Growth of Digital

Paymentsin India

Trends, Drivers, and Innovations Shaping the Financial Landscape

Presented by Kunal Bansal - MBA Seminar

2.

Presentation Roadmap

Navigating therapid evolution of India’s digital payments sector.

History & Evolution

Brief timeline and foundational context.

Growth Drivers & Scale

Key factors and the overwhelming size of UPI.

Core Infrastructure

Understanding UPI and other vital payment rails.

Market Players

Dominant consumer and enterprise platforms.

Outlook & Challenges

Regulatory landscape and future growth potential.

3.

Why Digital PaymentsAre Essential

Digital finance is a crucial catalyst for economic progress and modernisation in India.

Financial Inclusion

Provides access to formal financial systems for previously

unbanked and underserved populations.

Convenience & Speed

Offers instantaneous, 24/7 transaction processing,

significantly enhancing consumer experience.

Lower Transaction Costs

Dramatically reduces the logistical costs associated with

printing, transporting, and securing physical cash.

MSME & E-commerce Enabler

Digitisation empowers Micro, Small, and Medium Enterprises

(MSMEs) and fuels the growth of the digital economy.

4.

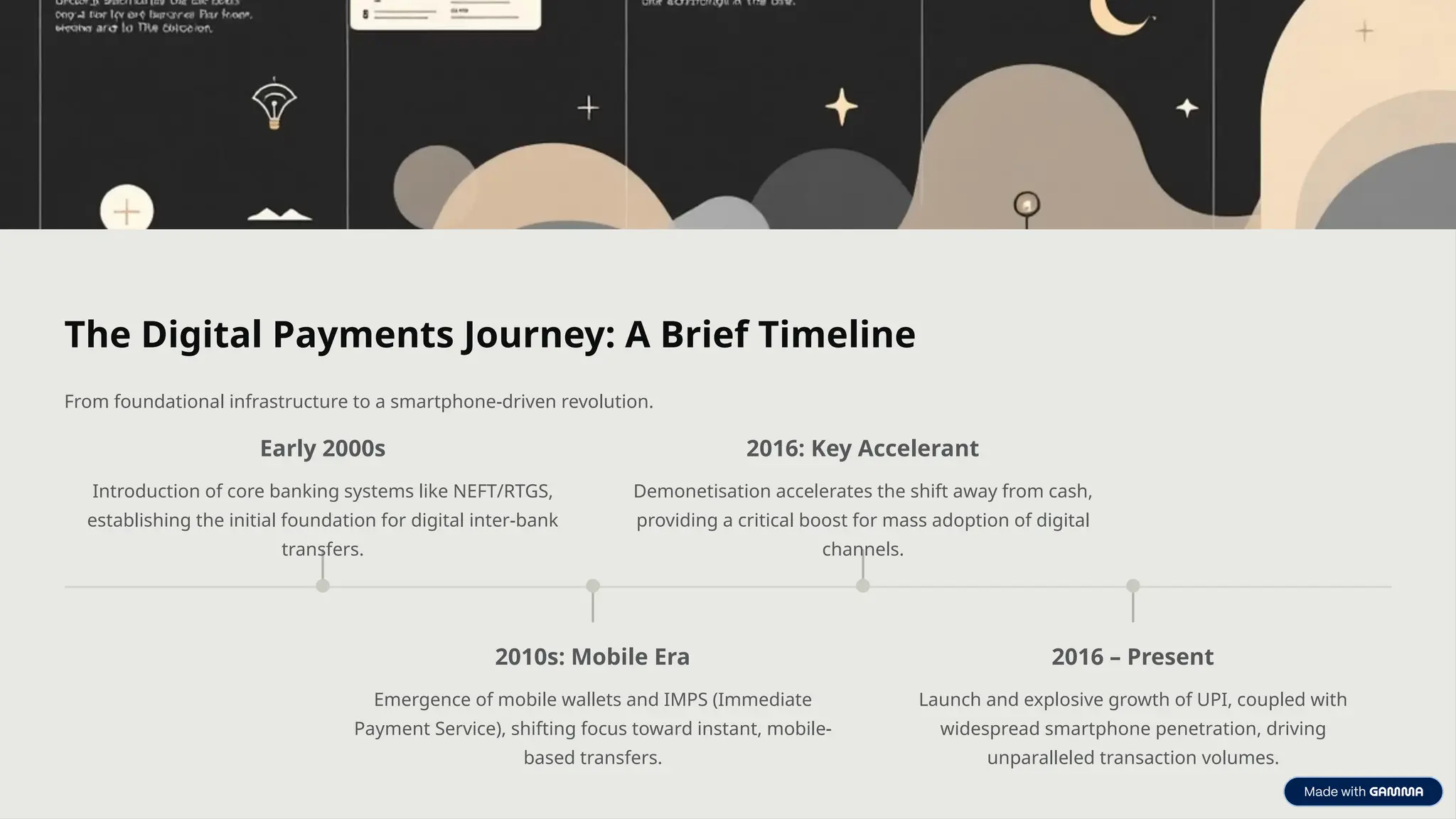

The Digital PaymentsJourney: A Brief Timeline

From foundational infrastructure to a smartphone-driven revolution.

Early 2000s

Introduction of core banking systems like NEFT/RTGS,

establishing the initial foundation for digital inter-bank

transfers.

2010s: Mobile Era

Emergence of mobile wallets and IMPS (Immediate

Payment Service), shifting focus toward instant, mobile-

based transfers.

2016: Key Accelerant

Demonetisation accelerates the shift away from cash,

providing a critical boost for mass adoption of digital

channels.

2016 – Present

Launch and explosive growth of UPI, coupled with

widespread smartphone penetration, driving

unparalleled transaction volumes.

5.

India's Core DigitalPayment Rails

The National Payments Corporation of India (NPCI) operates a diverse and sophisticated suite of payment systems.

UPI (Unified Payments Interface)

The flagship system for instant, real-time, peer-to-peer

(P2P) and person-to-merchant (P2M) payments via

Virtual Payment Addresses (VPAs).

IMPS, NEFT/RTGS

Foundational inter-bank transfer systems, offering

instant (IMPS) or near-real-time (NEFT/RTGS) bulk

transfers, essential for banking operations.

AePS & Wallets

Aadhaar Enabled Payment System (AePS) facilitates

cash withdrawal/deposit using biometric

authentication. Mobile wallets offer pre-paid closed-

loop systems.

FASTag & Bharat BillPay

Dedicated services for automatic vehicle toll collection

(FASTag) and a centralised platform for easy utility bill

payments (BBPS).

6.

UPI: A QuickPrimer on

Interoperability

UPI is a real-time payment layer enabling instant fund transfers

between bank accounts on a mobile platform, simplifying

transactions.

Developed By

NPCI (National Payments

Corporation of India), an

organisation promoted by the

RBI and the Indian Banks’

Association.

Key Feature: Virtual

Payment Addresses

(VPA)

Users transact using a simple

VPA (e.g., name@bank) instead of

complex bank account numbers

and IFSC codes, enhancing

security and speed.

7.

The Scale ofUPI: Unprecedented

Growth

UPI has become the most successful real-time payment system globally,

processing billions of transactions monthly.

19.63B

Transactions

Processed

Total volume of

transactions recorded

in September 2025.

₹24.9T

Total Value

Transacted

The astronomical

value in lakh crore

rupees processed

through UPI in

September 2025.

~50%

Annual Growth

The platform

continues to

demonstrate robust

year-on-year growth

in both volume and

value.

Source: The Economic Times, based on NPCI data. The trajectory shows continued

exponential adoption, driven by merchant integration.

8.

Market Dynamics: TheDominance of UPI Ecosystem

While UPI is the rail, a few major applications command the overwhelming majority of transaction volume.

9.

Primary Drivers ofAccelerated Digital Growth

The combination of technology access and active merchant integration has driven widespread adoption.

1. Smartphone & Data Accessibility

The 'Jio effect' led to drastically reduced data costs and the proliferation of

low-cost smartphones, connecting billions of users to the internet for the

first time.

2. Merchant Adoption & Digital Onboarding

Simplistic deployment methods like static and dynamic QR codes, coupled

with innovations like 'soundboxes,' ensure even small vendors can accept

digital payments easily.

3. Supportive Regulation

The government and RBI's focus on creating public digital infrastructure

(Digital Public Goods) like UPI has lowered entry barriers and fostered

trust.

10.

Ecosystem Players: Consumerand Enterprise

The market thrives on a robust mix of consumer-facing apps and sophisticated enterprise payment processors.

Consumer Apps (UPI-Enabled)

• PhonePe, Google Pay (Market Leaders)

• Paytm, Amazon Pay, WhatsApp Pay

• Focus on P2P, P2M, and bill payments

Merchant/Enterprise Solutions

• Razorpay, PayU (Online Payment Gateways)

• Pine Labs, MSwipe (Physical PoS Solutions)

• Focus on aggregation, reconciliation, and payment processing for businesses.