CONTENT

1. Introduction

2. Whois Behind UPI?

3. How UPI Works with NPCI?

4. Virtual Payment Address (VPA)

5. Types of Payment Requests

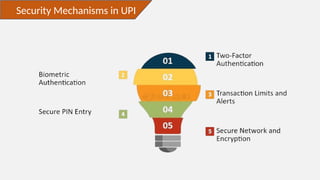

6. Security Mechanisms in UPI

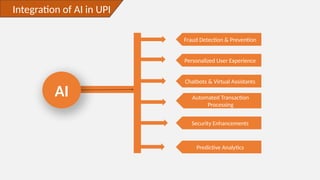

7. Integration of AI in UPI

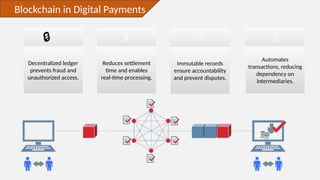

8. Blockchain in Digital Payments

9. Real-time Processing Technologies

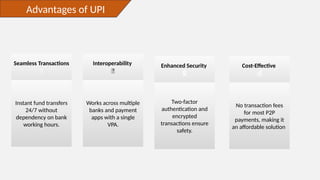

10. Advantages of UPI

11. Future Trends in UPI

12. Conclusion

13. References

3.

INTRODUCTION

- The rapidevolution of digital payments has ensured speed, security, and

interoperability.

- APIs enable seamless communication between banks & payment gateways.

- Integration of AI, blockchain, & cryptographic security.

- Focus on real-time transactions & fraud detection.

UPI is regulated by National Payments Corporation of India(NPCI) which was crated by RBI . It work as

central router for UPI ,it provide the information to bank in encrypted format for the transactions.

4.

Who is BehindUPI?

NPCI (National Payments Corporation Of India).

Umbrella organization for all retail payment systems.

Set up by RBI and IBA in April 2009.

Launched the IMPS.

Launched the RuPay card.

Currently launched UPI.

Virtual Payment Address(VPA)

A unique identifier

used in UPI

transactions.

VPA

Eliminates the

need to share

bank account

details.

Secure and

convenient for

digital payments.

Used for sending and

receiving money

instantly.

Integration of AIin UPI

AI

Fraud Detection & Prevention

Personalized User Experience

Chatbots & Virtual Assistants

Automated Transaction

Processing

Security Enhancements

Predictive Analytics

10.

Blockchain in DigitalPayments

Decentralized ledger

prevents fraud and

unauthorized access.

⚡

Reduces settlement

time and enables

real-time processing.

🏦

Immutable records

ensure accountability

and prevent disputes.

🤖

Automates

transactions, reducing

dependency on

intermediaries.

🔒

11.

Real-time Processing Technologies

MoreAccuracy & timely

Real time processing

keeps you sync all the

time

Deadlines are always

met with real time

processing

Realtime Processing is

Quite Reactive

Real time processing

involves multitasking

Real time processing

works independently

Real time

processing

12.

Advantages of UPI

SeamlessTransactions

🚀

Instant fund transfers

24/7 without

dependency on bank

working hours.

Interoperability

🔄

Works across multiple

banks and payment

apps with a single

VPA.

Enhanced Security

🔒

Two-factor

authentication and

encrypted

transactions ensure

safety.

Cost-Effective

💰

No transaction fees

for most P2P

payments, making it

an affordable solution.

Conclusion

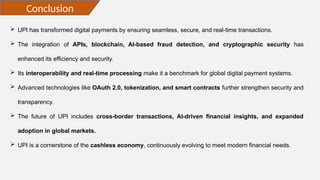

UPI hastransformed digital payments by ensuring seamless, secure, and real-time transactions.

The integration of APIs, blockchain, AI-based fraud detection, and cryptographic security has

enhanced its efficiency and security.

Its interoperability and real-time processing make it a benchmark for global digital payment systems.

Advanced technologies like OAuth 2.0, tokenization, and smart contracts further strengthen security and

transparency.

The future of UPI includes cross-border transactions, AI-driven financial insights, and expanded

adoption in global markets.

UPI is a cornerstone of the cashless economy, continuously evolving to meet modern financial needs.

15.

References

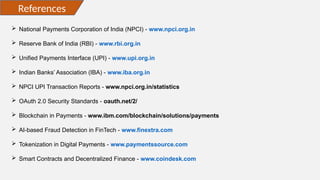

National PaymentsCorporation of India (NPCI) - www.npci.org.in

Reserve Bank of India (RBI) - www.rbi.org.in

Unified Payments Interface (UPI) - www.upi.org.in

Indian Banks’ Association (IBA) - www.iba.org.in

NPCI UPI Transaction Reports - www.npci.org.in/statistics

OAuth 2.0 Security Standards - oauth.net/2/

Blockchain in Payments - www.ibm.com/blockchain/solutions/payments

AI-based Fraud Detection in FinTech - www.finextra.com

Tokenization in Digital Payments - www.paymentssource.com

Smart Contracts and Decentralized Finance - www.coindesk.com