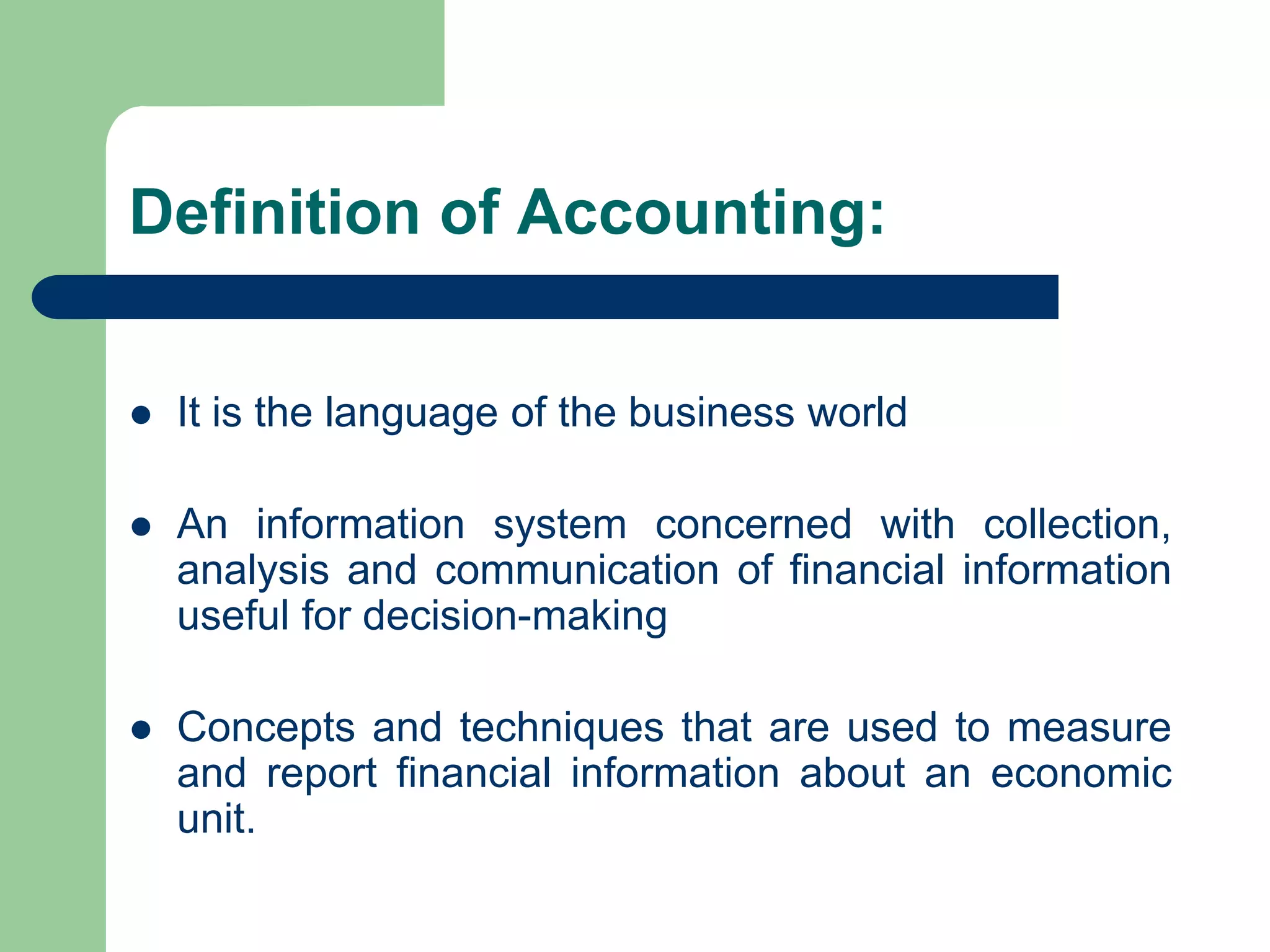

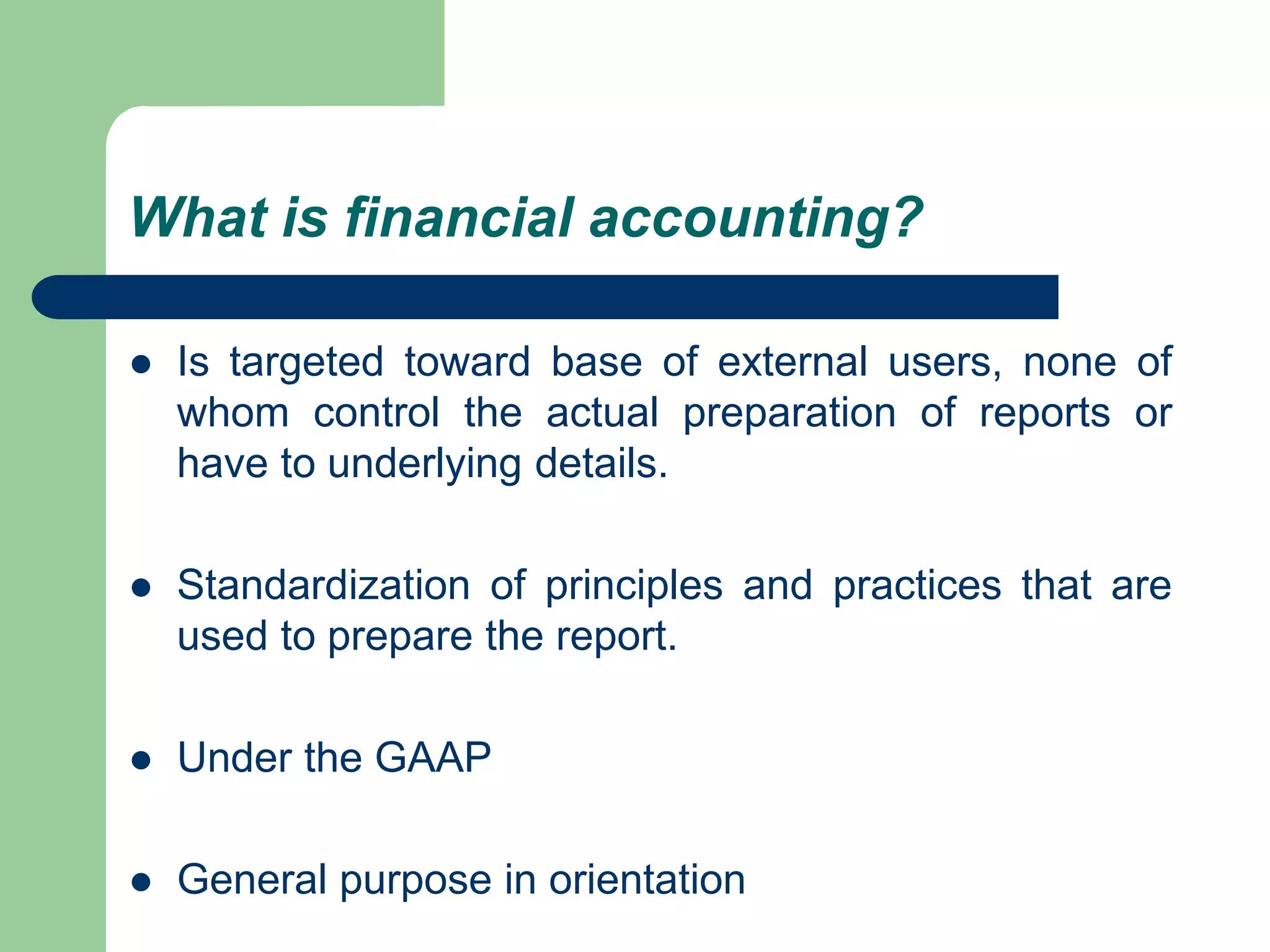

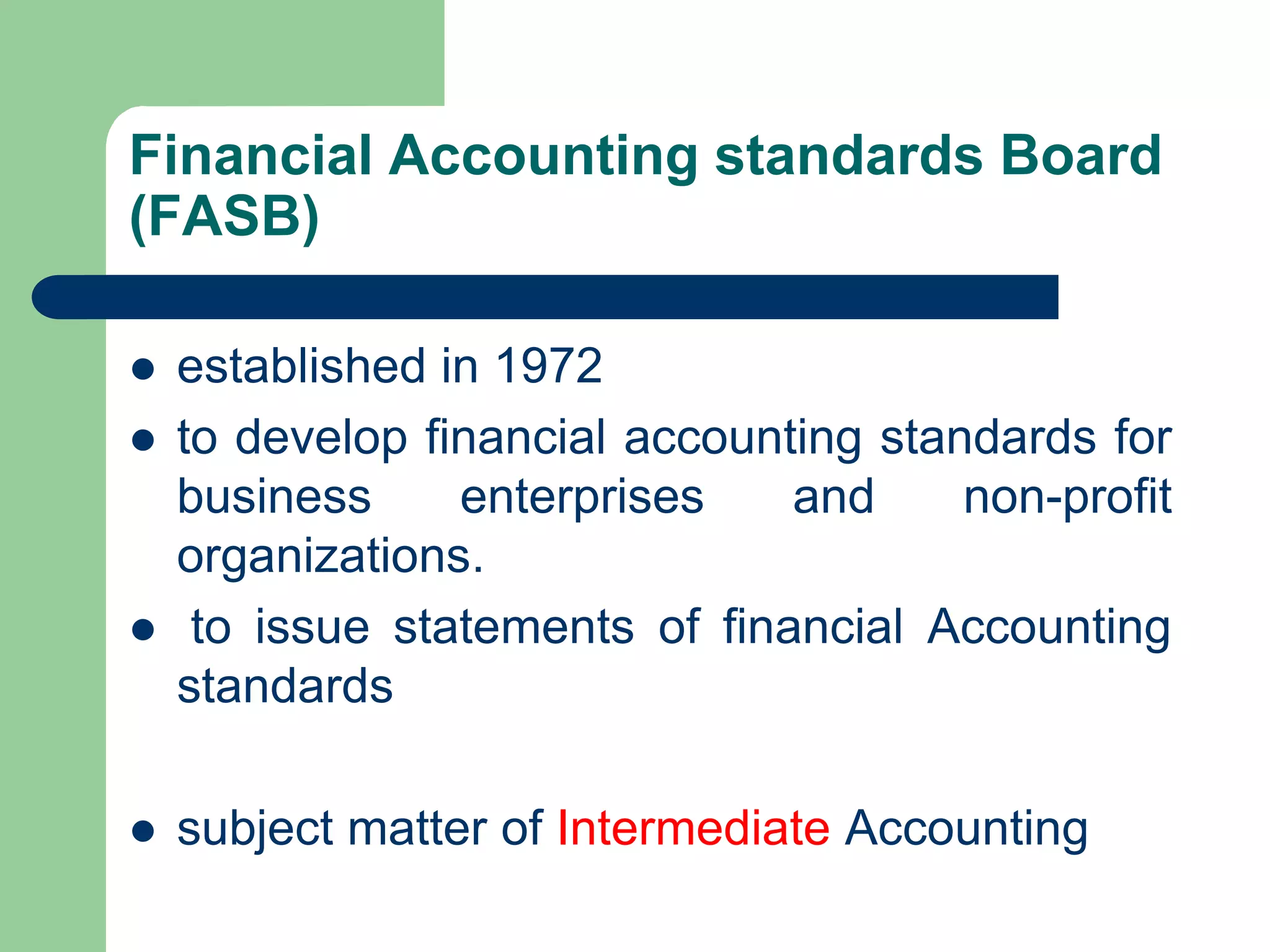

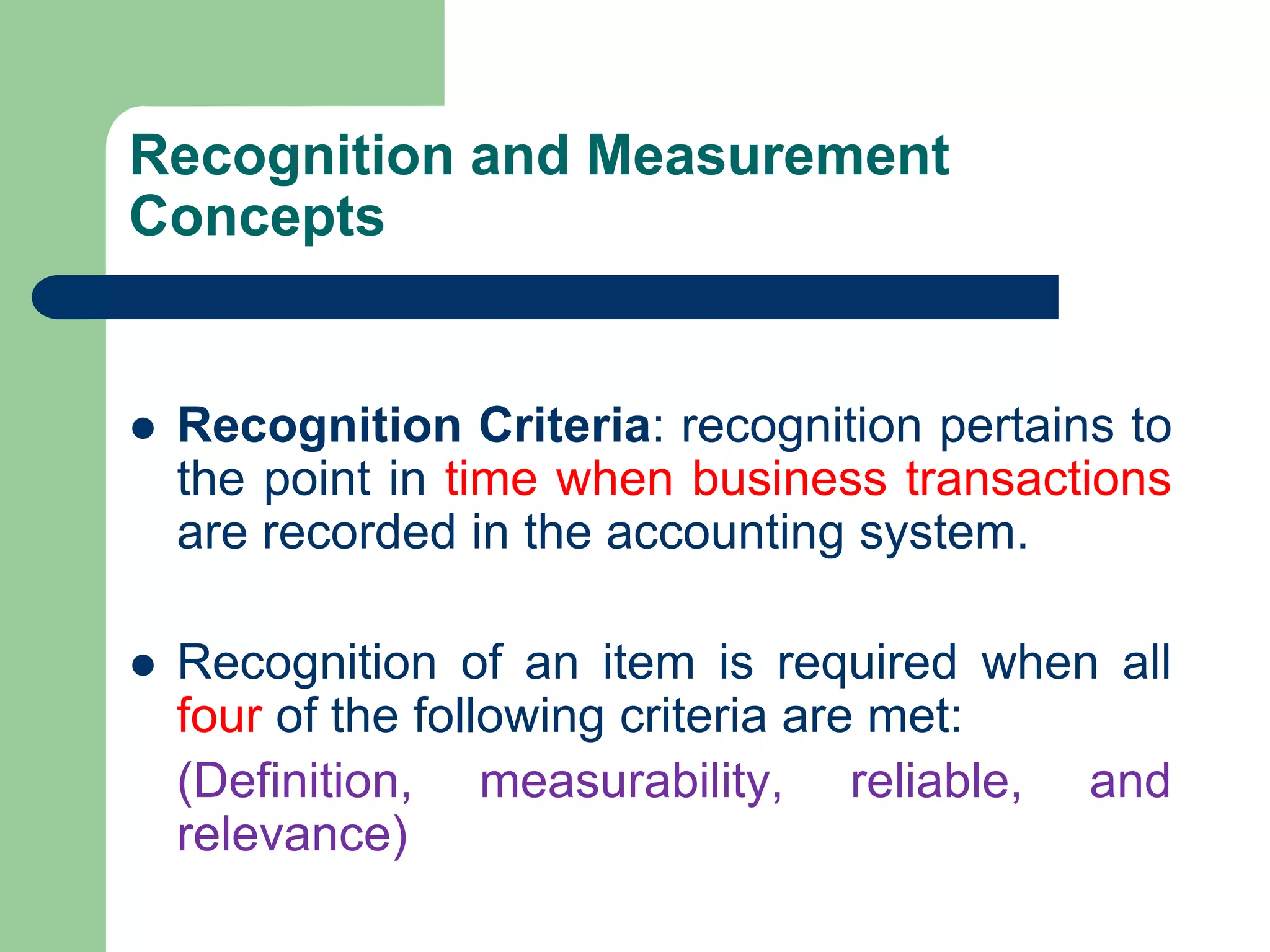

This training introduces financial accounting concepts. The objectives are to understand basic accounting concepts including the FASB, financial statements, assumptions, principles, accrual and cash basis accounting, and the accounting equation. Key topics covered include the definition of accounting and financial accounting, the roles of the FASB and elements of financial statements. The presentation also discusses recognition and measurement concepts, basic assumptions and principles, and cash versus accrual accounting methods.