Downloaded 206 times

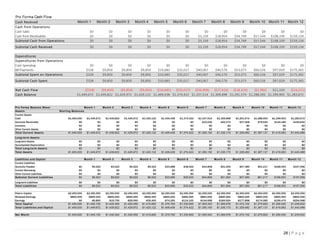

Payment Company is a mobile payment application designed to streamline online purchases, addressing issues of lengthy checkouts and cybersecurity. The app enables users to make transactions securely in under 12 seconds, utilizing encrypted data stored locally on devices. With an expected growth in e-commerce and interest from both small and large retailers, Payment Company aims to raise $2.25 million to capitalize on the significant market opportunity and compete against established payment systems.