Downloaded 1,192 times

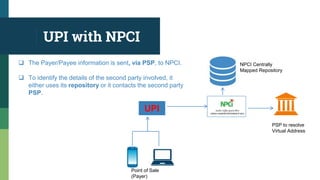

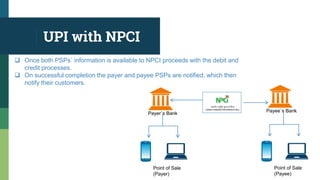

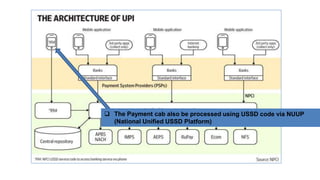

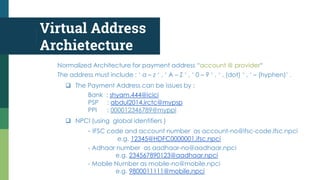

The document discusses the Unified Payments Interface (UPI) system in India. It provides the following key points: - UPI is an instant real-time payment system developed by NPCI that allows money transfers between bank accounts using a virtual payment address. - UPI offers features like being open source, mobile-first, interoperable, instantaneous, secure, cheap, simple, innovative and easily adaptable. - NPCI's central repository maps customers' Aadhaar numbers, mobile numbers and bank accounts to route payments based on these identifiers. - The UPI system uses a virtual payment address architecture to facilitate payments between parties using identifiers like bank account numbers, Aad