Download to read offline

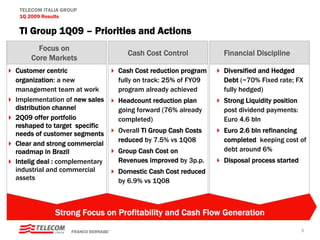

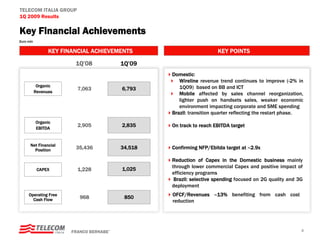

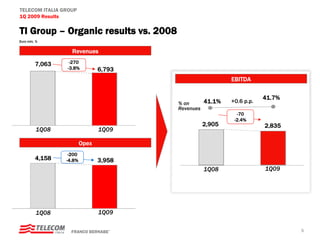

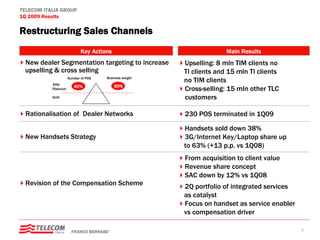

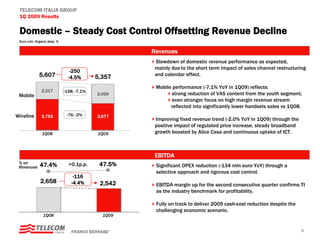

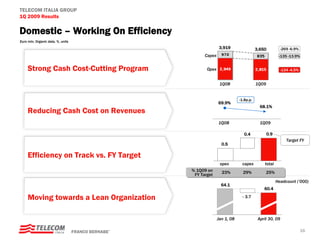

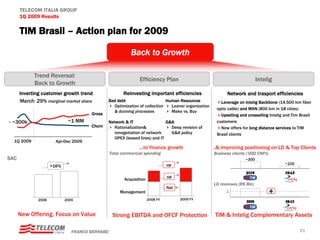

Telecom Italia Group reported its 1Q09 results, focusing on cost control and cash flow generation. Revenues declined 3.8% organically due to challenges in the domestic market from channel restructuring and the economy. However, EBITDA was largely stable as cash costs fell 7.5%. Looking ahead, Telecom Italia will continue restructuring sales channels and controlling costs while implementing new offers to boost revenues in key segments.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)