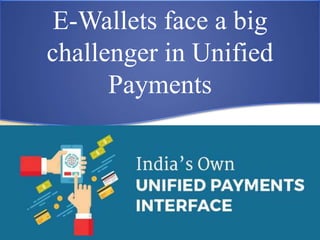

The document discusses the rapid changes in the banking landscape in India, particularly the rise of Unified Payments Interface (UPI) and its implications for mobile wallets, with many wallet players feeling threatened by UPI's convenience and accessibility. It also mentions the Murugappa group's decision to withdraw from the payments bank space due to concerns over financial viability and the changing landscape of financial inclusion. As UPI becomes more prevalent, it is expected to consolidate payment methods and potentially marginalize certain wallet services unless they adapt strategically.