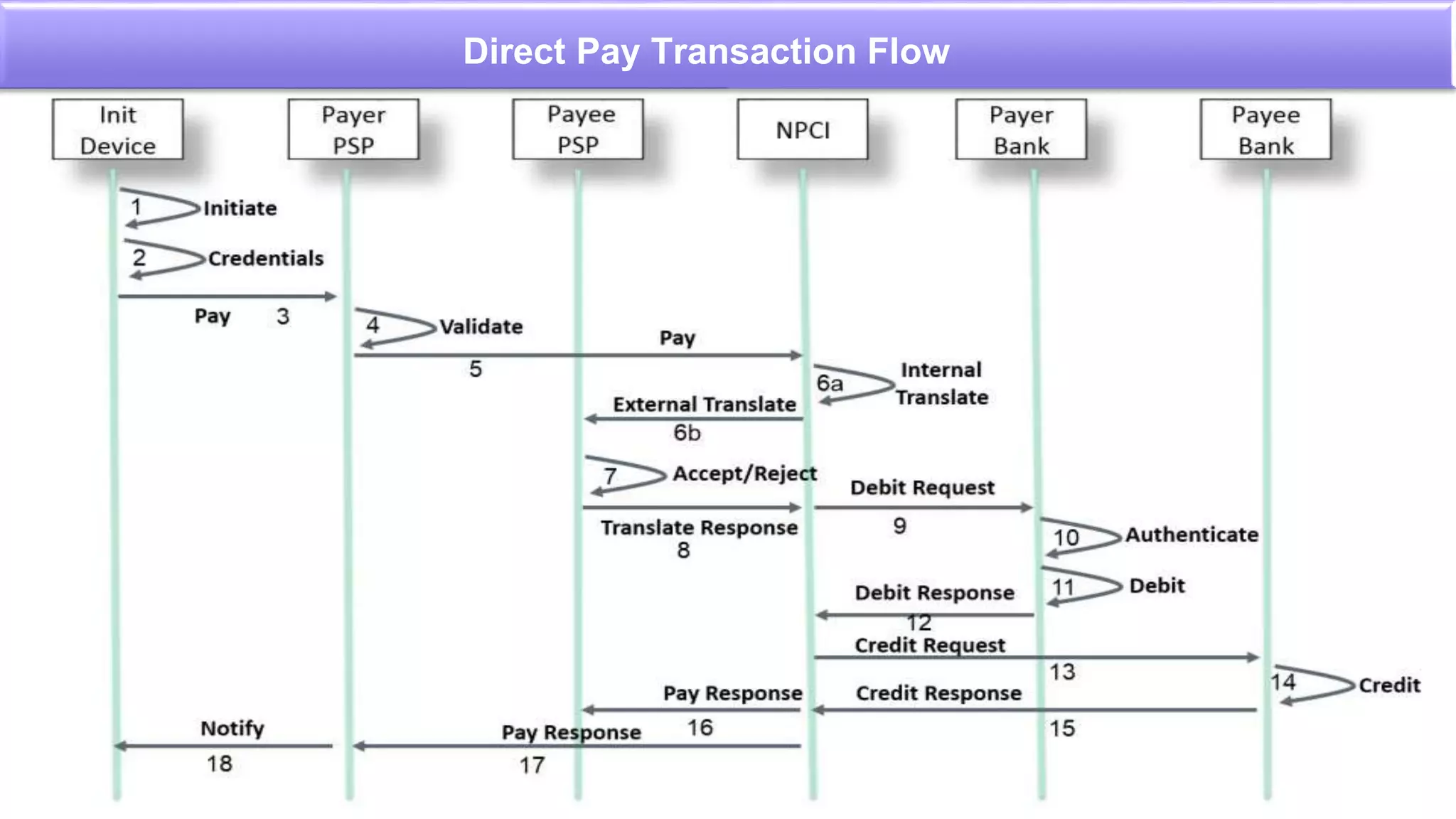

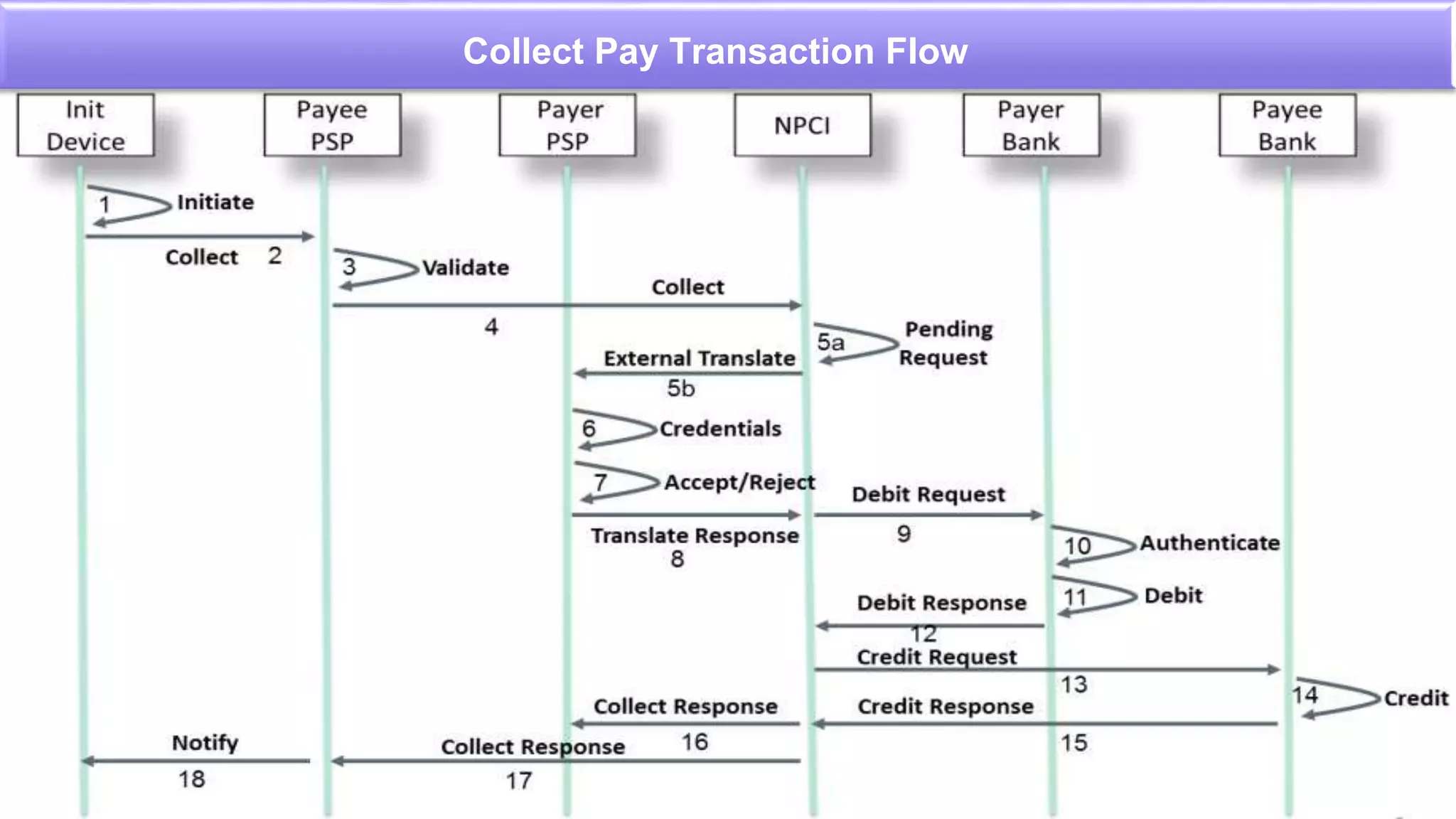

Details on how UPI transactions are processed by NPCI, involving payer and payee banks and transaction notifications.

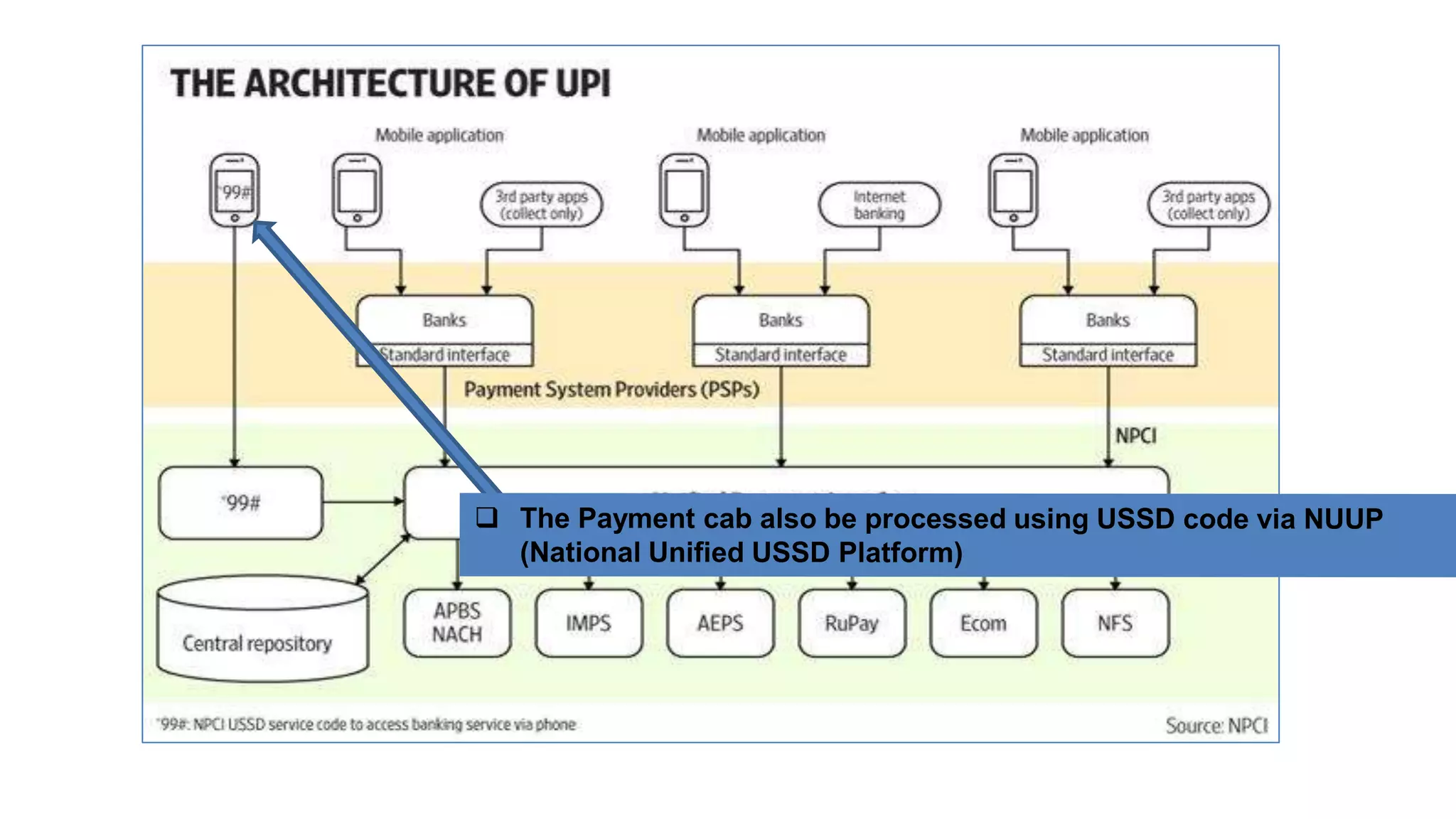

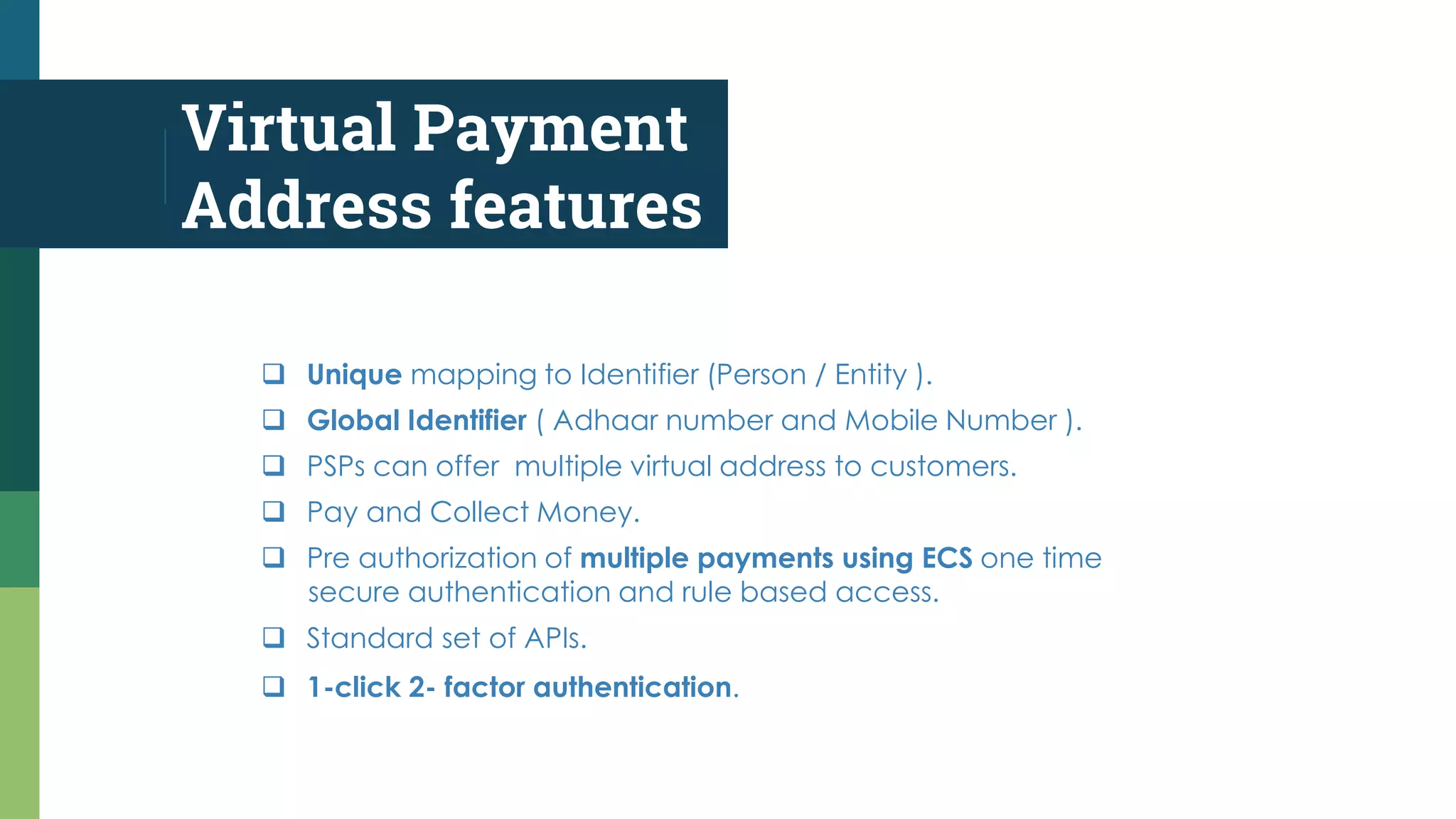

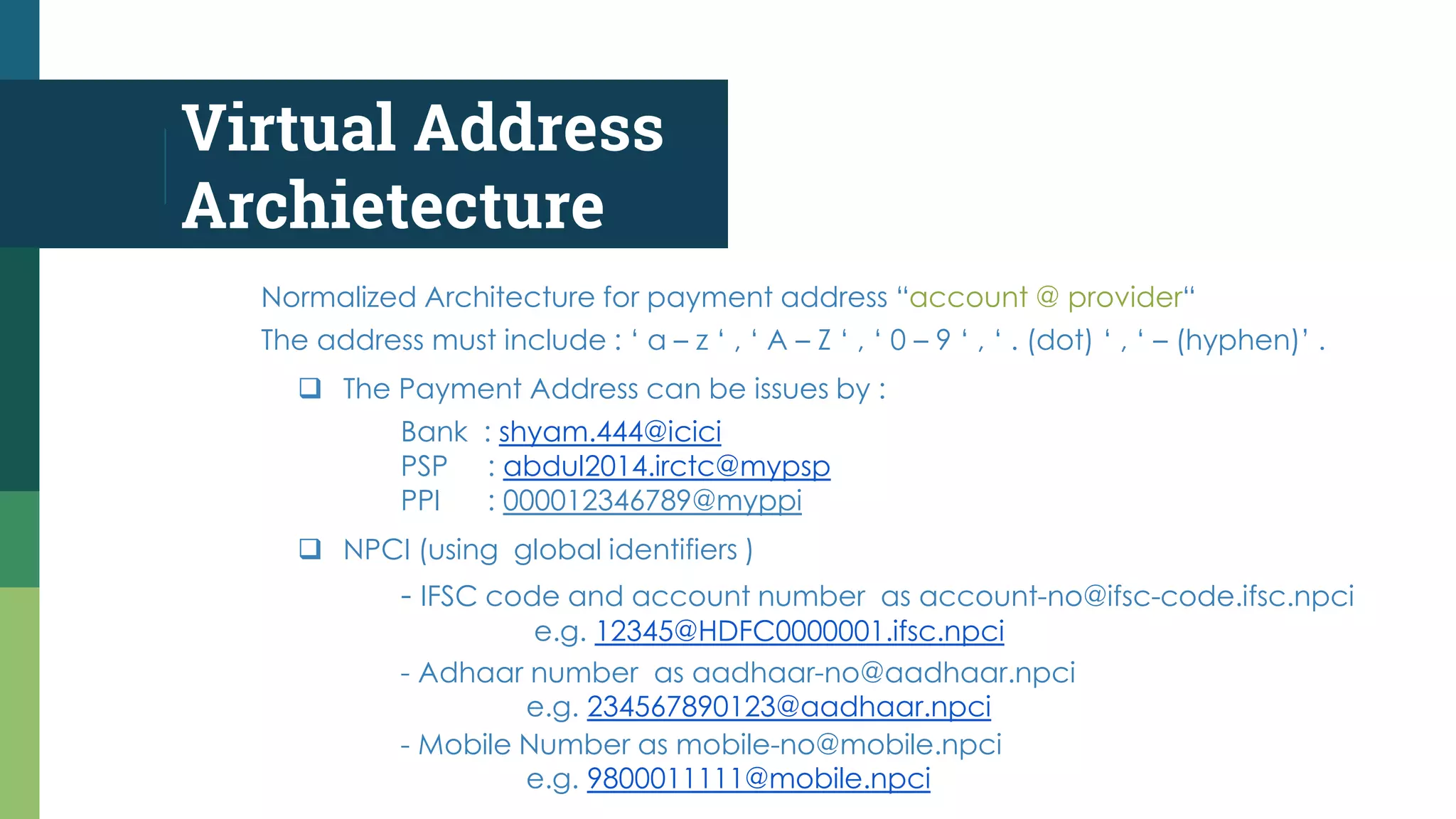

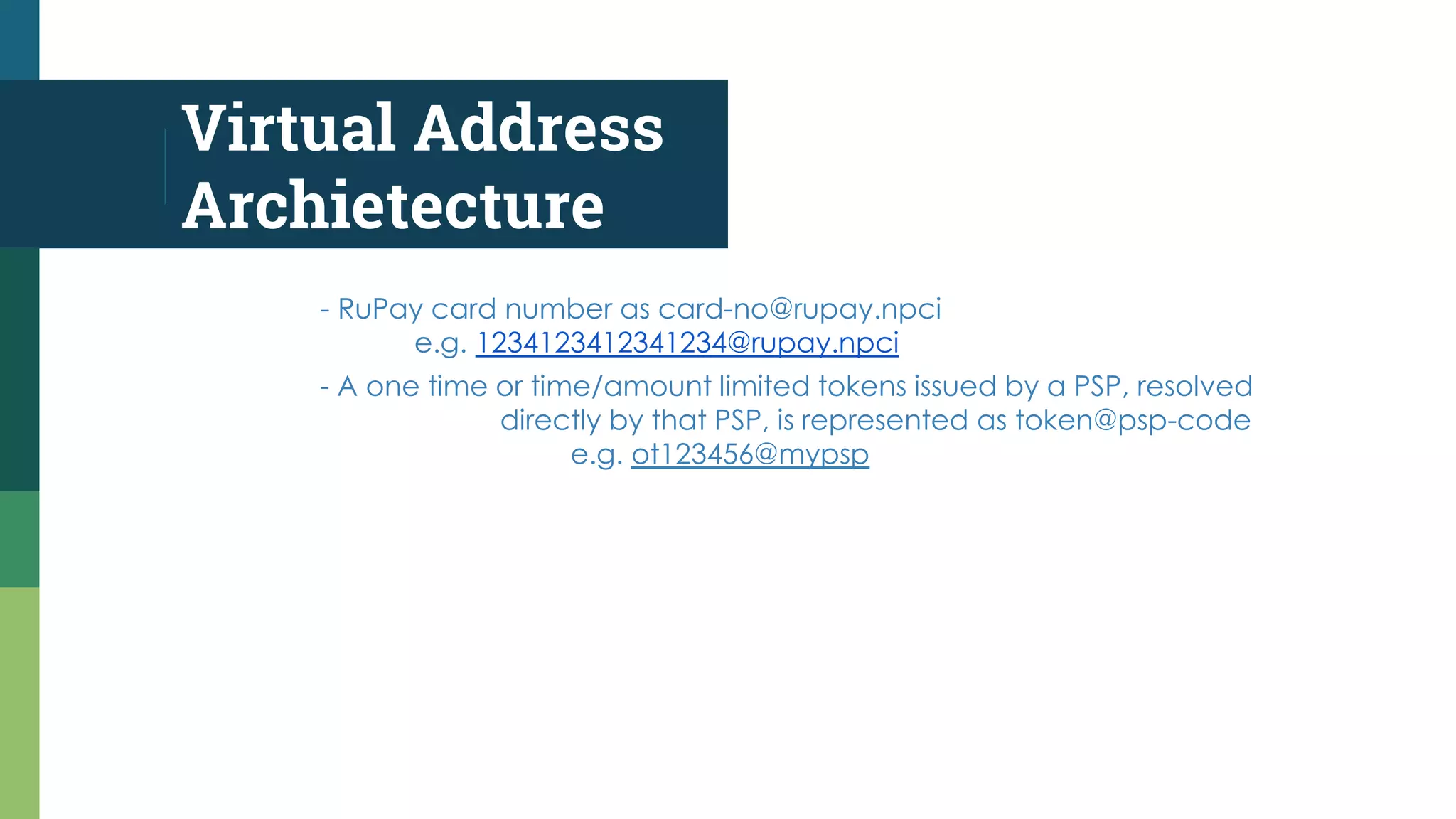

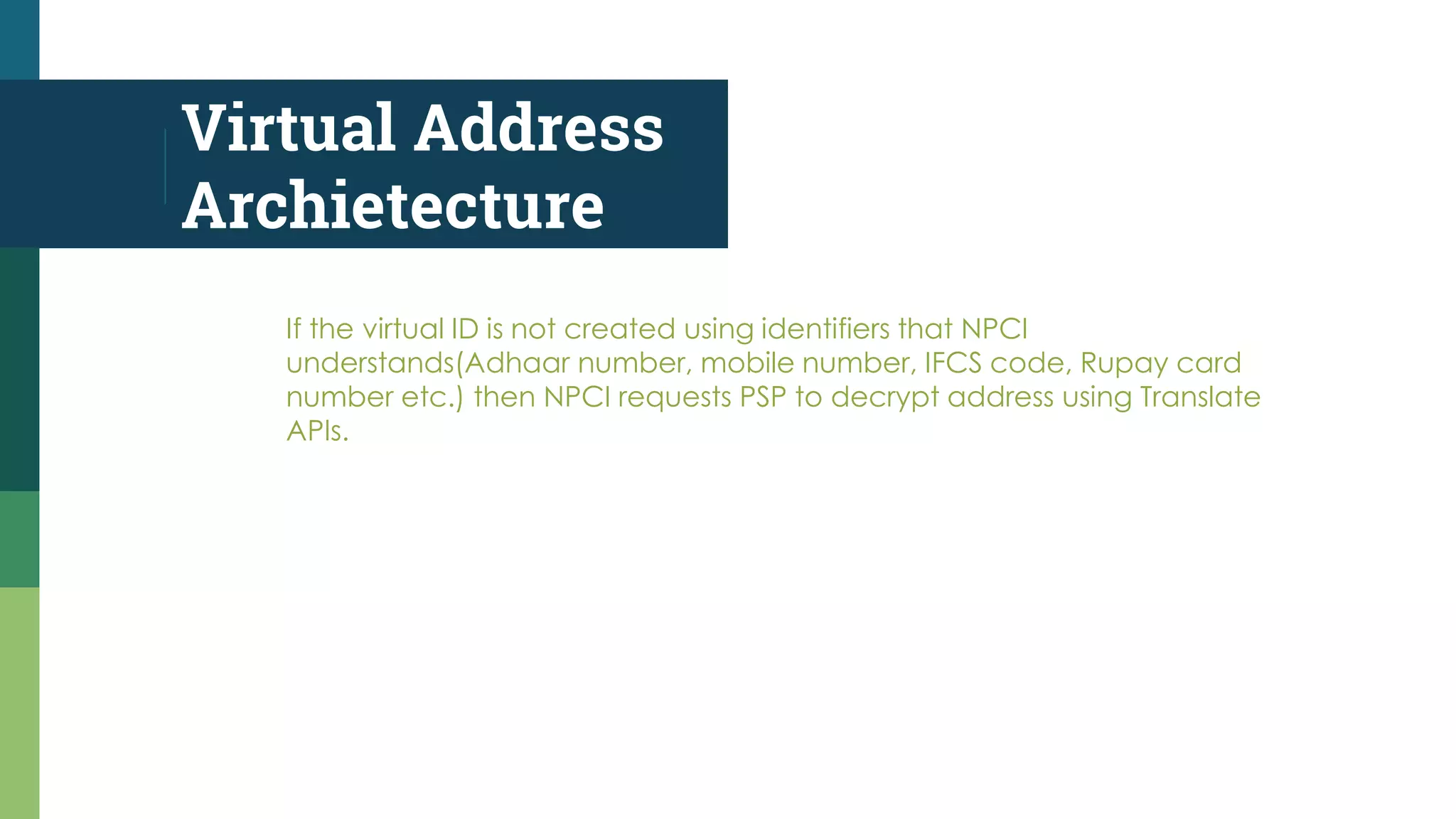

Description of UPI gateway architecture, including virtual payment address structure and mapping identifiers like Adhaar and mobile numbers.

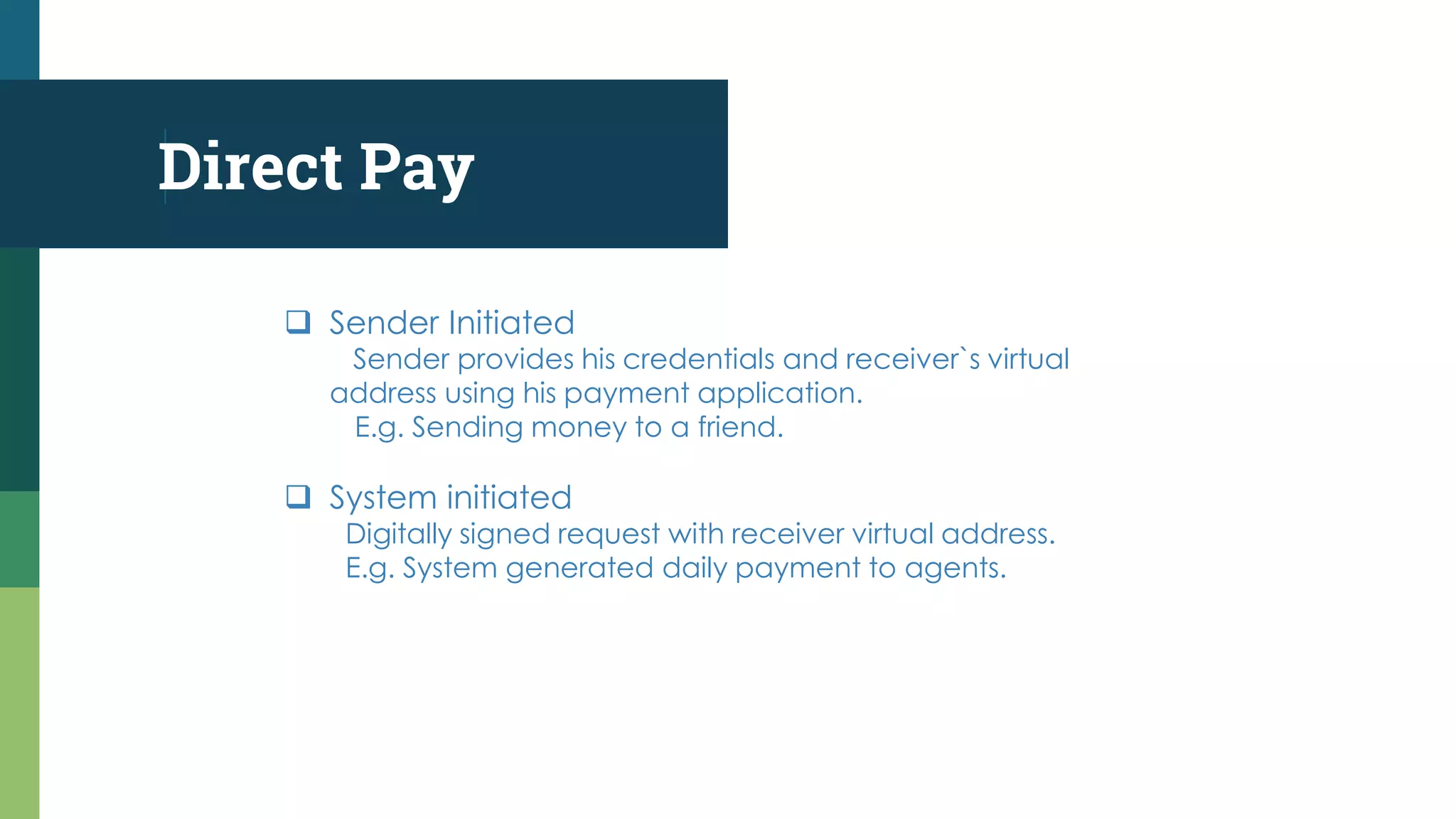

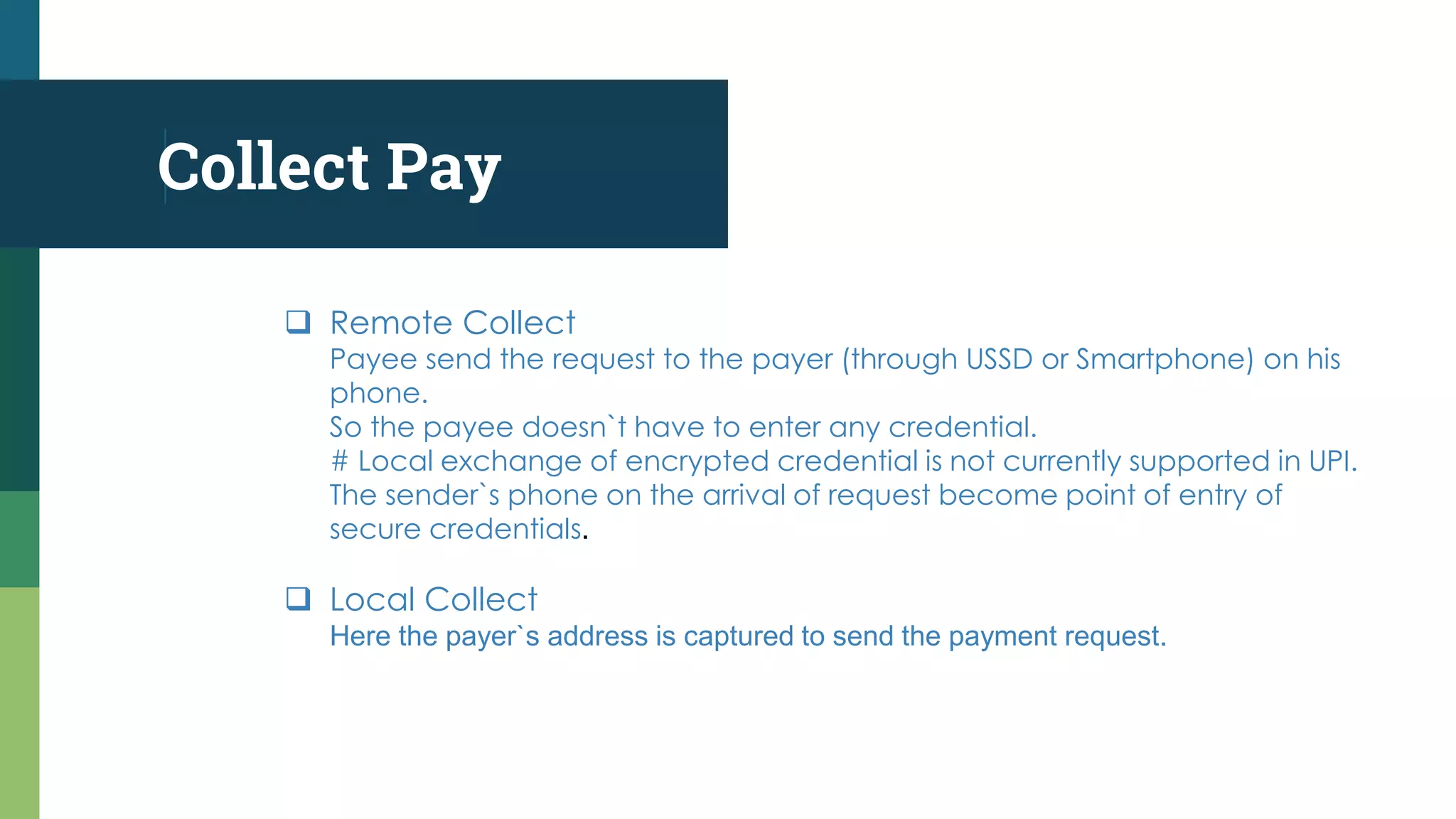

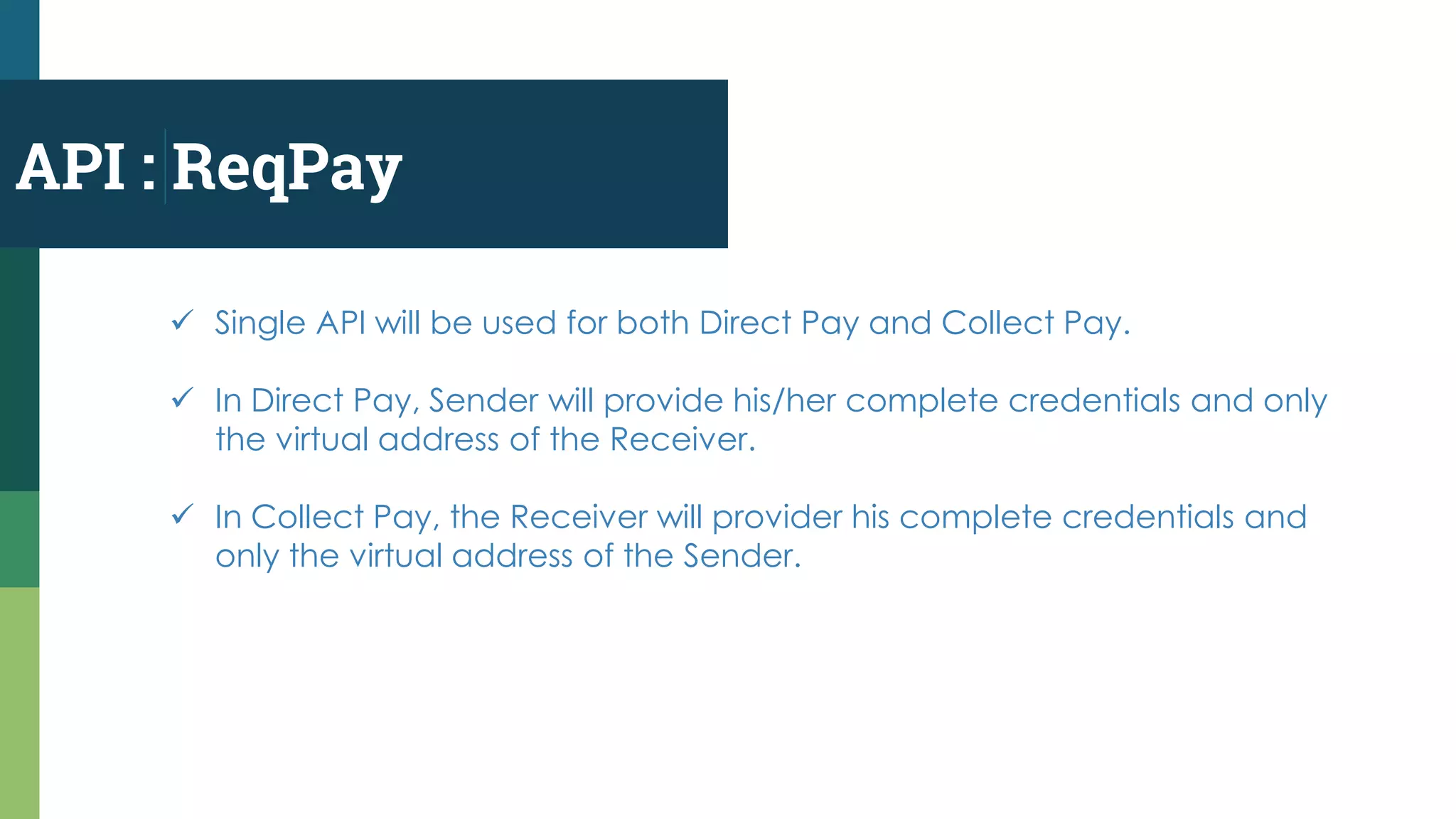

Different types of payment requests in UPI: Direct Pay (sender initiated) and Collect Pay (receiver requested) with transaction flows.

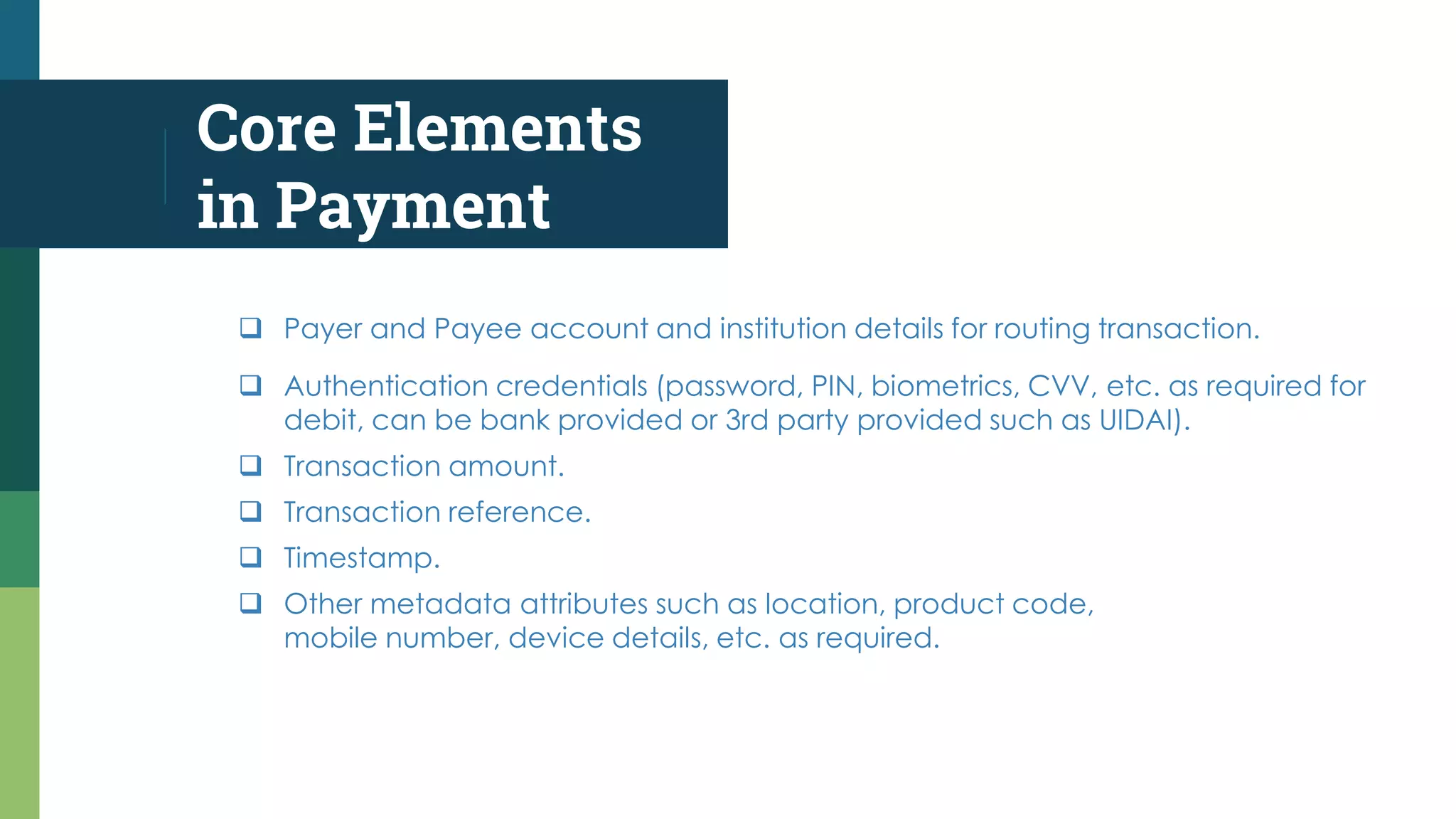

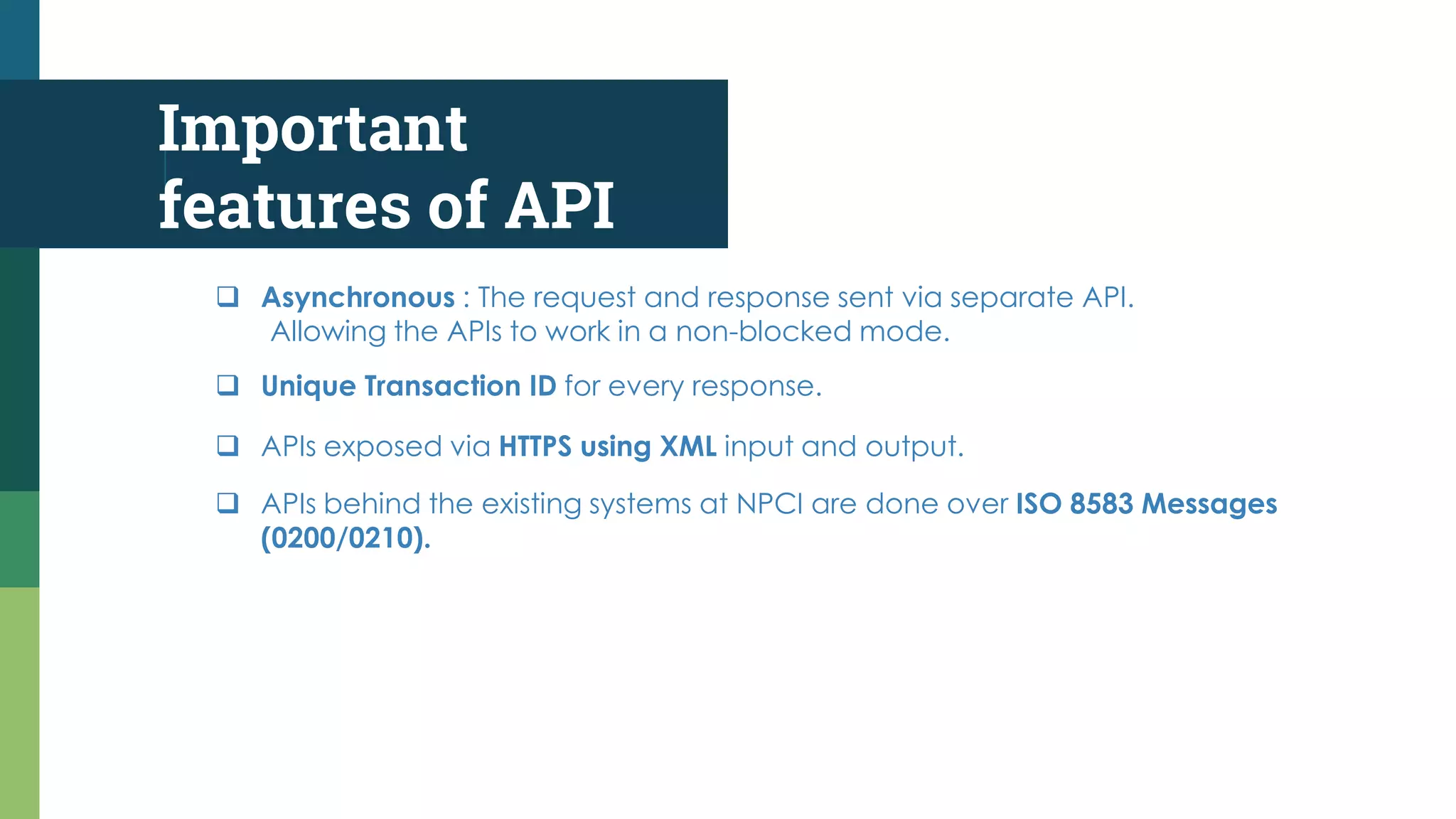

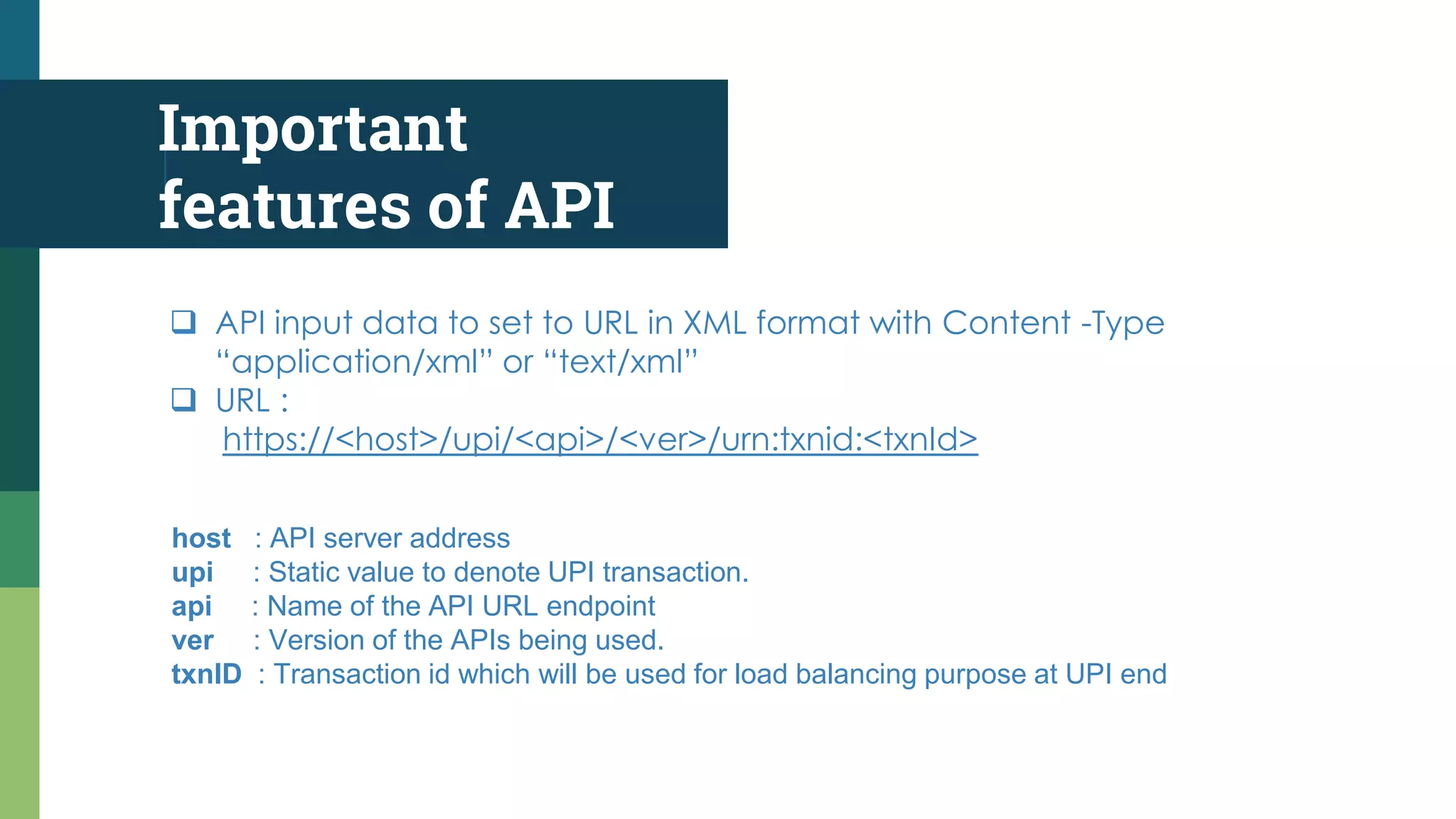

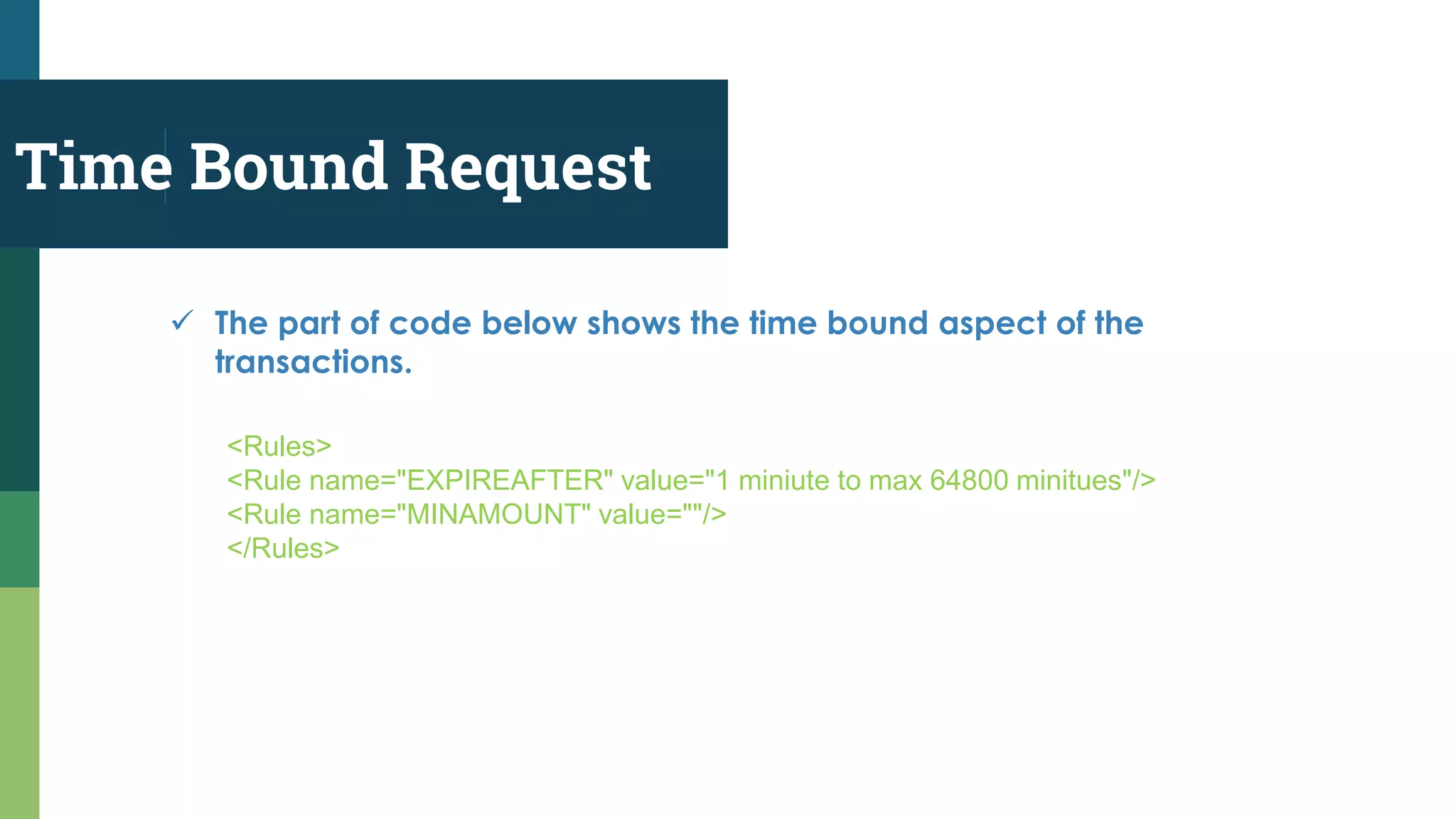

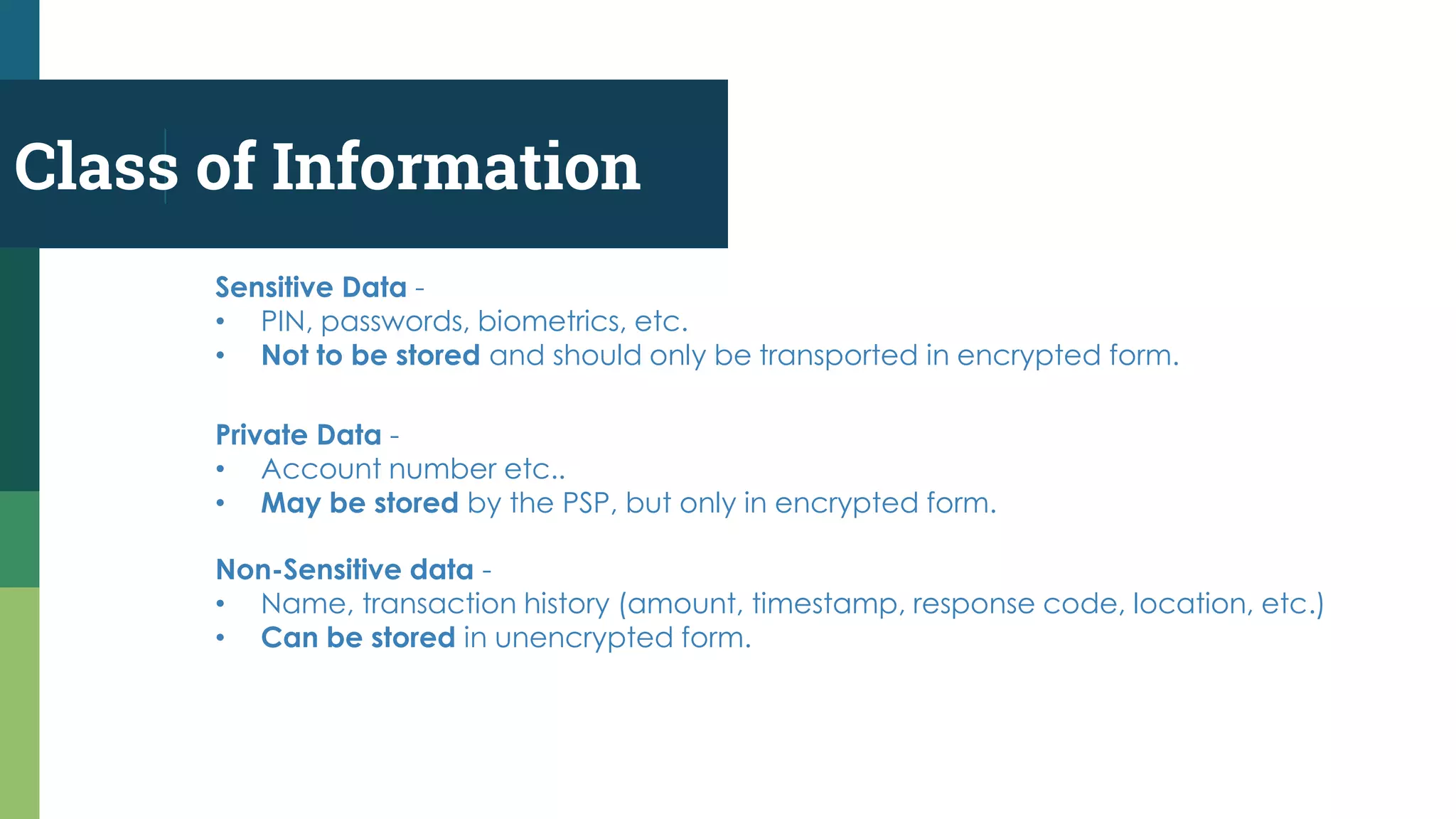

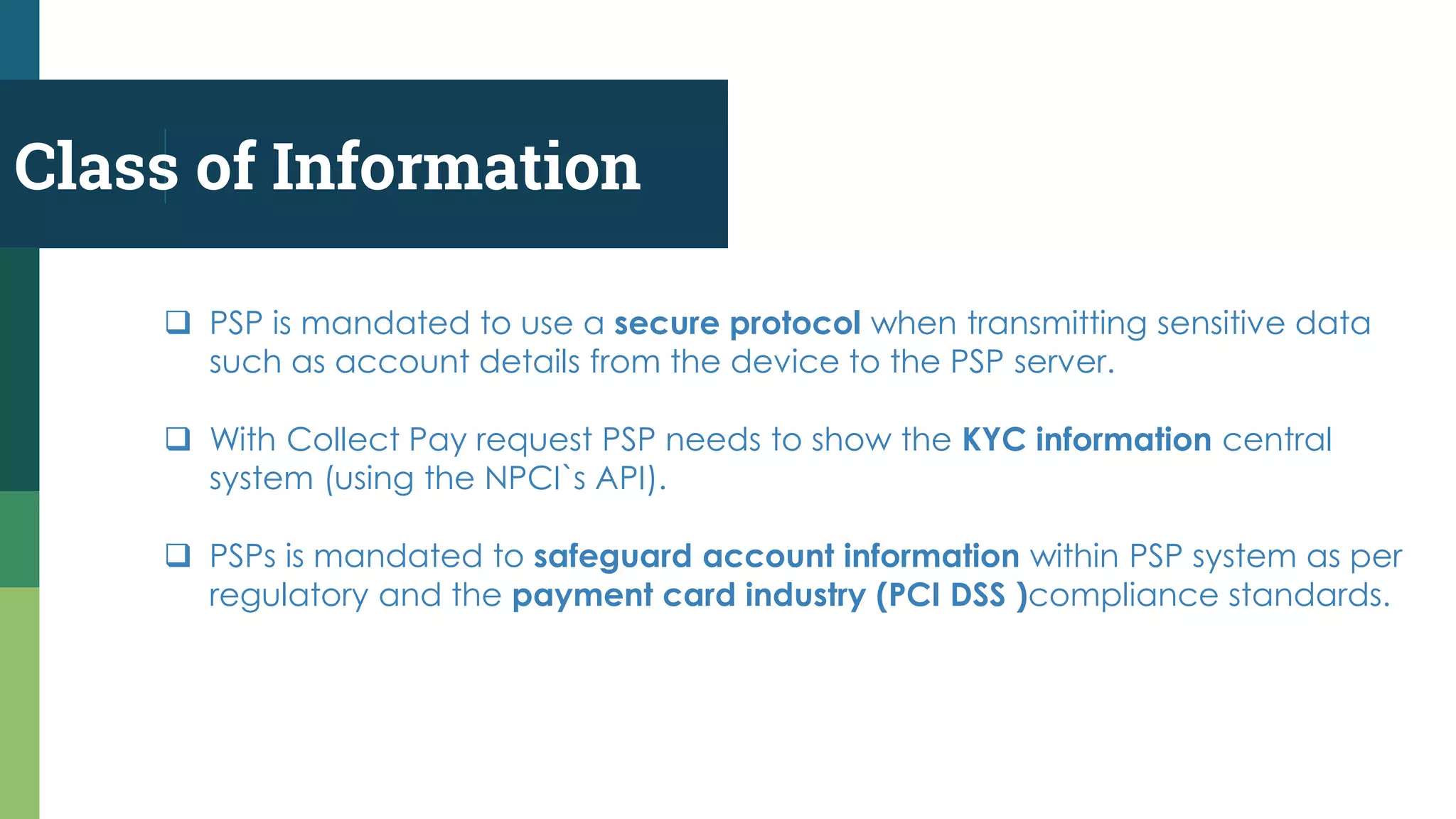

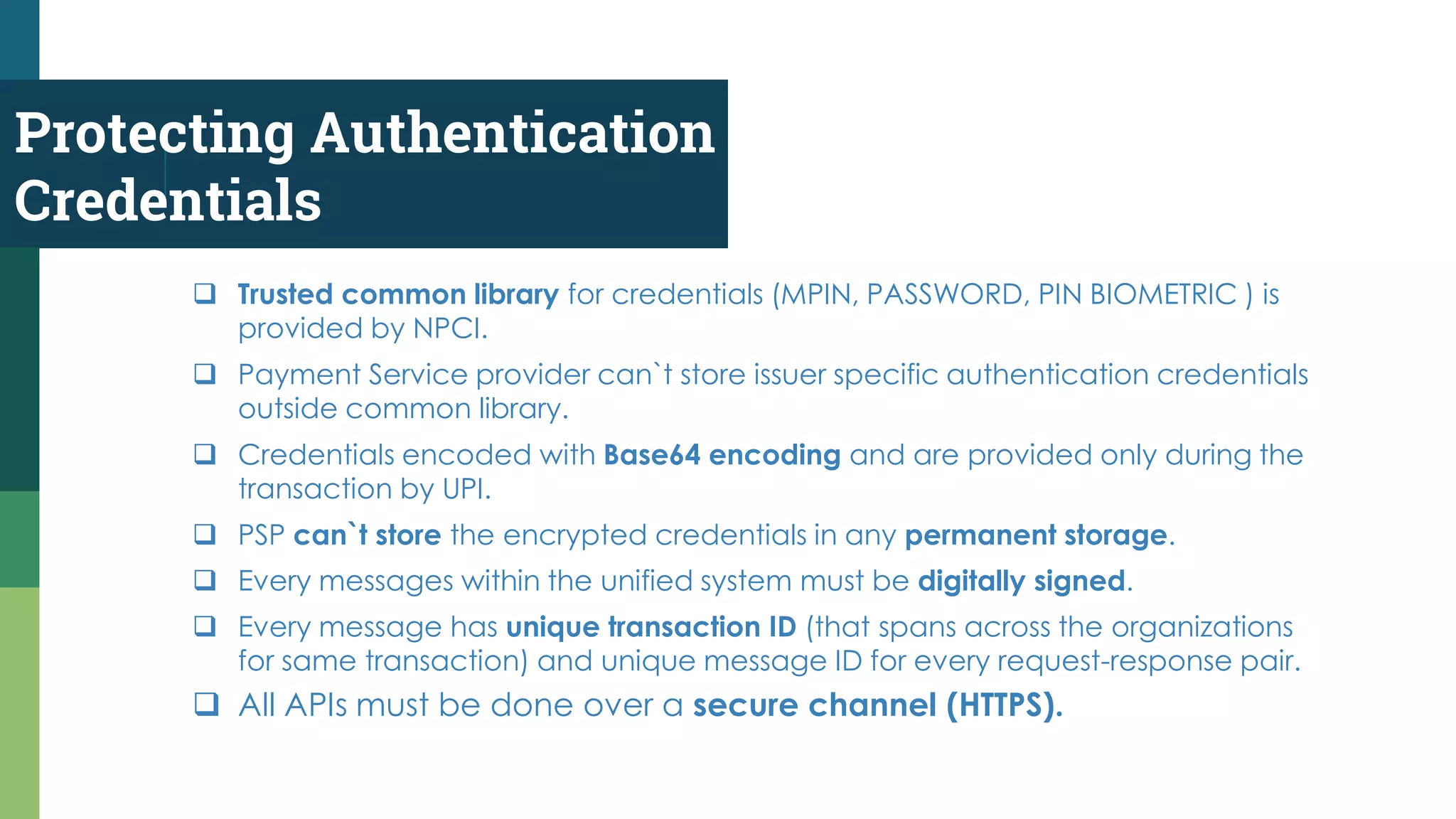

Details on APIs that support UPI transactions, including request and response handling, authentication, and security considerations.Information classification in UPI transactions, addressing sensitive, private data storage, and security protocols for data transmission.

Concludes the presentation, expressing gratitude to the audience.