Downloaded 18 times

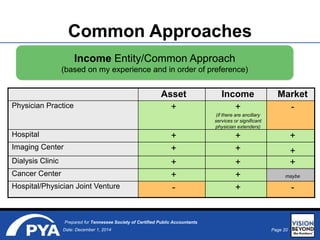

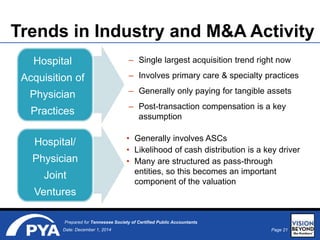

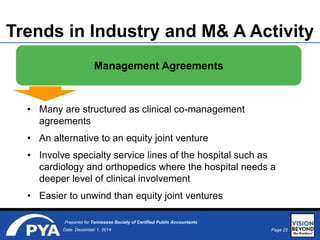

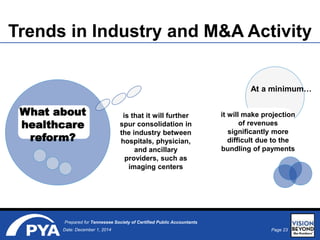

This document presents insights on healthcare valuation, emphasizing the complexities involved due to regulatory factors, market data limitations, and fluctuating trends. It outlines common pitfalls in projecting cash flows, highlights key industry data sources, and discusses various valuation approaches, including asset and income approaches. Additionally, it addresses current trends in mergers and acquisitions within healthcare, particularly concerning the consolidation driven by healthcare reforms.