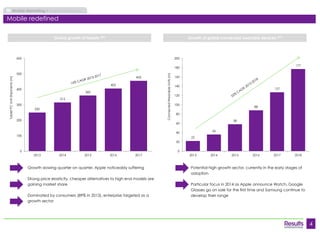

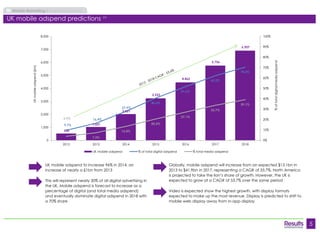

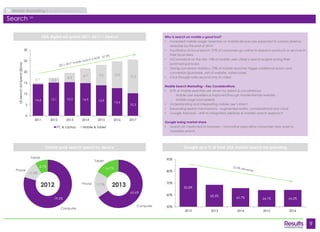

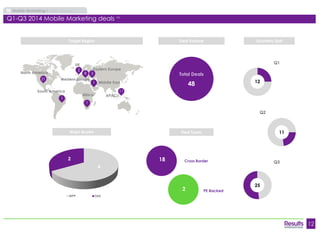

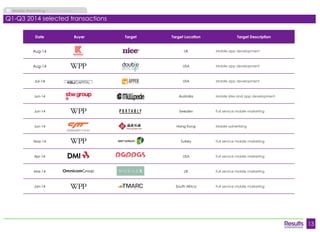

The document analyzes key trends in the marketing communications and technologies industry, focusing on the convergence of marcoms and martech, particularly in content marketing, data analytics, ecommerce, digital, and mobile marketing as of Q3 2014. It highlights significant growth in mobile ad spend, especially in the UK, where it is projected to take a large share of digital advertising by 2018, and discusses the increasing importance of mobile marketing strategies such as native advertising and video marketing. The report also provides insights into the mergers and acquisitions activity within the mobile marketing sector during the first three quarters of 2014.

![Why [Mobile] [In-app] Programmatic? A Marketer's Guide](https://cdn.slidesharecdn.com/ss_thumbnails/mopub-mobile-programmatic-benefits-web-160805140554-thumbnail.jpg?width=640&height=640&fit=bounds)