Download to read offline

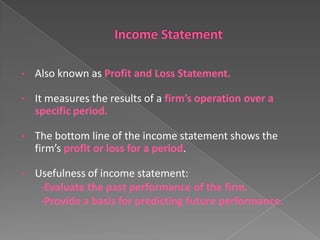

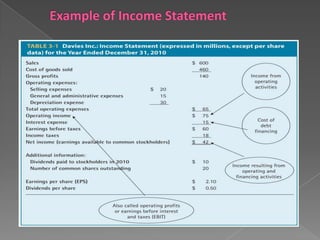

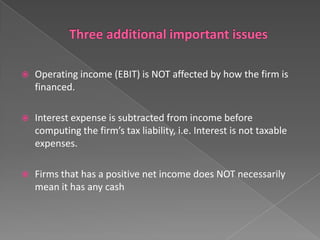

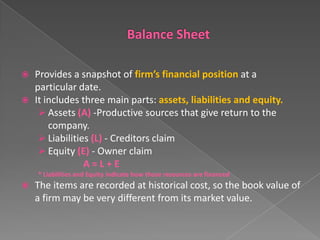

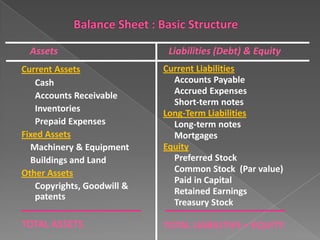

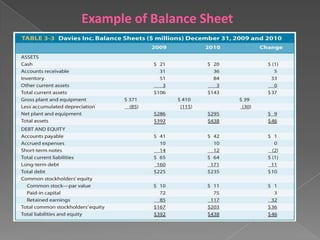

The document discusses the needs and purposes of key financial statements including the income statement, balance sheet, and statement of cash flows. It explains the components and calculations of these statements. It also describes common financial ratios used in analysis of statements, such as liquidity, profitability, asset management, and leverage ratios. These ratios are used to evaluate a firm's performance and financial position over time and in comparison to other companies.

![Topic 4[1] finance](https://cdn.slidesharecdn.com/ss_thumbnails/topic41-131107182635-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Topic 3 1_[1] finance](https://cdn.slidesharecdn.com/ss_thumbnails/topic311-131107182625-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)