1) Working capital refers to the capital required to finance short-term operating expenses like inventory, accounts receivable, and cash. It revolves quickly as assets are sold and replaced with new current assets.

2) There are different types of working capital classified by basis - gross working capital refers to total current assets while net working capital is current assets minus current liabilities. Working capital is also classified as permanent/fixed or temporary/variable.

3) Permanent working capital is needed continuously to operate the business while temporary working capital fluctuates to meet seasonal or specific needs like launches or strikes. Maintaining adequate working capital is important for business operations and liquidity.

In this document

Powered by AI

Introduction to Working Capital highlighting its significance for short-term asset financing.

Classification of Working Capital based on concepts (Gross and Net) and time (Permanent and Temporary).

Definition and importance of Gross Working Capital focusing on investment in current assets.

Explains Net Working Capital, its calculation, and significance in financial management.

Differences between Net and Gross Working Capital focusing on qualitative vs quantitative aspects.

Definition and characteristics of Permanent Working Capital essential for ongoing business activities.

Definition and characteristics of Temporary Working Capital, highlighting its fluctuating nature.

Definition of Seasonal Working Capital with examples of businesses requiring extra funds in certain seasons.

Definition of Specific Working Capital needed for unforeseen contingencies and special projects.

WORKING CAPITAL

Working Capital refers to that part of the firm’s

capital, which is required for financing short-term or

current assets such as cash marketable securities, debtors

and inventories. Funds thus, invested in current assets

keep revolving fast and are constantly converted into cash

and this cash flow out again in exchange for other current

assets. Working Capital is also known as revolving or

circulating capital or short-term capital.

3.

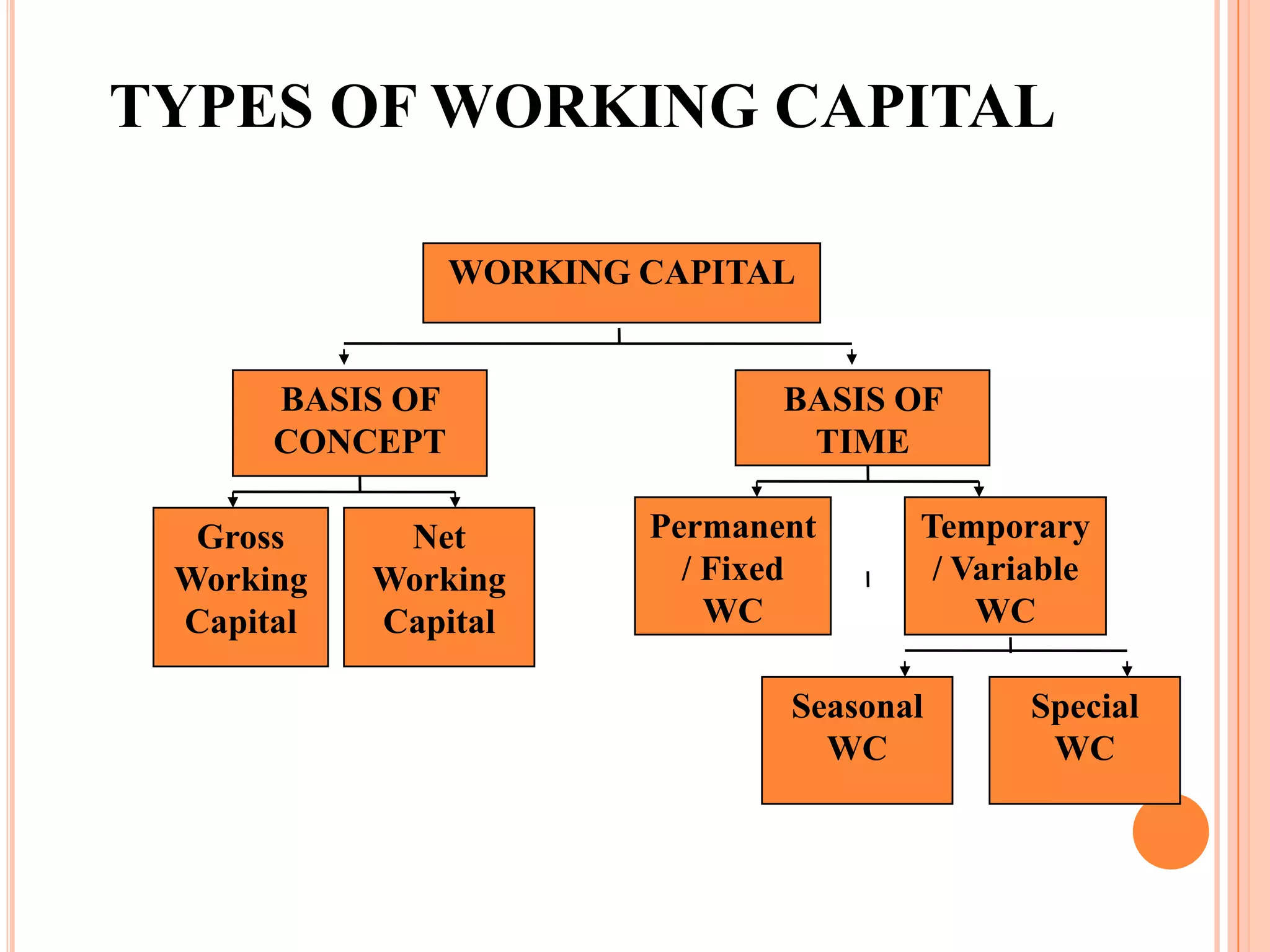

TYPES OF WORKINGCAPITAL

WORKING CAPITAL

BASIS OF BASIS OF

CONCEPT TIME

Gross Net Permanent Temporary

Working Working / Fixed / Variable

Capital Capital WC WC

Seasonal Special

WC WC

4.

GROSS WORKING CAPITAL

Gross working capital require that a firm have

adequate investment in current assets and proper

management of theses asset.

It should be neither excessive nor inadequate asset.

If there are surplus funds they should be immediately

invested, and if the funds become low and the

requirement is greater the financial manager should be

able to get the required finance so that the commitments of

the firm can be made short notice.

5.

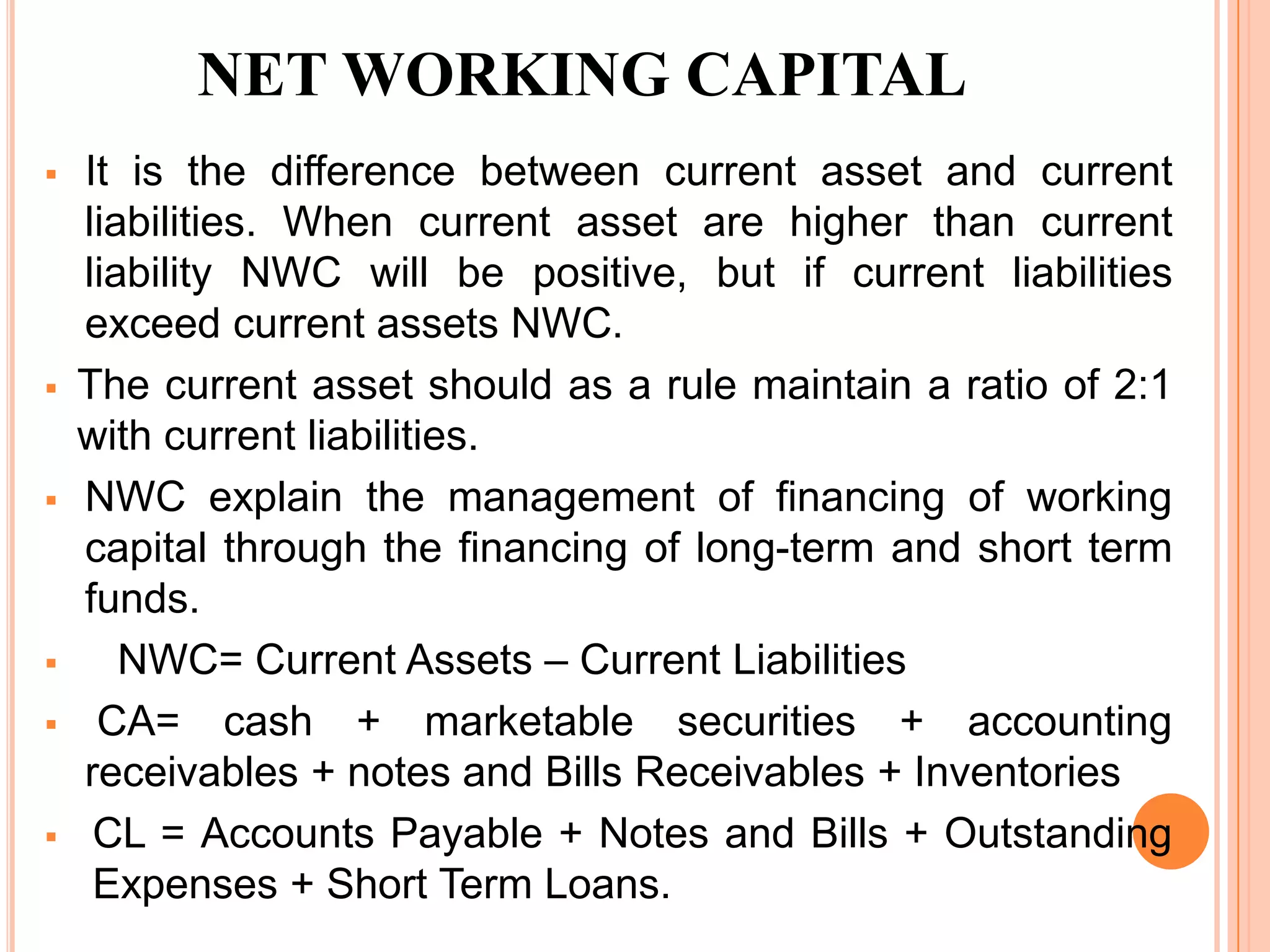

NET WORKING CAPITAL

It is the difference between current asset and current

liabilities. When current asset are higher than current

liability NWC will be positive, but if current liabilities

exceed current assets NWC.

The current asset should as a rule maintain a ratio of 2:1

with current liabilities.

NWC explain the management of financing of working

capital through the financing of long-term and short term

funds.

NWC= Current Assets – Current Liabilities

CA= cash + marketable securities + accounting

receivables + notes and Bills Receivables + Inventories

CL = Accounts Payable + Notes and Bills + Outstanding

Expenses + Short Term Loans.

6.

DIFFERENCE BETWEEN NETWORKING

CAPITAL AND GROSS WORKING CAPITAL

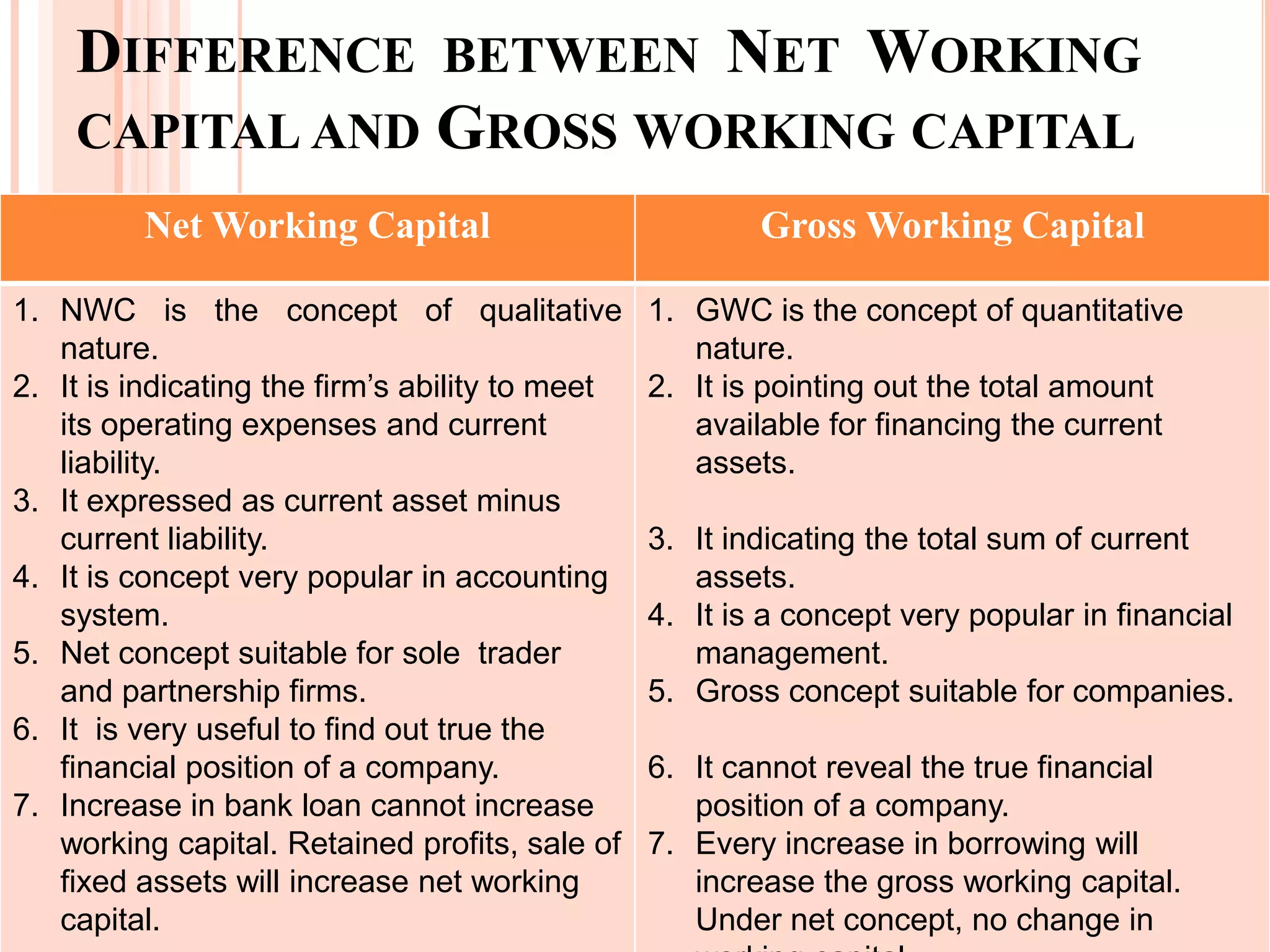

Net Working Capital Gross Working Capital

1. NWC is the concept of qualitative 1. GWC is the concept of quantitative

nature. nature.

2. It is indicating the firm’s ability to meet 2. It is pointing out the total amount

its operating expenses and current available for financing the current

liability. assets.

3. It expressed as current asset minus

current liability. 3. It indicating the total sum of current

4. It is concept very popular in accounting assets.

system. 4. It is a concept very popular in financial

5. Net concept suitable for sole trader management.

and partnership firms. 5. Gross concept suitable for companies.

6. It is very useful to find out true the

financial position of a company. 6. It cannot reveal the true financial

7. Increase in bank loan cannot increase position of a company.

working capital. Retained profits, sale of 7. Every increase in borrowing will

fixed assets will increase net working increase the gross working capital.

capital. Under net concept, no change in

7.

PERMANENT OR REGULAR

WORKING CAPITAL

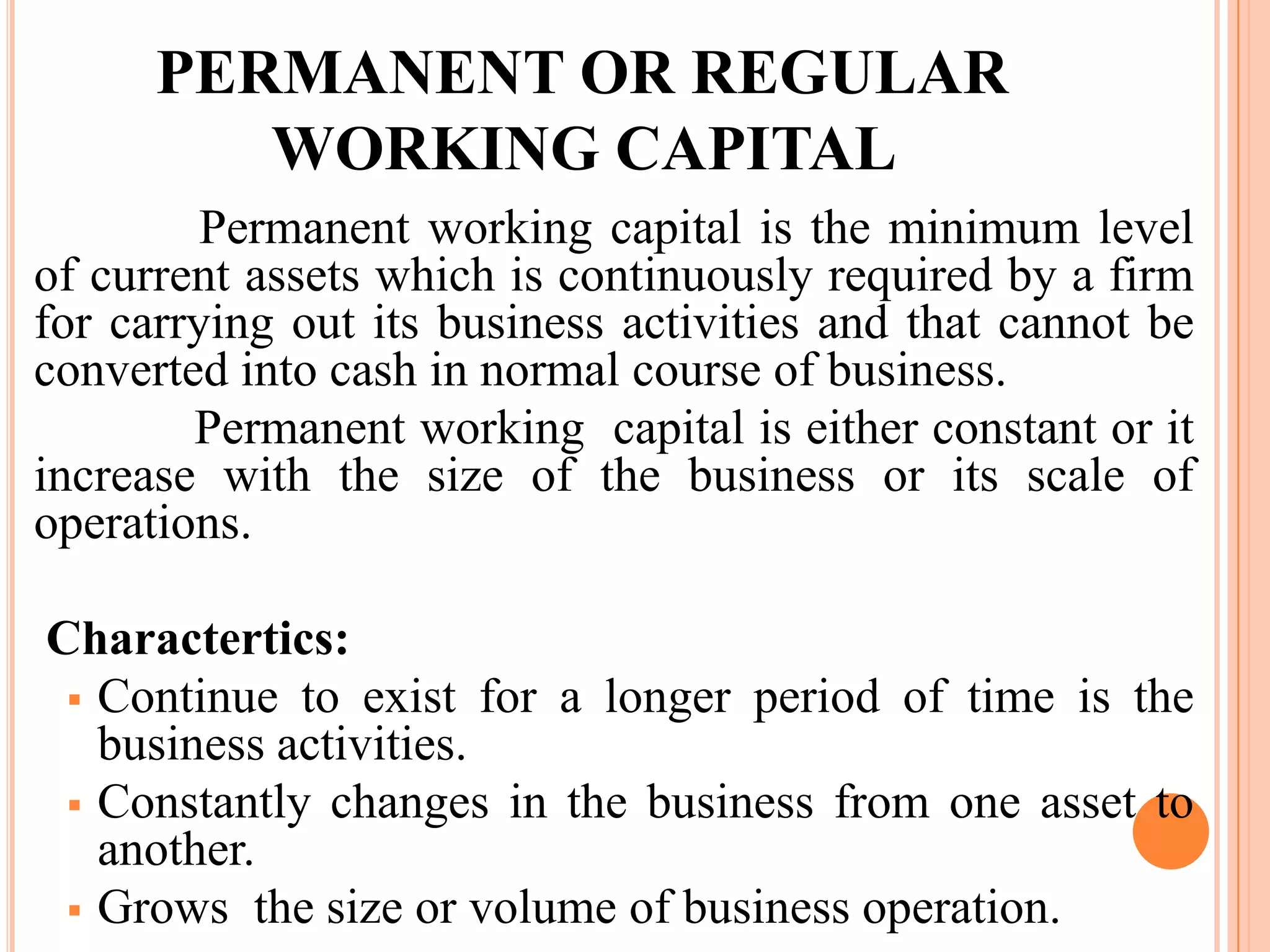

Permanent working capital is the minimum level

of current assets which is continuously required by a firm

for carrying out its business activities and that cannot be

converted into cash in normal course of business.

Permanent working capital is either constant or it

increase with the size of the business or its scale of

operations.

Charactertics:

Continue to exist for a longer period of time is the

business activities.

Constantly changes in the business from one asset to

another.

Grows the size or volume of business operation.

8.

TEMPORARY OR VARIABLE

WORKING CAPITAL

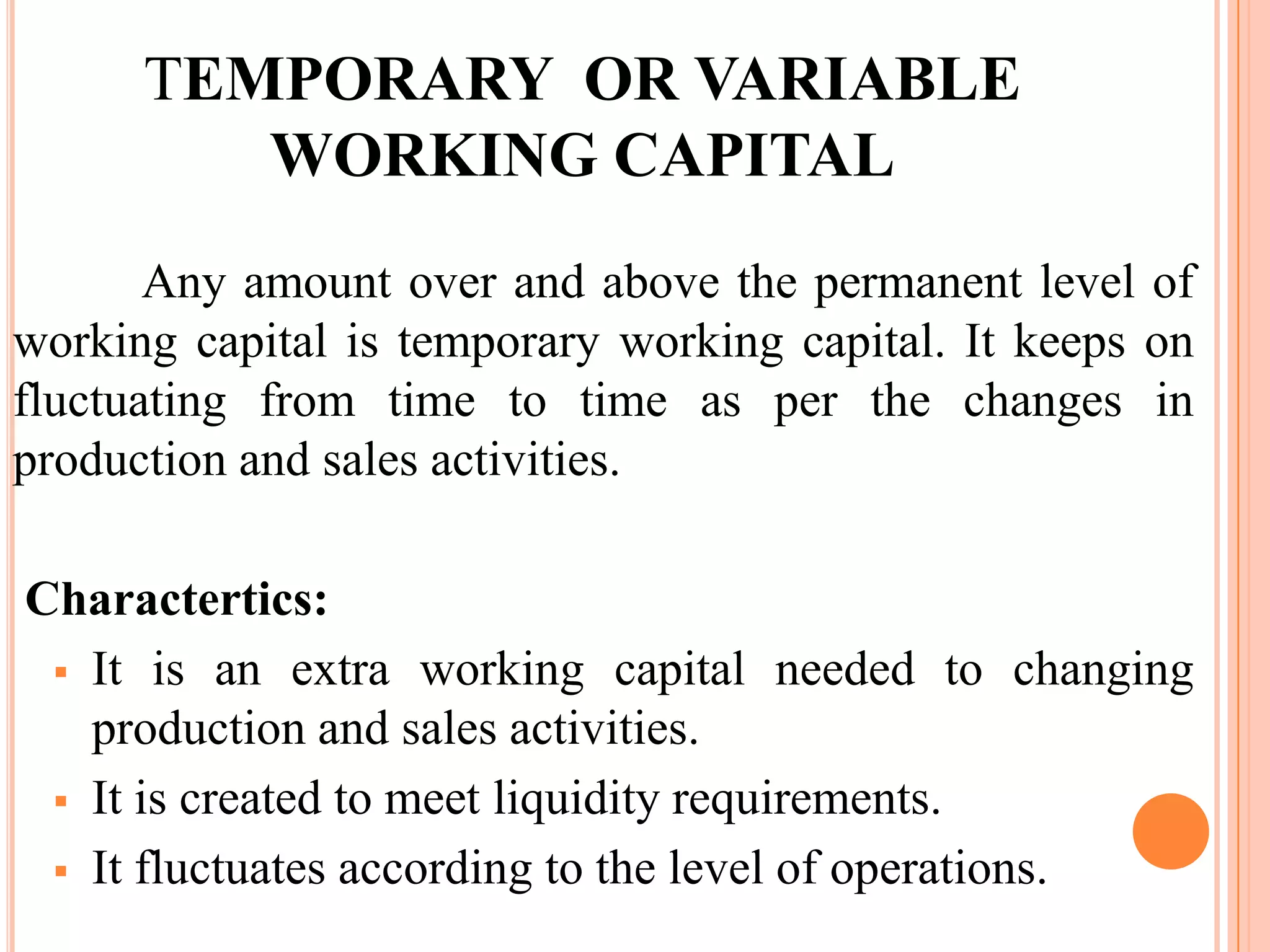

Any amount over and above the permanent level of

working capital is temporary working capital. It keeps on

fluctuating from time to time as per the changes in

production and sales activities.

Charactertics:

It is an extra working capital needed to changing

production and sales activities.

It is created to meet liquidity requirements.

It fluctuates according to the level of operations.

9.

Temporary working capital is fluctuating during the

operating period.

It is needed for shorter period.

Two types of temporary working capital

• Seasonal working capital.

• Specific working capital.

10.

SEASONAL WORKING CAPITAL

The capital required to meet the seasonal

demands of the enterprise is called seasonal working

capital.

For example, a manufacture of woolen textiles,

refrigerators or coolers may need extra funds to carry on

production and to accumulate stock before the sales

operations.

Seasonal working capital being of short-term

nature, it has to be financed from short-term sources like

bank loan etc.

11.

SPECIFIC WORKING CAPITAL

Specific working capital is that part of working

capital which is required to meet unforeseen contingencies

like slump, strike, flood, war etc.

Additional working capital is to be arranged to

meet special exigencies such as launching of extensive

marketing campaign, purchase of goods for stock in view

of future increase in price etc.