Downloaded 48 times

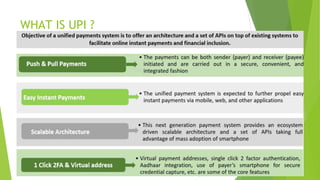

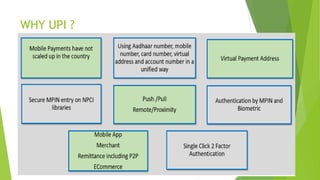

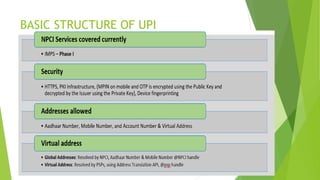

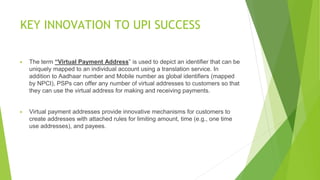

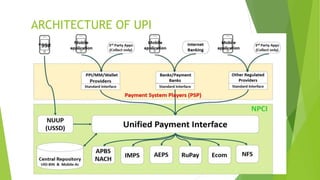

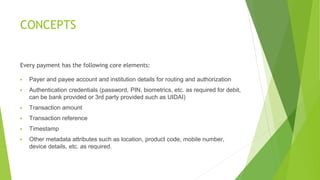

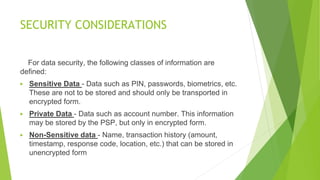

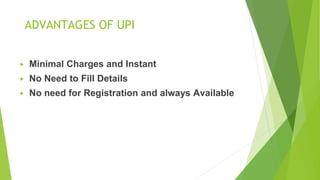

The document outlines the Unified Payment Interface (UPI) as India's advanced payment system, launched to facilitate secure and efficient digital transactions, with a focus on financial inclusion and innovation. Key features include virtual payment addresses, two-factor authentication, and integration with Aadhaar, ensuring security and convenience for users. Despite its advantages, such as instant transfers and minimal charges, UPI faces challenges like transaction limits and the need for internet access and smartphones.